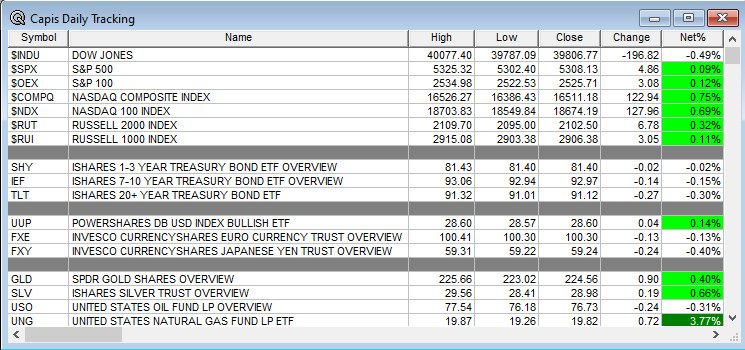

Overnight Summary: The S&P 500 closed Monday higher by +0.09% at 5308.13 from Friday at 5303.27 up by 0.12%. The overnight high was hit at 5,335.75 at 4:05 p.m. while the overnight low was hit at 5329 at 5:45 a.m. EDT. The range overnight is 16 points as of 7:00 a.m. EDT. Currently, the S&P 500 is lower by -1.25 points at 6:15 a.m. EDT.

Executive Summary: Stocks are higher to start the week with the catalyst of the week being Nvidia’s earnings due on Wednesday after the close. No change from yesterday.

- Lots of Fedspeak continues.

Earnings Out After The Close:

- Beats: ZM +0.16, PANW +0.07, NDSN +0.03, KEYS +0.02 of note.

- Flat: None of note.

- Misses: None of note.

- IPOs For The Week:

- New SPACs launched/News:

- IPOs Filed:

- Secondaries Files or Priced:

- DYN filed $300 million offering.

- LNC filed 44 million shares of common stock related to incentive compensation plan.

- HL files 2,068,000 shares of common stock.

- APLM filed offering of 19,166,666 common shares.

- MULN filed 20 million shares of common stock.

- FIHL filed secondary offering of common stock.

- Common Stock filings/Notes:

- Notes Priced of note:

- Direct Offering:

- Exchangeable Subordinate Voting Shares:

- Selling Shareholders of note:

- files to sell 14.421,070 shares by selling shareholders.

- Debt/Credit Filing and Notes:

- Mixed Shelf Offerings:

- OWL: Filed a Mixed Shelf Offering.

- NWL: Filed a $2.75 billion Mixed Shelf Offering.

- BIOR: Filed a Mixed Shelf Offering.

- PHIO: Filed a $100 million Mixed Shelf Offering.

- Private Placement of Public Entity (PIPE):

- Rights Offering:

- Convertible Offering & Notes Filed:

- Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close :

- Changes After The Close:

- LRMR +23.4%, TRNS +3.8%

- NDSN -12.40%, PANW -8.3%, PTON -5.9%, HSAI -4.9%, KEYS -2.7%

- News Items After the Close:

- APA sells two assets for $700 million.

- PSX to buy Pinnacle Midland Parent LLC for $550 million.

- SUZ may make a higher bid for International Paper (IP).

- CAAP announces a -4.8% decrease in passenger traffic.

- FDIC Chair to leave after reports of toxic workplace. (Bloomberg)

- Exchange/Listing/Company Reorg and Personnel News:

- NRIX Board Chair David L. Lacey steps down; board member Julia P. Gregory unanimously elected new board chair

- TALK announces CFO transition, appointing Ian Harris as new CFO.

- FWRD CFO Rebecca Garbrick to step down, names interim CFO.

- LEG appoints Karl Glassman as President and CEO

- Stock Splits or News:

- APH approves a 2:1 split.

- Buyback Announcements or News:

- INFU announced a $20 million repurchase agreement.

- Dividends Announcements or News:.

- ups dividend to $0.45 from $0.30.

What’s Happening This Morning: Futures value reflects the change with fair value. Futures on the Dow +23, S&P 500 +4.62, NASDAQ -0.94, and Russell -3.90. Asia and Europe are lower this morning. VIX Futures are at 13.57 from 13.51. Gold and Silver are lower with Copper higher this morning. WTI Crude Oil and Brent Crude Oil lower with Natural Gas higher. US 10-year Treasury sees its yield at 4.426% from 4.414% yesterday. The U.S. Dollar is lower versus the Euro, lower versus the Pound and higher against the Yen. Bitcoin is at $71,227 from $67,215 higher by 2.29% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

- Daily Positive Sectors: Technology, Materials, Communication Services and Industrials of note.

- Daily Negative Sectors: Financials, Consumer Defensive, Real Estate and Consumer Cyclical of note.

- One Month Winners: Utilities, Real Estate, Technology, Consumer Defensive and Financials of note.

- Three Month Winners: All led by Utilities, Energy, Materials, Financials and Communication Services of note.

- Six Month Winners: Communication Services, Technology, Industrials and Financials of note.

- Twelve Month Winners: Communication Services, Technology, Financials, Industrials, and Consumer Cyclicals of note.

- Year to Date Winners: Communication Services, Energy, Utilities, Technology, Financials, Industrials and Consumer Defensive of note.

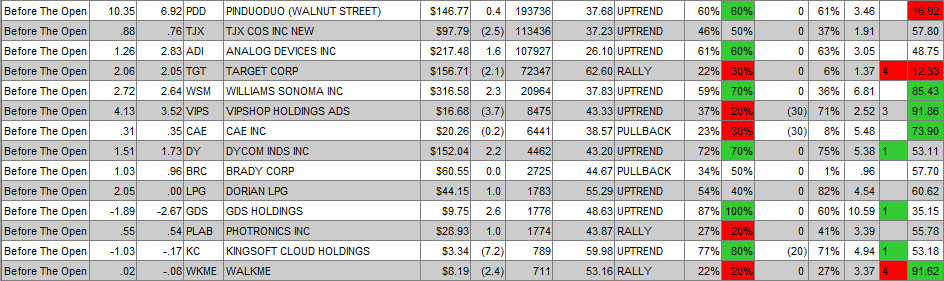

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Wednesday Before the Open:

Earnings of Note This Morning:

- Beats: AZO +0.67, LOW +0.11, M +0.11, AS +0.07 of note.

- Flat: None of note.

- Misses: EXP -0.46 of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative Guidance: NDSN KEYS of note.

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market (+4% or down more than -4%):

- Gap Up: LRMR +18.3%, XPEV +5.7%, NRIX +5.1%, MTUS +4.4%, ALVO +4.4%, TRNS +4.3%, INFU +4%, CTKB +2.5%, LOW +2.1% of note.

- Gap Down: NDSN -12.1%, HSAI -11%, PANW -7.8%, JD -4.2%, KEYS -4.2%, PTON -2.3% of note.

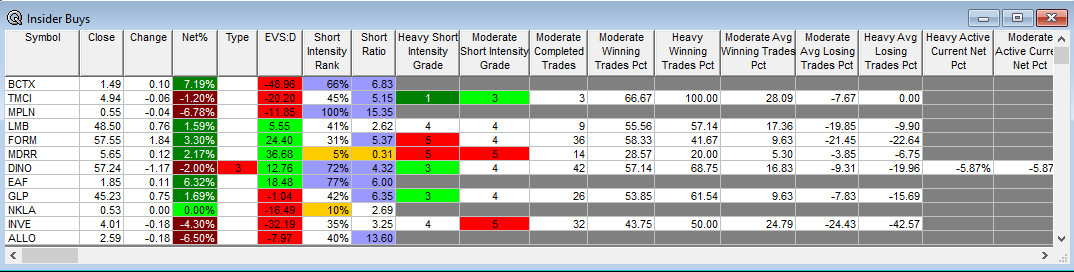

Insider Action: DINO sees Insider buying with dumb short selling. No names see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- What You Need To Know To Start Your Day. (Bloomberg)

- 5 Things to Know Before The Stock Market Open Today. (CNBC)

- Morning Briefing For Bloomberg Subscribers (Bloomberg)

- Stocks Making The Biggest Move: (CNBC)

- Bloomberg Lead Story: ASML and Taiwan Semi Can Disable Chip Machines If China Invades Taiwan. (Bloomberg)

- Stocks slip as focus turns to Nvidia and Fed Speak: Markets Wrap. (Bloomberg)

- Lowe’s (LOW) beats despite slowdown on Do It Yourself projects. (CNBC)

- British inflation rate could drop under 2%. (CNBC)

- Bloomberg’s The Big Take: Google’s Moonshot factory falls back down to earth. (Podcast)

- NY Times Daily: The Crypto Comeback. (Podcast)

- Marketplace: Why cellphones may be affecting polling data. (Podcast)

- Wealthion: Inflation slowdown Can we win the battle? (Podcast)

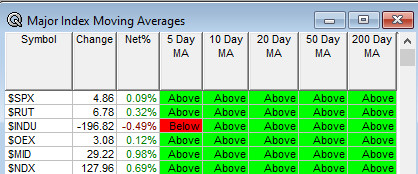

Moving Average Update: Score at 97% from 100%.

Geopolitical:

- President’s Public Schedule:

- There is a Daily Briefing today at 8:00 a.m. EDT.

- President Biden heads to Nashua, NH at 9:40 a.m. EDT and then speaks at 1:30 p.m. EDT on the PACT Act.

- The President then heads to Boston for a campaign reception at 7:30 p.m. EDT and arrives back at the White House at 10:05 p.m. EDT.

Economic:

- Weekly API Crude Oil Inventories are due out at 4:30 p.m. EDT.

Federal Reserve / Treasury Speakers:

- Federal Reserve Governor Christopher Waller speaks at 9:00 a.m. EDT.

- Federal Reserve Richmond President Thomas Barkin speaks at 9:00 a.m. EDT.

- Federal Reserve New York President John Williams speaks at 9:05 p.m. EDT.

- Federal Reserve Governor Michael Barr speaks at 11:45 a.m. EDT.

- Federal Reserve Atlanta President Raphael Bostic speaks at 7:00 p.m. EDT.

M&A Activity and News:

Meeting & Conferences of Note:

- Sellside Conferences:

- Top Shareholder Meetings: BMRN, BYON, CVII, DINO, DSX, FL, INO, JPM, LBTYA, NE, OCFC, RWT, SHEL,

SNBR, SOFI, STKS, TMCI, TTI, USM, VSH, WEN

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: ARCC, ARES, AZN, CELU, CW, CYBR, GE

- Update: None of note.

- R&D Day: None of note.

- FDA Presentation:

- Company Event:

- Industry Meetings:

- ALS Drug Development Summit

- American Thoracic Society International

- Barclays Leveraged Finance Conference

- Benchmark Healthcare House Call Virtual Conference

- Cowen Virtual Sustainability Conference

- Digestive Disease

- Gartner CFO & Finance Executive Conference

- IMPACT 24: The Identity Security Conference

- JP Morgan TMT Conference

- Mizuho Neuroscience Summit

- SME Current Trends in Mining Finance Conference

- Spinal Cord Injury Investor Symposium

- TD Cowen Sustainability Conference

- UBS Spring Biotech Conference

- Wolfe Global Transportation & Industrials Conference

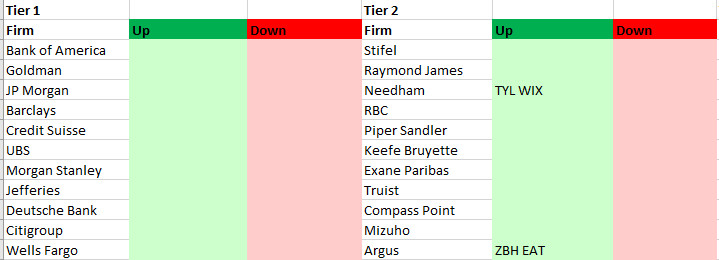

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades: