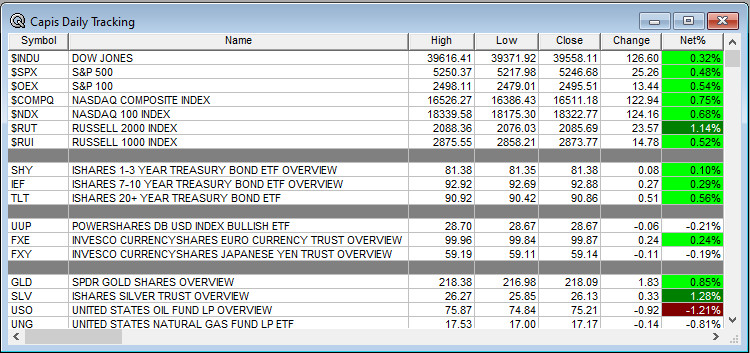

Overnight Summary: The S&P 500 closed Tuesday at 5246.68 higher by +0.48% from Monday at 5221.42 lower by -0.02%. The overnight high was hit at 5,277.50 at 10:45 p.m. while the overnight low was hit at 5266.25 at 6:05 p.m. EDT. The range overnight is 11 points as of 7:10 a.m. EDT. Currently, the S&P 500 is higher by +2 points at 7:10 a.m. EDT.

Executive Summary: All eyes are focused on CPI this morning.

- Multiple Economic Releases see below. Key is CPI release at 8:30 a.m. EDT.

- Several Fed speakers on deck.

Earnings Out After The Close:

- Beats: NXT+0.28, SDRL +0.15, BOOT +0.07, CSWC +0.02 of note.

- Flat: None of note.

- Misses: KYTX -0.28, PBH -0.12, DLQ -0.06, DHT -0.01 of note.

- IPOs For The Week: BTOC GGL JDZG KDLY RAY.

- New SPACs launched/News:

- IPOs Filed:

- Secondaries Priced:

- Common Stock filings/Notes:

- VSEC files a common share offering.

- Notes Priced of note:

- Direct Offering:

- Exchangeable Subordinate Voting Shares:

- Selling Shareholders of note:

- Debt/Credit Filing and Notes:

- Mixed Shelf Offerings:

- PKOH: Filed a $125 million Mixed Shelf Offering.

- Private Placement of Public Entity (PIPE):

- Rights Offering:

- Convertible Offering & Notes Filed:

- Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close :

- Winners & Losers After The Close:

- AMC +16.80%, HROW +14.9%, VYGR +7.9%, PSFE +7.2%, STXS +6.1%, ALLO +5.2%, IFIN +5.2%

- NOTV -12.50%, MBIN -9.2%, STNE -7%, NGD -5.7%

- News Items After the Close:

- Bond King Bill Gross sells calls and puts on Meme stocks. (Bloomberg)

- Traders set up for post CPI pop with 10 Year going to 4.30%. (Bloomberg)

- Walmart to cut white collar jobs at headquarters. (Reuters)

- Vanguard to tap former Blackrock Executive Salim Ramji as CEO. (WSJ)

- DDD, NOTV, MAPS, FRST, RXT, RILY and SPWR delay their 10-Qs.

- Exchange/Listing/Company Reorg and Personnel News:

- Petco Health and Wellness (WOOF) appoints Glenn Murphy as Executive Chairman

- SMART Global (SGH) announces departure of CFO Ken Rizvi, Jack Pacheco, SGH COO and Former CFO, to serve as interim CFO.

- Synaptics (SYNA) appoints Ken Rizvi as CFO, effective July 15.

- Buyback Announcements or News:.

- Stock Splits or News:

- Dividends Announcements or News:.

What’s Happening This Morning: Futures value reflects the change with fair value.

S&P 500 +2, Dow Jones +14, NASDAQ -3.50, Russell +9.11. (as of 8:15 a.m. EDT). Asia is higher and Europe is higher this morning ex the CAC. VIX Futures are at 14.25 from 14.52. Gold, Silver and Copper are higher this morning for a second day in a row. WTI Crude Oil and Brent Crude Oil are higher with Natural Gas higher as well. US 10-year Treasury sees its yield at 4.42% from 4.477% yesterday. The U.S. Dollar is lower versus the Euro, lower versus the Pound and lower against the Yen. Bitcoin is at $62,600 from $61,686.34 higher by 1.74% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

- Daily Positive Sectors: Technology, Real Estate, Materials, Financials, Communication Services and Healthcare of note.

- Daily Negative Sectors: Consumer Defensive of note.

- One Month Winners: Utilities, Consumer Defensive, Financials, and Healthcare of note.

- Three Month Winners: All but Real Estate led by Utilities, Energy, Materials and Communication Services of note.

- Six Month Winners: Communication Services, Technology, Industrials and Financials of note.

- Twelve Month Winners: Communication Services, Technology, Financials, Industrials, and Consumer Cyclicals of note.

- Year to Date Winners: Communication Services, Energy, Utilities, Technology, Financials, Industrials and Consumer Defensive of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Wednesday After the Close:

- Thursday Before the Open:

Earnings of Note This Morning:

- Beats: MNDY +0.21, RSKD +0.11, DOLE +0.12, DT+0.03, of note.

- Flat: of note.

- Misses: of note.

- Still to Report: ARCO of note.

Company Earnings Guidance:

- Positive Guidance: MNDY of note.

- Negative Guidance: of note.

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market (+4% or down more than -4%):

- Gap Up: ARQT +25.3%, NXT +13.9%, GSM +7.7%, FOUR +6.2%, NU +6%, NYCB +5.9%, BLNK +4.6%, ATNM +3.1%, BGS +2.6%, KRMD +2.2%, ORLA +2.1%of note.

- Gap Down: DLO -26.7%, PBR -8.8%, PBH -7.7%, DT -5.9%, BOOT -5.6%, RUM -3.8%, VSEC -3.5%, NUVB -3%, DHT -2.5%, INFN -2.4% of note.

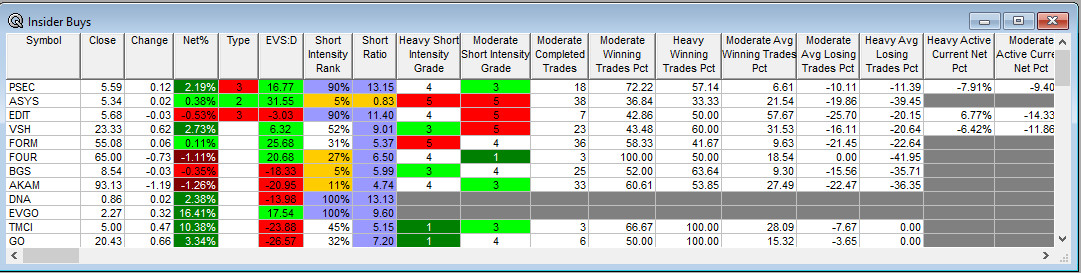

Insider Action: PSEC EDIT see Insider buying with dumb short selling. No stocks see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- What You Need To Know To Start Your Day. (Bloomberg)

- Bloomberg Lead Story: China Government Considers Buying Unsold Homes To Save Property Market. (Bloomberg)

- Mortgage Demand drops despite rates falling as well. (CNBC)

- Stocks hold gains ahead of CPI data: Market Wrap. (CNBC)

- What to expect on key inflation report. (CNBC)

- China Foreign Minister says U.S. is “losing its mind” over Tariff decisions. (Reuters)

- President Biden to push ahead with new weapons deal worth $1 billion to Israel. (WSJ)

- DOJ notifies Boeing (BA) that it violated its 2021 agreement over 737 Max crashes. (CNN)

- Bridgewater CEO warns of overconfidence to investors. (Bloomberg)

- Walmart (WMT) under threat to remain the largest retailer as Amazon is closing in on them. (WSJ)

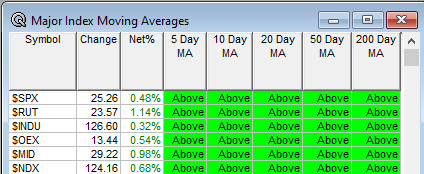

Moving Average Update: Score at 100% from 97%.

Geopolitical:

- President’s Public Schedule:

- There is a Daily Briefing today at 2:45 p.m. EDT.

- President Biden delivers remarks at the U.S. Capitol at 12:00 p.m. EDT at the National Peace Officer’s Memorial.

- Press Briefing at 1:30 p.m. EDT with Press Secretary Karine Jean-Pierre.

- President Biden hosts the Joint Chiefs and Combatant Commanders for a meeting at 4:30 p.m. EDT and then a dinner 6:30 p.m. EDT.

Economic:

- April CPI is due out at 8:30 a.m. EDT and is expected to remain at 0.4%.

- April Housing Starts are due out at 8:30 a.m. EDT and is expected to remain at 0.4%.

- April Retail Sales are due out at 8:30 a.m. EDT and are expected to come in at 0.4% from 0.7%.

- May Empire Manufacturing is due out at 8:30 a.m. EDT as well and is expected to come in at -9.0 from -14.3.

- May NAHB Housing Market Index is due out at 10:00 a.m. EDT and is expected to remain at 51.

- Weekly Crude Oil Inventories are due out at 10:30 a.m. EDT.

Federal Reserve / Treasury Speakers:

- Federal Reserve Governor Michael Barr speaks at 10:00 a.m. EDT

- Federal Reserve Minnesota President Neel Kashkari speaks at 12:00 p.m. EDT.

- Federal Reserve Governor Michelle Bowman speaks at 3:00 a.m. EDT.

M&A Activity and News:

Meeting & Conferences of Note:

- Sellside Conferences:

- Top Shareholder Meetings: AAN BG BLK HAL HIG KSS LUV PSX STT TAP TRV UHS VLO VRTX ZI

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: AXTA BRFH BYSI GDRX HRTX LDTC OLMA SQSP UBER

- Update: None of note.

- R&D Day: None of note.

- FDA Presentation: LYRA

- Company Event:

- Industry Meetings:

- Bank of America Healthcare Conference, Global Metals & Mining Conference and Transportation and Industrials Conference

- Barclays Emerging Payment and FinTech Forum

- BMO Global Farm to Market Conference, Farm to Market Chemicals Conference

- Citi Energy Conference

- Goldman Sachs Structured Leverage and Credit Conference

- JPM Homebuilding Conference

- JPM Life Sciences

- Needham Technology Conference

- RBC Global Healthcare Conference

- Wells Fargo Financial Services Conference

- Wolfe Research Commercial Real Estate Conference

Top Tier Sell-side Upgrades & Downrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades: