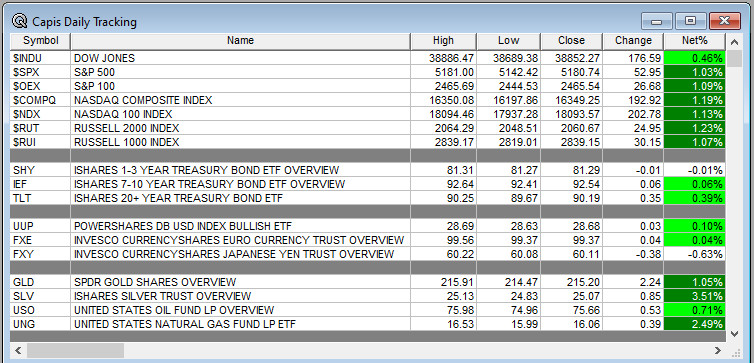

Overnight Summary: The S&P 500 closed Monday higher by 1.03% at 5180.74 from Friday higher by 1.26% at 5127.79. The overnight high was hit at 5,213.25 at 5:15 a.m. while the overnight low was hit at 5202.25 at 4:10 a.m. EDT. The range overnight is 11 points as of 7:05 a.m. EDT. Currently, the S&P 500 is higher by +3.75 points at 7:05 a.m. EDT.

Executive Summary: The quiet week continues with stocks mixed this morning.

- 3-Year Auction at 1:oo p.m.

- Consumer Credit due out at 3:00 p.m. EDT.

- Uber Hawk Federal Reserve Minneapolis President speaks at 11:50 a.m. EDT.

Earnings Out After The Close:

- Beats: SPG +0.75, VRTX +0.68, SWAV +0.45, FIS +0.37, BCC +0.32, FN +0.28, IFF +0.27, JJSF +0.23, AXON +0.20, MWA +0.16, CBT +0.12, COHR +0.11, GT +0.11, VAC +0.11, WMB +0.10, PLYA +0.07, FMC +0.04, HIMS +0.04, JELD +0.03, TDC +0.02 of note. (Greater than +0.10)

- Flat: None of note.

- Misses: DOOR -0.71, BYON -0.35, PRI -0.21, LCID -0.05, VNO -0.03, O -0.01 of note.

- IPOs For The Week: .

- New SPACs launched/News:

- Secondaries Priced:

- Notes Priced of note:

- Common Stock filings/Notes:

- Direct Offering:

- Exchangeable Subordinate Voting Shares:

- Selling Shareholders of note:

- TMUS files 3,264,952 common stock offering by a selling shareholders.

- AL files 4,643,608 shares of common stock by selling shareholders.

- by selling shareholder.

- Debt/Credit Filing and Notes: .

- Mixed Shelf Offerings:

- CNO files mixed-shelf offering

- GPRE files a mixed-shelf offering

- TBI files a $200 million mixed-shelf offering

- NOW files a mixed-shelf offering

- AL files a mixed-shelf offering

- APLD files a $300 million mixed-shelf offering

- ARI files a mixed-shelf offering

- Tender Offer:

- Private Placement of Public Entity (PIPE)

- Rights Offering:

- Convertible Offering & Notes Filed:

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

- Movers of Note:

- EVER +11%, ZETA +10.1%, HIMS +10.1%, SYM +9.1%, RXST +8.4%, UCTT +7.4%, FN +6%, IFF +5.8%, JJSF +4.3%, PLYA +3.9%, PRA +3.8%, PRAA +2.6%, TVTX +2.3%

- PAY -9.8%, PLTR -9.1%, LCID -6.6%, MCHP -4.6%, TDC -4.1%, LITE -3.1%

- News Items After the Close:

- Vertex (VRTX) tops estimates for Q1 on Cystic Fibrosis treatment. (Reuters)

- Lucid (LCID) reports a loss in Q1 but Gravity SUV still on track for 2024 release. (Yahoo Finance)

- Coty (COTY) beats Q3 estimates on revenues on strong demand. (Reuters)

- Reddit (RDDT) set to report first quarter as a public company. (MarketWatch)

- Axon (AXON) raises full year guidance on strong demand for software products. (Reuters)

- Jefferies (JEF) and Weiss Multi Strat get nasty in court over bankruptcy proceedings. (Bloomberg)

- Treasury released the Social Security and Medicare trustees reports. (Press Releases)

- Buyback Announcements or News

- MYRG announces a $75 million buyback program.

- EVRI ends repurchase program.

- Exchange/Listing/Company Reorg and Personnel News

- UPS CFO Brian Newman to step down June 1.

- IFF Chief Financial and Business Transformation Office Glenn Richter to retire.

- Stock Splits or News:

- USLM announces a 5-1 split on July 15th.

- Dividends Announcements or News:

- CBT increases quarterly dividend to $0.43 from $0.40..

What’s Happening This Morning: Futures value reflects the change with fair value.

S&P 500 +16.50, Dow Jones +124, NASDAQ +41, Russell +18.88. (as of 8:15 a.m. EDT). Asia and Europe are higher this morning. VIX Futures are at 14.28 from +14.40. Gold, Silver and Copper are lower this morning. WTI Crude Oil and Brent Crude Oil are lower with Natural Gas higher for the fourth day in a row. US 10-year Treasury sees its yield at 4.461% from 4.48% yesterday. The U.S. Dollar is higher versus the Euro, higher versus the Pound and higher against the Yen. Bitcoin is at $64,033 from $64,284 by +1.55% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

- Daily Positive Sectors: All led by technology, Financials and Industrials of note.

- Daily Negative Sectors: None of note.

- One Month Winners: Consumer Defensive,Communication Services, and Utilities of note.

- Three Month Winners: All but Real Estate led by Energy, Materials and Communication Services of note.

- Six Month Winners: Communication Services, Technology, Industrials and Financials of note.

- Twelve Month Winners: Communication Services, Technology, Financials, Industrials, and Consumer Cyclicals of note.

- Year to Date Winners: Communication Services, Energy, Technology, Financials, Industrials, and Technology, Consumer Defensive of note.

(WSJ – Edited by QPI)

Upcoming Earnings Of Note:

- Tuesday After the Close: ($3 Billion Market Cap Cut Off)

- Wednesday Before the Open: ($3 Billion Market Cap Cut Off)

Earnings of Note This Morning:

- Beats: of note.

- Flat: of note.

- Misses: of note.

- Still to Report: of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative Guidance: None of note.

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: ZETA +19.7%, MWA +17.8%, HIMS +14.3%, BRBR +13.2%, AMBC +12.4%, VMEO +11.8%, FN +9.6%, SYM +9.4%, RXST +9.4%, PRAA +9.2%, UBS +9%, UCTT +8.3%, COHR +7.7%, JJSF +7.2%, OTTR +7.1%, SIM +6.5%, ATSG +5.7%, KNF +4.9%, IFF +4.7%, CMPO +4.4%, ADTH +4.4%, AORT +4.4%, LITE +4%, USLM +3.9%, COTY +3.8%, PRA +3.8%, COKE +3.3%, TVTX +3.1%, EVER +3%, TBI +2.9%, PLYA +2.9%, CPG +2.8%, RCKT +2.2%, SAFE +2.1%, MRUS +2%, GBDC +2%, IDYA +2%, HSIC +2%, of note.

- Gap Down: CELH -15%, AUDC -11%, TDC -10.9%, PLTR -10.2%, GEO -9.8%, BYON -9.1%, LCID -8.5%, JELD -5.5%, AL -4.6%, PARR -4.5%, MCHP -3.9%, RKLB -3.9%, ATKR -3.7%, VNO -3.2%, HNRG -3.1%, ASR -2.8%, CNO -2.3%, RYAM -2.2%, CLLS -2.1%, BSM -2.1%, ADTN -2.1%, DOOR -2%, of note.

Insider Action: TBBK sees Insider buying with dumb short selling. Yesterday we missed writing about DAL and LEG which made the list. Today sees HI with Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- 5 Things To Know Before The Market Opens On Tuesday. (CNBC)

- What You Need To Know To Start Your Day. (Bloomberg)

- Stocks Making the Biggest Moves: DIS PLTR HIMS (CNBC)

- Bloomberg Lead Story: Israel Troops Take Control of Rafah Border Crossing in Gaza. (Bloomberg)

- Former Hedge Fund Titan Stanley Drukenmiller interviewed on CNBC. Still sees upside in AI. With Trump worried about inflation and with Biden worried about stagflation.

- Stocks gain on bank earnings, rate cut optimism: Markets Wrap. (Bloomberg)

- Ahead of retail earnings, here is what we know about the consumer. (CNBC)

- Walt Disney (DIS) tops analyst estimates as streaming nearly breaks even. (CNBC)

- Bloomberg Daybreak Podcast: UBS surges the most in a year. (Podcast)

- Bloomberg Big Take Podcast: Bill Hwang’s $36 billion house of cards. (Podcast)

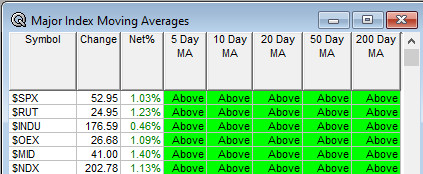

Moving Average Update: Score moves to 100% from 87%.

Geopolitical:

- President’s Public Schedule:

- President Biden receives the Daily Briefing at 9:00 p.m. EDT.

- President Biden to deliver keynote speech at the Holocaust Museum Annual Days of Rembrance Ceremony at 11:30 a.m. EDT.

- President Biden meets with Romanian President Klaus Iohannis at 1:30 p.m. EDT.

- Press Briefing with Press Secretary Karine Jean-Pierre at 2:00 p.m. EDT.

Economic:

- March Consumer Credit is due out at 3:00 p.m. EDT and is expected to come in at $15,3 billion from $14.1 billion.

- Treasury holds a 3-Year Note Auction at 1:00 p.m. EDT.

- Weekly API Crude Oil Report is out at 4:30 p.m. EDT.

Federal Reserve / Treasury Speakers:

- Federal Reserve Minneapolis President Neel Kashkari speaks at 11:30 a.m. EDT.

M&A Activity and News:

Meeting & Conferences of Note:

- Sellside Conferences:

- Top Shareholder Meetings: ALB ARW BAX D DHR EW GMY GE GPS INTC MTW OSK

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: AAPL AMX ASLN CSCO FIS MBRX UMC PGR

- Update: None of note.

- R&D Day: None of note.

- FDA Presentation:

- ANNX has FDA Data Presentation on ANX007

- Company Event:

- Industry Meetings:

- American Society of Cell & Gene Therapy Meeting

- Apple event.

- Canaccord Global Metals & Mining Conference

- Houlihan Lokey Global Industrials Conference

- HSBC Mexico Opportunities Forum

- Jamaica Mining Conference

- Jefferies Reduced Risk Seminar

- Offshore Technology Conference

- Oppenheimer Industrial Growth Conference

- Raymond James Lodging Tour

- Spinal Cord Injury Investor Symposium

- Waste Expo

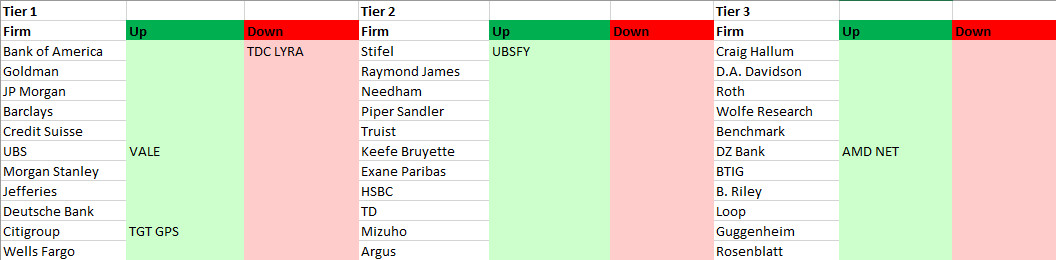

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades: