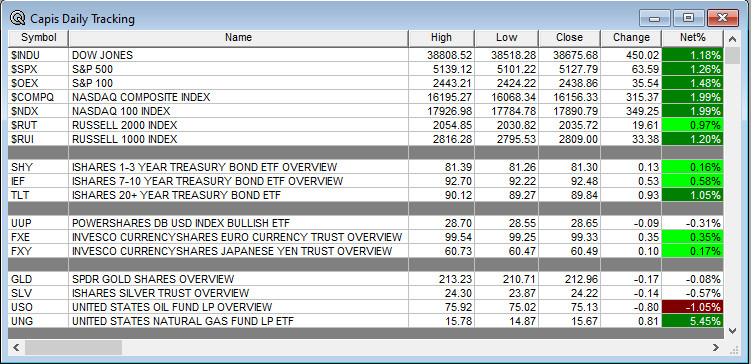

Overnight Summary: The SP 500 closed Friday higher by 1.26% at 5127.79 from Thursday higher by 0.91% at 5064.20. The overnight high was hit at 5,174.75 at 7:00 p.m. while the overnight low was hit at 5155.75 at 1:35 p.m. EDT. The range overnight is 19 points as of 7:15 a.m. EDT. Currently, the S&P 500 is higher by +16.50 points at 7:25 a.m. EDT.

Executive Summary:

- 3-6 month Treasury Auctions.

- Fed Speakers Larkin and Williams at 12:50 p.m. EDT and 1:00 p.m. EDT.

Earnings Out After The Close:

- Beats: None of note. (Greater than +0.10)

- Flat: None of note.

- Misses: None of note.

- IPOs For The Week: ALEH KMCM NNE RAN ZENA.

- New SPACs launched/News:

- Secondaries Priced:

- Notes Priced of note:

- Common Stock filings/Notes:

- LOT files a 15.037,030 ADS offering, also files 680,957,495 ADS offering, relates to warrants.

- Direct Offering:

- Exchangeable Subordinate Voting Shares:

- Selling Shareholders of note:

- NDAQ files 85,608 by a selling shareholder.

- LILM files 75 million by selling shareholder.

- Debt/Credit Filing and Notes: .

- Mixed Shelf Offerings:

- ABR files mixed-shelf offering

- BNL files a mixed-shelf offering

- LAZR files a mixed-shelf offering

- PTPI files a $100M mixed-shelf offering

- YTEN files a $100 million mixed-shelf offering.

- Tender Offer:

- Private Placement of Public Entity (PIPE)

- Rights Offering:

- Convertible Offering & Notes Filed:

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

- Movers of Note:

- News Items After the Close:

- ABBV to invest $161 million in new R&D site in Germany. (Endpoint News)

- WHR to increase workforce reduction and will cost $52 to $57 million.

- UAL and AAL sign off on proposed changes to O’Hare after pushing back on rebuild. (Chicago Tribune)

- CBOE files its April trading stats. (Release)

- LAZR filed a mixed-shelf offering and then laid off 20% of workforce.

- VST to replace PXD in the S&P 500. AAON to replace VST in the S&P 400. MARA to replace AAON in S&P 600 on Wednesday, May 8th.

- Boeing (BA) awarded $461 million contract with the U.S. Missile Defense Agency.

- AT&T (T) wins award for $267 million U.S. Navy wireless service contract with other wireless companies.

- Adtran (ADTN) to take a $293 million goodwill impairment charge.

- News Over The Weekend:

- Barron’s: + on MTZ URI EQIX VTR ETR DUK SHW ADBE

- Barron’s -/cautious on: CVS

- Buyback Announcements or News

- Exchange/Listing/Company Reorg and Personnel News

- Stock Splits or News:

- Dividends Announcements or News:

- CNO see dividend increase to $0.16 from $0.15.

- MAN sees dividend increase by 4.8% to $1.54.

What’s Happening This Morning: Futures value reflects the change with fair value.

S&P 500 +16.50, Dow Jones +124, NASDAQ +41, Russell +18.88. (as of 8:15 a.m. EDT). Asia is lower ex Australia while Europe is higher this morning. VIX Futures are at +14.40 from +15.30. Gold, Silver and Copper are higher this morning. WTI Crude Oil and Brent Crude Oil are higher with Natural Gas higher as well for a third day in a row. US 10-year Treasury sees its yield at 4.48% from 4.561% yesterday. The U.S. Dollar is lower versus the Euro, lower versus the Pound and higher against the Yen. Bitcoin is at $64,284 from $59,176 higher by +0.62% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

- Daily Positive Sectors: Technology, Utilities, Materials, Consumer Cyclicals and Communication Services of note.

- Daily Negative Sectors: None of note.

- One Month Winners: Consumer Defensive,Communication Services,

Energy and Utilities of note.

- Three Month Winners: All but Real Estate led by Energy,

Industrials, Materials and Communication Services of note.

- Six Month Winners: Communication Services, Technology, Industrials and Financials of note.

- Twelve Month Winners: Communication Services, Technology, Financials, Industrials, and Consumer Cyclicals of note.

- Year to Date Winners: Communication Services, Energy, Technology, Financials, Industrials, and Technology, Consumer Defensive of note.

(WSJ – Edited by QPI)

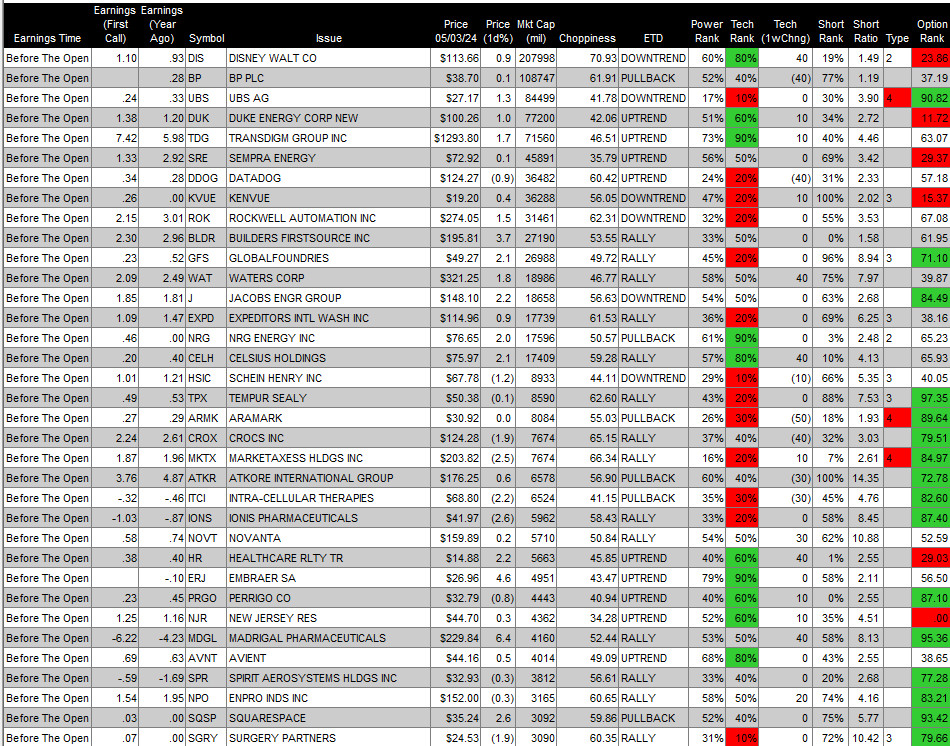

Upcoming Earnings Of Note:

- Monday After the Close: ($3 Billion Market Cap Cut Off)

- Tuesday Before the Open: ($3 Billion Market Cap Cut Off)

Earnings of Note This Morning:

- Beats: JLL +0.92, FRPT +0.59, BCRX +0.04, SHO +0.02 of note.

- Flat: IART of note.

- Misses: AMR -1.23, AMG -1.05, PRFT -0.20, CNA -0.10, NWN -0.08, BNTX -0.07, THS -0.02, SAVE -0.01 of note.

- Still to Report: of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative Guidance: None of note.

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: PRFT +52.8%, ADCT +30.4%, VST +5%, CLLS +4%, L +4%, URGN +3.2% of note.

- Gap Down: GLYC -56.9%, LAZR -8.9%, IART -6.5%, SAVE -5.7%, PAC -2.3% of note.

Insider Action: No stocks sees Insider buying with dumb short selling. No stocks see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- 5 Things To Know Before The Market Opens On Monday. (CNBC)

- What You Need To Know To Start Your Day. (Bloomberg)

- Stocks Making the Biggest Moves: (CNBC)

- Bloomberg Lead Story: Israel Tells Civilians to Leave Rafah as Weighs Its Attack. (Bloomberg)

- Stocks rally as confidence in Fed wagers grow: Markets Wrap. (Bloomberg)

- Warren Buffet weighs in on Berkshire Hathaway and his mortality this weekend. (CNBC)

- Why fast food prices have exceeded inflation rates. (CNBC)

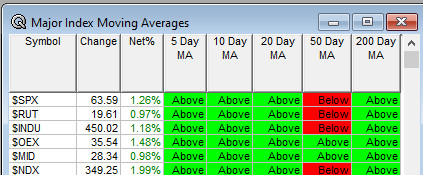

Moving Average Update: Score moves to 87% from 63%.

Geopolitical:

- President’s Public Schedule:

- President Biden receives the Daily Briefing at 9:00 p.m. EDT.

- President Biden arrives back at the White House at 11:00 a.m. EDT.

- President Biden presents the Commander-in-Chief’s Trophy to West Point at 12:00 p.m. EDT.

- President Biden has lunch with King Abdullah II of Jordan at 1:00 p.m. EDT.

- Press Briefing with Press Secretary Karine Jean-Pierre at 1:30 p.m. EDT.

- President Biden and The First Lady host a Cinco De Mayo reception at the White House at 5:15 p.m. EDT.

Economic:

Federal Reserve / Treasury Speakers:

- Federal Reserve Richmond President Tom Larkin speaks at 12:50 p.m. EDT.

- Federal Reserve New York President John Williams speaks at 1:00 p.m. EDT.

M&A Activity and News:

Meeting & Conferences of Note:

- Sellside Conferences:

- Top Shareholder Meetings: AXP AFL CVNA HSY LLY MRNA MAIN PBI PHM UBER

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: CTSO FAST ENVX NOW RA

- Update: None of note.

- R&D Day: None of note.

- FDA Presentation:

- Company Event:

- Industry Meetings:

- AANS Scientific Meeting

- American Urological Association Annual Meeting

- Association for Research in Vision and Ophthalmology

- American Association of Immunologists

- Meeting of American Association of Immunologists

- Offshore Technology Conference

- Oppenheimer Industrial Growth Conference

- Spinal Cord Injury Investor Symposium

- Stifel Investor Conference

- Waste Expo

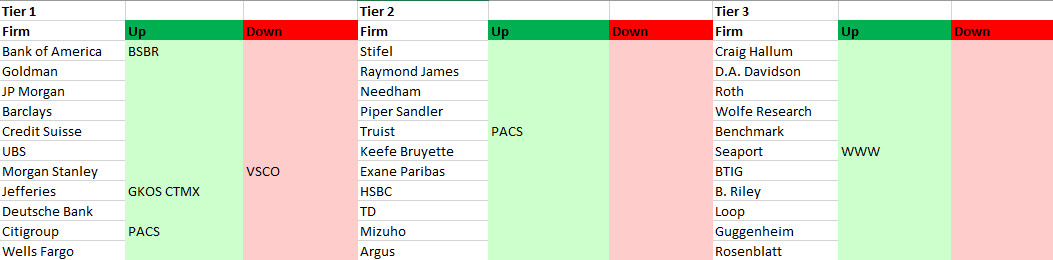

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades: