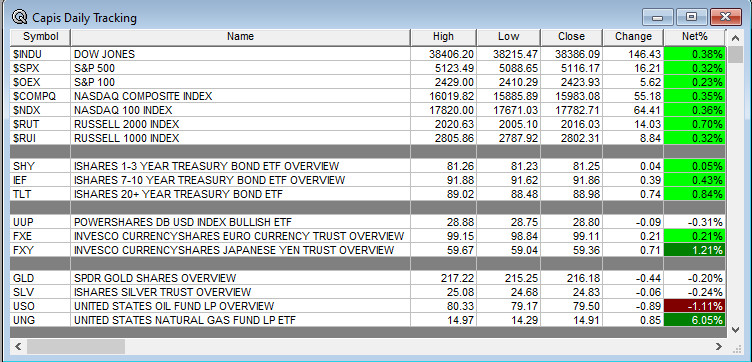

Overnight Summary: The SP 500 closed Monday higher by 0.32% at 5116.17 from Friday higher by 1.02% at 5099.96. The overnight high was hit at 5,151.50 at 4:05 p.m. while the overnight low was hit at 5135.25 at 1:45 a.m. EDT. The range overnight is 16 points as of 6:15 a.m. EDT. Currently, the S&P 500 is lower by -3.75 points at 8:25 a.m. EDT.

Executive Summary: All eyes are on Wednesday’s Federal Reserve Open Market Committee (FOMC) announcement and press conference.

- Several economic releases are due out including Case-Shiller, Chicago PMI and Consumer Confidence.

- The Fed begins its FOMC with no commentary of note.

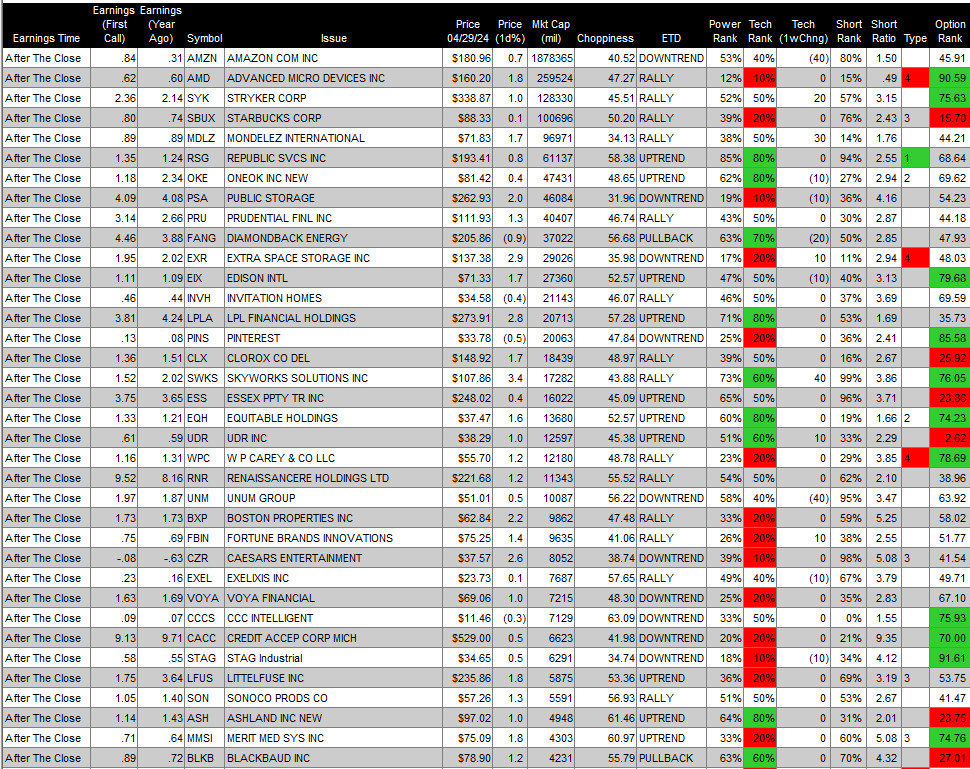

Earnings Out After The Close:

- Beats: EG +0.39, ACGL +0.36, WWD +0.29, PARA +0.27, AMKR +0.13, RIG +0.12, FLS +0.11, WELL +0.07, COUR +0.06, CCK +0.06, YUMC +0.06, MSA +0.05, NXPI +0.05, SANM +0.05, FFIV +0.04, ST +0.04, AIN +0.03, BRX +0,03, of note.

- Flat: KFRC and LSCC of note.

- Misses: MSTR -2.45, PCH -0.45, RMBS -0.14, CVI -0.14, CNO -0.13, MED -0.12, SBAC -0.02 of note.

- IPOs For The Week: ALEH KMCM NNE RAN VIK ZENA

- New SPACs launched/News:

- Secondaries Priced:

- MBIO prices $4M of 16,877,638 @$0.237.

- Notes Priced of note:

- Common Stock filings/Notes:

- ALCE files 35,575,274 shares of common stock.

- Direct Offering:

- Exchangeable Subordinate Voting Shares:

- Selling Shareholders of note:

- DCTH files 1,918,140 shares of common stock offered by selling shareholders.

- Debt/Credit Filing and Notes:

- Mixed Shelf Offerings:

- RSVR files a $100 million mixed-shelf offering

- CHRW files a mixed-shelf offering

- Tender Offer:

- Private Placement of Public Entity (PIPE)

- Rights Offering:

- Convertible Offering & Notes Filed:

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close :

- Movers of Note:

- News Items After the Close:

- Fluor (FLR) and SunCoke Energy (SXC) extend contract seven years at its five coke plants in the U.S.

- Rocket Lab USA (RKLB) prepares to back to back Electron launches to deploy NASA’s PREFIRE mission.

- Exchange/Listing/Company Reorg and Personnel News:

- PARA President and CEO Bob Bakish is stepping down from CEO role and from the Board of Directors.

- Nathan Schultz named CEO and Dan Rosensweig becomes Executive Chairman of Chegg (CHGG).

- Paul Donahue will transition from Chairman and CEO of Genuine Parts (GPC) to Executive Chairman and William Stengel to succeed him as President and CEO.

- Buyback Announcements or News:

- Stock Splits or News:

- Stock splits for week BKKT and RCON.

- Dividends Announcements or News:

What’s Happening This Morning: Futures value reflects the change with fair value.

S&P 500 -3.92, Dow Jones -23, NASDAQ -18.47, Russell -7.03. (as of 8:15 a.m. EDT). Asia is higher while Europe is lower ex the FTSE this morning. VIX Futures are at 15.33 from 15.63. Gold, Silver and Copper are lower this morning. WTI Crude Oil and Brent Crude Oil are higher with Natural Gas higher as well. US 10-year Treasury sees its yield at 4.63% from 4.624% yesterday. The U.S. Dollar is lower versus the Euro, higher versus the Pound and higher against the Yen. Bitcoin is at $61,487 from $62,310 lower by -1.97% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

- Daily Positive Sectors: Consumer Cyclical, Utilities, Real Estate and Materials of note.

- Daily Negative Sectors: Utilities, Energy and Financials of note.

- One Month Winners: Communication Services, Energy and Utilities of note.

- Three Month Winners: All but Real Estate led by Energy, Industrials or Communication Services of note.

- Six Month Winners: Communication Services, Technology, Industrials and Financials of note.

- Twelve Month Winners: Communication Services, Technology, Financials, Industrials, and Consumer Cyclicals of note.

- Year to Date Winners: Communication Services, Energy, Technology, Financials, Industrials, and Technology, Consumer Defensive of note.

(WSJ – Edited by QPI)

Upcoming Earnings Of Note:

- Tuesday After the Close: ($4 Billion Market Cap Cut Off)

- Wednesday Before the Open: ($5 Billion Market Cap Cut Off)

Earnings of Note This Morning:

- Beats: THC +1.77, IT +0.40, ZBRA +0.40, MMM +0.29, TT +0.29, MPC +0.24, AMT +0.22, TAP +0.21, LEA +0.17, APD +0.15, ETN +0.11, LLY +0.11, ADM +0.09, EAT +0.09, MLM +0.09, GLW +0.03, AEP +0.02, KO +0.02, PNM +0.01, QSR +0.01 of note.

- Flat: of note..

- Misses: LGIH -0.34, ARCB -0.19, PAG -0.16, INCY -0.16, DAN -0.16, CCJ -0.13, HEES -0.07, MAC -0.06, MCD -0.02, EPD -0.01 of note.

- Still to Report: BEN HOPE of note.

Company Earnings Guidance:

- Positive Guidance: WWD TT AWI LLY CCJ of note.

- Negative Guidance: COUR SANM CHGG MED LSCC of note.

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: BLND +19.6%, ST +15.9%, LL +11%, AMKR +6.5%, LOGI +6.5%, LDOS +6.4%, WWD +5.9%, AUPH +5.6%, HLIT +4.3%, NXPI +4%, HSBC +4%, TERN +3.9%, TT +3.1%, TWO +2.9%, LCTX +2.7%, ACIW +2.7%, MOR +2.5%, CCK +2.3%, RIG +1.9% of note.

- Gap Down: MED -15.5%, COUR -13.3%, CHGG -12.6%, FFIV -9.8%, LSCC -6.6%, MSTR -5.8%, GEHC -5.6%, YUMC -5.1%, ESI -4.8%, RMBS -4.1%, SAN -3.4%, DCTH -3.3%, STLA -3%, SBAC -2.8%, ALVO -2.3%, SANM -2.3%, RSVR -2%, CNO -2% of note.

Insider Action: No stock sees Insider buying with dumb short selling. No stocks see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- 5 Things To Know Before The Market Opens On Tuesday. (CNBC)

- What You Need To Know To Start Your Day. (Bloomberg)

- Stocks Making the Biggest Moves: (CNBC)

- Bloomberg Lead Story: BOJ Accounts Suggest Japan Intervened To Support the Yen. (Bloomberg)

- April Factory Activity in China expanded. (Bloomberg)

- Stocks set for monthly drop as traders wait for Fed : Markets Wrap. (Bloomberg)

- Bloomberg: Daybreak Podcast: HSBC CEO Noel Quinn to retire after 5 years. (Podcast)

Moving Average Update: Score improves to 77% from 57%.

Geopolitical:

- President’s Public Schedule:

- President Biden receives the Daily Briefing at 10:00 a.m. EDT.

- President Biden heads to Wilmington, DE for a campaign event at 3:00 p.m. EDT.

- President Biden returns to the White House at 7:20 p.m. EDT.

Economic:

- February Case-Shiller Home Price Index is due out at 9:00 a.m. EDT and expected to rise to 6.70% from 6.60%.

- April Chicago PMI is due out at 9:45 a.m. EDT and is expected to rise to 44.5 from 41.40.

- April Consumer Confidence is due out at 10:00 a.m. EDT and is expected to fall to 104 from 104.70.

Federal Reserve / Treasury Speakers:

- No Fed Speakers as in the Blackout Period due to this week’s FOMC meeting.

- Federal Reserve Open Market Committee (FOMC) begins a two day meeting.

M&A Activity and News:

Meeting & Conferences of Note:

- Sellside Conferences:

- Top Shareholder Meetings: ABEV C EXC FMC FR GLPG IBM KN MT PCAR PLNT SNY VICI VSAC WMB WFC TS TX X.

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: AXP AZN BCDA DAWN LQDA MACE MITI MRNA NBIX PWFL XFOR XOMA

- Update: None of note.

- R&D Day: None of note.

- Company Event:

- Industry Meetings:

- Jefferies Macro Summit

- Longwood Healthcare Leaders Conference

- NSBW Summit

- SBA Virtual Summit

- Spinal Cord Injury Investor Symposium

- Women in Data Science Conference

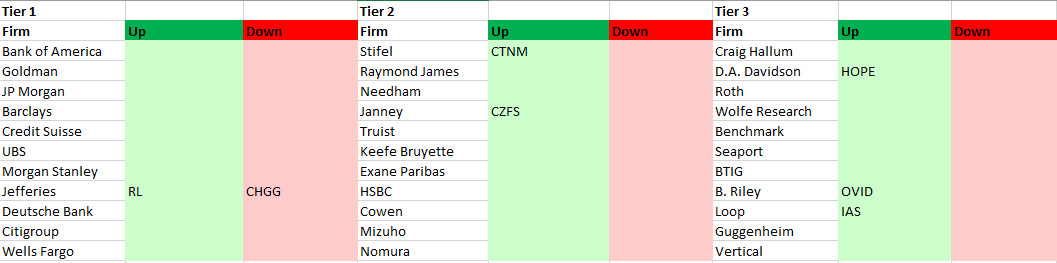

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades: