Overnight Summary: The SP 500 closed higher Friday. The overnight high was hit at 5,147 at 10:00 p.m. while the overnight low was hit at 5134.50 at 5:20 a.m. EDT. The range overnight is 13 points as of 7:00 a.m. EDT. Currently, the S&P 500 is higher by +10.50 points at 7:00 a.m. EDT.

Executive Summary: All eyes are on Wednesday’s Federal Reserve Open Market Committee (FOMC) announcement and press conference. There could be a lift into this catalyst.

- Dallas Fed Manufacturing Survey at 10:30 a.m. EDT.

- Treasury holds 3 & 6-month auctions at 11:30 a.m. EDT.

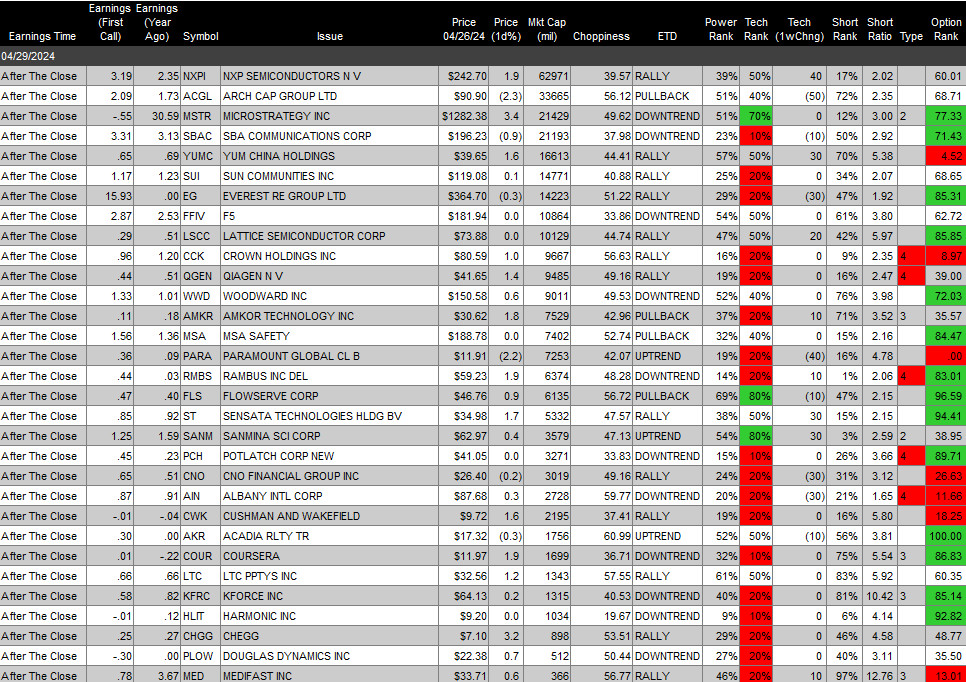

Earnings Out After The Close:

- Beats: None of note.

- Flat: None of note.

- Misses: None of note.

- IPOs For The Week: ALEH KMCM NNE RAN VIK ZENA

- New SPACs launched/News:

- Secondaries Priced:

- Notes Priced of note:

- Common Stock filings/Notes:

- OPHC files 1,381,025 shares of common stock.

- RNXT files 6,960, 864 shares of common stock.

- Direct Offering:

- Exchangeable Subordinate Voting Shares:

- Selling Shareholders of note:

- TDAM files 1,069,272 shares of common stock offered by selling shareholders.

- OTLK files 2,776,867 shares of common stock offered by selling shareholders.

- ACHV files 13,086,151 share of common stock offered by selling shareholders.

- EDBL files 2,396,168 units.

- Private Placement of Public Entity (PIPE):

- Mixed Shelf Offerings:

- HPP files a mixed-shelf offering.

- MORF files a mixed-shelf offering.

- TREE files a $150 million mixed-shelf offering.

- SQFT files $50 million mixed-shelf offering.

- Debt/Credit Filing and Notes:

- Tender Offer:

- Rights Offering:

- Convertible Offering & Notes Filed:

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close :

- Weekly Movers of Note:

- Healthcare RMD +22%, CYT +20%, MESO +20% Industrials TPC +33%, Expo +22% Consumer SAH +25%, STRA +23%, GRPN +22% Tech PI +28%, GDS +22%, RBBN +22%, TER +19% Financials RLY +85%, STI +66% Energy SLCA +22%.

- Healthcare ABEO -56%, FATE -21%, ALLO -17%, GLYC -13% Industrials NCI -99%, HTZ -26%, JBLU -19%, TNET -16%, SAIA -16%, ODFL -14% Consumer BYD -15%, PLCE -14% Financials KNSL -15% Energy OIS -22%, NINE -15%.

- News Items After the Close:

- AMC guides Q1 earnings and revenues above consensus.

- UMBF seeks to acquire Heartland (HTLF) in largest regional bank merger of the year. (Bloomberg)

- Amazon (AMZN) Prime has framework for a deal to include regular and post season NBA games. (The Athletic)

- Northrop Grumman (NOC) awarded a $388 million US Airforce contract.

- Barrons Highlights:

- Positive: BRKB, BKR, JPM, META, UNH, META, WMT, TRP

- Negative: CLF

- Exchange/Listing/Company Reorg and Personnel News:

- CYTK names Sung H. Lee as CFO as of May 8th.

- SAIA CFO Douglas L. Col to retire once successor named.

- Buyback Announcements or News:

- Stock Splits or News:

- Stock splits for week BKKT and RCON.

- Dividends Announcements or News:

What’s Happening This Morning: Futures value reflects the change with fair value.

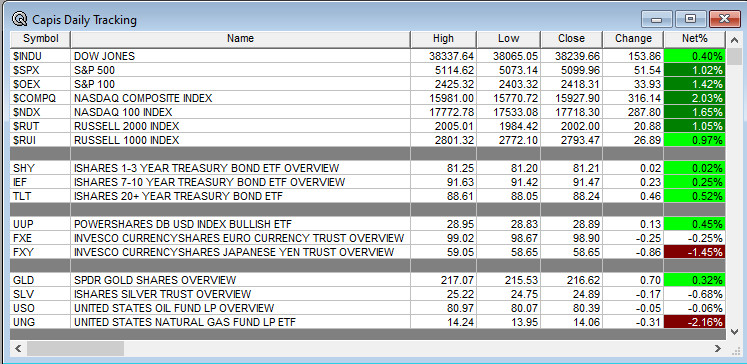

S&P 500 +12, Dow Jones +59, NASDAQ +62, Russell +6. (as of 8:15 a.m. EDT). Asia is higher while Europe is higher ex Germany this morning. VIX Futures are at 15.33 from 15.63. Gold, Silver and Copper are higher this morning for a second trading day. WTI Crude Oil and Brent Crude Oil are lower with Natural Gas higher. US 10-year Treasury sees its yield at 4.624% from 4.69% from Friday. The U.S. Dollar is lower versus the Euro, lower versus the Pound and lower against the Yen. Bitcoin is at $62,310 from $64,188 lower by -2.26% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

- Daily Positive Sectors: Communication Services, Technology, Consumer Cyclical, Materials of note.

- Daily Negative Sectors: Utilities, Energy and Financials of note.

- One Month Winners: Communication Services, Energy and Utilities of note.

- Three Month Winners: All but Real Estate led by Energy, Industrials or Communication Services of note.

- Six Month Winners: Communication Services, Technology, Industrials and Financials of note.

- Twelve Month Winners: Communication Services, Technology, Financials, Industrials, and Consumer Cyclicals of note.

- Year to Date Winners: Communication Services, Energy, Technology, Financials, Industrials, and Technology, Consumer Defensive of note.

(WSJ – Edited by QPI)

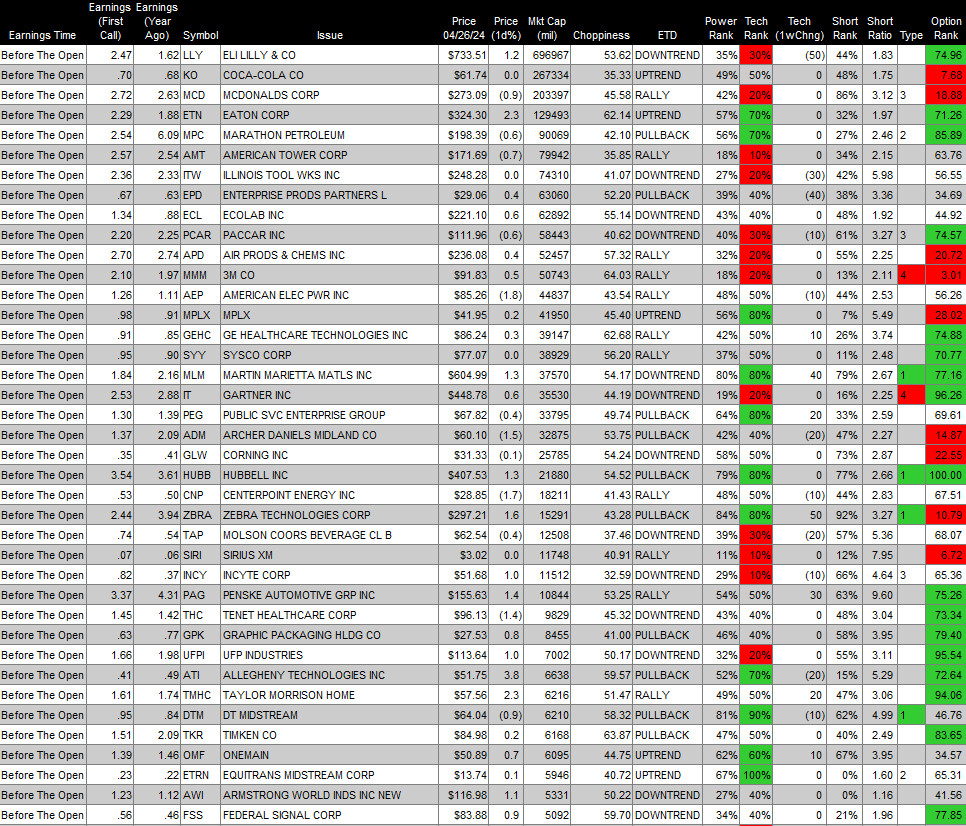

Upcoming Earnings Of Note:

- Tuesday Before the Open: ($5 Billion Market Cap Cut Off)

Earnings of Note This Morning: (Greater Than $0.10 and Lower Than $-0.00)

- Beats: JKS +0.60, UMB +0.45, HNI +0.19, DPZ +-0.18, HTLF +0.11, ON +0.04, RVTY +0.04, SOFI +0,01 of note.

- Flat: PHG of note.

- Misses: of note.

- Still to Report: BEN HOPE of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative Guidance: ON of note.

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: PHG +40.8%, XFOR +13.3%, TSLA +9.1%, MNKD +8.5%, KIND +7.9%, DPZ +6%, ARLP +3.8%, ACHV +3.5%, LSXMA +2.3%, ATHE +2% of note.

- Gap Down: ADXN -53.7%, DB -6.7%, TGAN -4.1%, OTLK -3.4%, TREE -2.6%, MORF -2% of note.

Insider Action: No stock sees Insider buying with dumb short selling. CTRN STCN sees Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- 5 Things To Know Before The Market Opens On Monday. (CNBC)

- Stocks Making the Biggest Moves: TSLA LUV DPZ PARA APPL (CNBC)

- Bloomberg Lead Story: Elon Musk and Tesla Leave China With a Big Victory. (Bloomberg)

- Chinese President Xi to make first trip to Europe since 2019. (Bloomberg)

- Philips (PHG) settles sleep apnea claims. (Bloomberg).

- Earnings keep stocks aloft at start of Fed week: Markets Wrap. (Bloomberg)

- Bloomberg: Daybreak Podcast: Yen briefly passes 160 Yen per Dollar. (Podcast)

- Bloomberg: The Big Take: How The Freedom of Information Act unlocks Government Secrets. (Podcast)

- Marketplace: Atlas gives way to the next generation of robots. (Podcast)

- NY Times Daily: What a Second Trump Presidency would bring. (Podcast)

- Wealthion: Market Chaos with Jon Najarian of Market Rebellion. (Podcast)

- Adam Taggart’s Thoughtful Money: The new era of fiscal dominance. (Podcast)

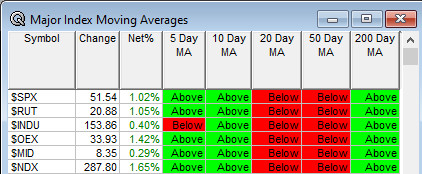

Moving Average Update: Score improves to 57% from 50%.

Geopolitical:

- President’s Public Schedule:

- President Biden receives the Daily Briefing at 10:00 a.m. EDT.

- Press Briefing at 2:00 p.m. EDT held by Press Secretary Karine Jean-Pierre.

Economic:

- Dallas Fed Manufacturing Survey at 10:30 a.m. EDT.

Federal Reserve / Treasury Speakers:

- No Fed Speakers as in the Blackout Period due to this week’s FOMC meeting.

M&A Activity and News:

Meeting & Conferences of Note:

- Sellside Conferences:

- Top Shareholder Meetings: AND, BLD, FLNG, GOGL, PAYC, SAND, SNDR.

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls:

- Update: None of note.

- R&D Day: None of note.

- Company Event:

- Industry Meetings:

- Gulf South Bank Conference

- Longwood Healthcare Leaders Conference

- LSX World Congress

- Spinal Cord Injury Investor Symposium

- Women in Data Science Conference

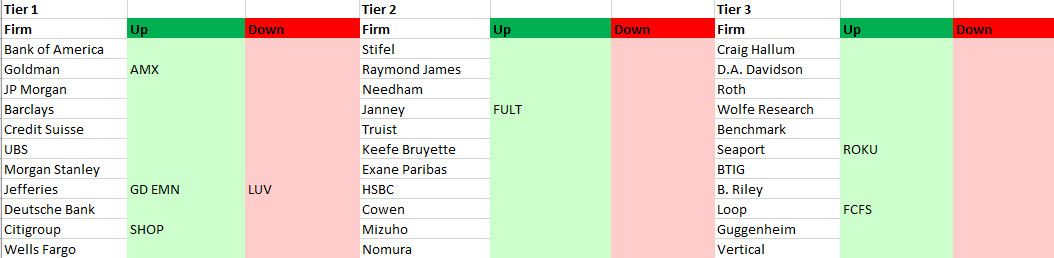

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades: