Overnight Summary: The S&P 500 closed Wednesday higher by 0.14% at 4781.58 from Tuesday higher by 0.42% at 4774.75. The overnight high was hit at 4841 at 3:30 a.m. EST while the low was hit at 4831 at 7:15 a.m. EST. The range overnight was 10 points as of 7:25 a.m. EST identical to yesterday. The 10-day average of the overnight range is at 15.10 from 16.40. The average for May-November average was 21.43 from 22.06. Currently, the S&P 500 is higher by 0.50 at 7:35 a.m. EST.

Breaking News: None of note.

Executive Summary: Happy New Year!! Look for volatility to return next week as players come back to their desks.

- NYSE Short Interest Rose 0.95%. NASDAQ Short Interest Fell by -0.16%

Earnings Out After The Close:

- Beats: None of note.

- Flat: None of note.

- Misses: None of note.

- IPOs Priced or News: None of note.

- New SPACs launched/News:

- Secondaries Priced: None of note.

- Notes Priced of note: None of note.

- Common Stock filings/Notes:

- ASPS files a S-3 of 1,611,889 shares of common stock.

- GEO files a $300M offering of common shares.

- Direct Offering: None of note.

- Selling Shareholders of note: None of note.

- NVRO sees selling shareholders file a 2,587,742 shares of common stock.

- Private Placement of Public Entity (PIPE): None of note.

- Mixed Shelf Offerings:

- BSGM Filed 75,000,000 mixed shelf securities offering.

- LQDA Filed a $200M mixed shelf securities offering.

- Debt/Credit Filing and Notes: None of note.

- Tender Offer: None of note. None of note.

- Convertible Offering & Notes Filed: None of note.

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close and Over the Weekend:

- News Items After the Close:

- Gilead Sciences (GILD) takes a 12.9% passive stake in Arcellex (ACLX) from 7.3%.

- Erlanger Type 1 Short Squeezes and Type 4 Long Squeezes reporting earnings this week:

- Exchange/Listing/Company Reorg and Personnel News:

- BCB Bancorp (BCBO) announces that Michael Shriner will become the next President and CEO while Thomas Coughlin the last President will continue to serve on the Board of Directors.

- Buyback Announcements or News:

- Stock Splits or News: None of note.

- After The Close Movers:

- Ups: ALRM+2.2%, BSX +1.5%.

- Downs: None of note.

- Dividends Announcements or News:

- SM Energy (SM) increases its quarterly dividend to $0.18 from $0.15.

- Insider Sales Of Note: None of note.

What’s Happening This Morning: Futures value reflects the change with fair value.

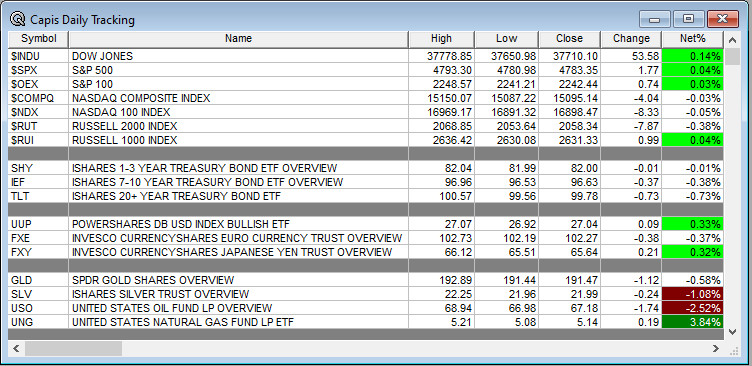

S&P 500 +1.50, Dow Jones +19, NASDAQ -3.75, and Russell 2000 -1.34. (as of 8:15 a.m. EST). Asia is lower ex South Korea and Europe is higher this morning. VIX Futures are at 13.98 from 13.90 this morning. Gold, Silver and Copper are lower this morning for a second day in a row. WTI Crude Oil and Brent Crude Oil are higher with Natural Gas lower. US 10-year Treasury sees yields at 3.883% from 3.813% from yesterday. The U.S. Dollar is lower versus the Euro, flat versus the Pound and higher against the Yen. Bitcoin is at $42,793 from $42,903 higher by +0.70% this morning.

Sector Action – (1/3/6/12/YTD Updated Daily this week):

- Daily Positive Sectors: Utilities, Real Estate, Financials, Healthcare and Technology were higher yesterday.

- Daily Negative Sectors: Energy, Materials and Consumer Cyclicals of note.

- One Month Winners: Real Estate, Materials, Industrials, Consumer Cyclicals, Financials of note.

- Three Month Winners: Technology, Real Estate, Industrials, Consumer Cyclicals and Materials of note.

- Six Month Winners: Communication Services, Financial, Technology, Energy and Consumer Cyclical of note.

- Twelve Month Winners: Technology, Communication Services, Consumer Cyclicals and Industrials of note.

- Year to Date Winners: Technology, Communication Services, Industrials and Financials of note.

Stocks inched higher Thursday, putting the S&P 500 on pace for its longest weekly winning streak in nearly 20 years. The broad index gained 0.04. The tech-heavy Nasdaq Composite fell 0.03, while the Dow Jones Industrial Average rose 0.1%, or 54 points. Markets are ending 2023 on a hot streak. All three indexes are on pace for a ninth consecutive weekly gain. For the S&P 500, that would mark the longest streak since January 2004. The index is now within 0.3% of its all-time high, set in January 2022. With one trading session remaining in 2023, the S&P 500 is up 25%.

Optimism that the Federal Reserve can successfully cool inflation without inducing a major economic slowdown has powered the market’s recent advance. Now, some investors say the looming end of the calendar year is giving markets an extra boost. “Nobody who has caught this rally wants to incur a taxable event,” said Michael Green, chief strategist at Simplify Asset Management. “If nobody wants to sell, prices will push higher on low volume.”

Stocks often rise at year-end because investors typically wait to sell stocks that have appreciated to avoid paying taxes. Trading volume is usually lower near the holidays, which can exacerbate market moves. Initial jobless claims, considered a proxy for layoffs, were 218,000 in the week ending Dec. 23, the Labor Department said Thursday. That was slightly more than the 215,000 that economists expected, and marked the latest sign that the economy is cooling at a gradual pace.

“As the data has come in this year, you have to acknowledge that the soft landing probability has increased,” said Matt Dmytryszyn, chief investment officer at Telemus Capital. “But a lot is still to be determined” regarding the economy’s ultimate fate. He said his fund is boosting its position in shares of energy and industrial firms. Bond yields rose as prices fell. The yield on the benchmark 10-year Treasury note rose to 3.849%, up from 3.788% Wednesday. The average rate on a 30-year fixed mortgage dropped to 6.61%, down more than a percentage point from a 23-year high of 7.79% in late October, according to data released by mortgage giant Freddie Mac on Thursday. The rate has declined for nine consecutive weeks.

Crude oil prices fell 3.2% to settle at $71.77 a barrel. The S&P 500 energy sector slipped 1.5%. Gold futures fell 0.5%, snapping a four-session winning streak.

The S&P 500’s top performer Thursday was Match Group, which advanced 2.6%. Tesla was the index’s biggest laggard, dropping 3.2%. In overseas trading, Asian stocks rallied after Beijing appeared to soften a crackdown on videogame makers, which roiled markets last week. Hong Kong’s Hang Seng Index rose 2.5% and the Shanghai Composite gained 1.4%.

(WSJ – edited by QPI)

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Thursday After the Close: None of note

- Friday Before the Open: None of note.

Earnings of Note This Morning:

- Beats: None of note.

- Flat: None of note.

- Misses: None of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Mixed Guidance: None of note.

- Negative Guidance: None of note.

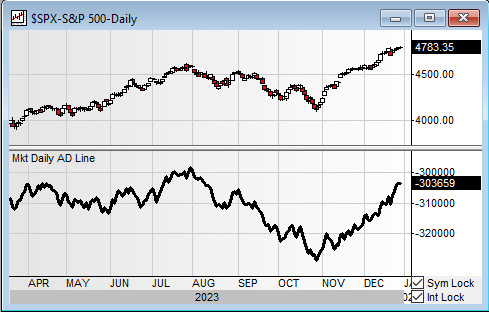

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market:

- Gap Up: FLJ+53%, FSR +15% of note.

- Gap Down: LYFT -4% of note.

Insider Action: Several stocks sees Insider buying with dumb short selling (rating of 4 or 5). FDX see Insider buying with smart short sellers (rating of 1 to 3).

Rags & Mags.: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Stocks making the biggest moves before the bell: LYFT NVDA UNH BSX UBER (CNBC)

- What You Need To Know To Start Your New Year. (Bloomberg)

- Bloomberg Lead Story: Maine Bars President Trump from Primary Ballot. (Bloomberg)

- Bloomberg Second Most Shared Story: L’Oreal Heiress Francoise Bettencourt becomes first woman worth $100 billion. (Bloomberg)

- Stocks set for last hurrah as the year draws to a close: Market Wrap. (Bloomberg)

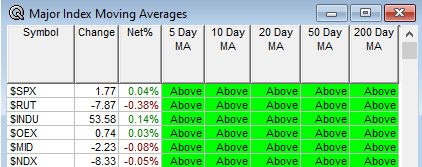

Moving Average Update:

Geopolitical:

- President’s Public Schedule:

- President Biden has no public events scheduled.

- President Biden and The First Lady are inthe U.S. Virgin Islands for a little R&R.

Economic:

- December Chicago PMI is due out at 9:45 a.m. EST and is expected to come in at 50.0 from 55.80.

- Baker Hughes Rig Count is due at 1:00 p.m. EST.

Federal Reserve / Treasury Speakers: None of note.

M&A Activity and News:

- Kadant (KAI) to buy Key Knife for $156 million.

Meeting & Conferences of Note:

- Sellside Conferences: None of note.

-

- Previously posted and ongoing conferences: None of note.

- Top Shareholder Meetings: None of note.

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: None of note.

- Update: None of note.

- R&D Day: None of note.

- Company Event: None of note.

- Industry Meetings: None of note.

- Previously posted and ongoing conferences: None of note.

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades:

Previous Day’s Upgrades and Downgrades: