There will be no note on Tuesday, December 26 but we will be in production Wednesday through Friday next week.

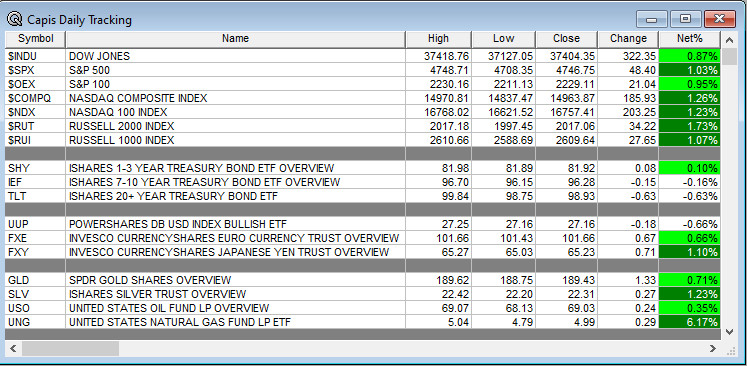

Overnight Summary: The S&P 500 closed Thursday higher by 1.03% at 4746.75 from Wednesday lower by -1.47% at 4698.35. The overnight high was hit at 4797.75 at 4:30 p.m. EST while the low was hit at 4785.50 at 1:20 a.m. EST. The range overnight was 12 points as of 7:15 a.m. EST. The 10-day average of the overnight range is at 16.60 from 16.80. The average for May-November average was 21.43 from 22.06. Currently, the S&P 500 is lower by -1 at 7:15 a.m. EST.

Breaking News:

Executive Summary: The S&P 500 gained back 1.03% after losing 1.47% Wednesday and it is now higher for the week by 0.58%. Lack of follow-through supports the bullish bias to the market.

- See Economic Section as 5 releases today!!

- Nike is lower despite beating estimates.

Earnings Out After The Close:

- Beats: NKE +0.19, AIR +0.01, AVO +0.01 of note.

- Flat: None of note.

- Misses: WS -0.04 of note.

- IPOs Priced or News: None of note.

- New SPACs launched/News:

- Secondaries Priced: None of note.

- Notes Priced of note: None of note.

- Common Stock filings/Notes:

- PIXY files a S-1 common stock offering of 94,375 shares.

- PSNL files a S-3 common stock offering of 9,218,800 shares.

- TRNR files a S-1 common stock offering of 12,480,480 shares.

- SSTK files a stock offering.

- Direct Offering: None of note.

- Selling Shareholders of note: None of note.

- Private Placement of Public Entity (PIPE): None of note.

- Mixed Shelf Offerings:

- AMPE: Files mixed shelf securities offering.

- GP: Files a $20M mixed securities shelf offering.

- PSNL: Files a $200M mixed shelf securities offering.

- Debt/Credit Filing and Notes: None of note.

- Tender Offer: None of note. None of note.

- Convertible Offering & Notes Filed: None of note.

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close and Over the Weekend:

- News Items After the Close:

- Stifel Financial (SF) sees client assets grow 7.7% to $427.8 billion.

- Rocket Lab (RKLB) to make 18 space vehicles at cost of $515 million.

- Becton Dickinson (BDX) agrees to $85 million settlement on previously announced class action related to infusion pumps.

- Erlanger Type 1 Short Squeezes and Type 4 Long Squeezes reporting earnings this week:

- Exchange/Listing/Company Reorg and Personnel News:

- Marathon Petroleum (MPC) announces CFO Maryann T. Mannen appointed President and John J. Quaid to be next CFO.

- MPLX names C. Kristopher Hagedorn as CFO at year end.

- Credicorp LTD (BAP) names multiple changes at officer level including a new CRO Cesar Rios Briceno, CFO Alejandro Perez- Reyes Zarak.

- C.H. Robinson (CHRW) announces the retirement of CFO Mike Zechmeister but will remain until successor named no later than May 31, 2024.

- Buyback Announcements or News:

- Primis Financial (FRST) approves stock buyback of 740,600 shares.

- Beyond (BYND) authorizes and extends two years and by $50 million, bringing total to $150 million.

- Stock Splits or News: None of note.

- After The Close Movers:

- Ups: RKLB +17.40%, ALDX +3.3%, CPLP +2.50%.

- Downs: NKE -9.4%, FL -4.7%, UAA -4%, DKS -2.60%, SKX -2.2%, LULU -1.9%

- Dividends Announcements or News:

- Insider Sales Of Note: None of note.

What’s Happening This Morning: Futures value reflects the change with fair value.

S&P 500 +2, Dow Jones -75, NASDAQ -1, and Russell 2000 +3. (as of 8:15 a.m. EST). Asia is lower ex Japan and Europe is lower ex the FTSE this morning. VIX Futures are at 15.50 from 15.75 this morning. Gold and Silver are higher with Copper lower this morning. WTI Crude Oil and Brent Crude Oil are higher with Natural Gas higher as well. US 10-year Treasury sees yields at 3.85% from 3.885% from yesterday. The U.S. Dollar is lower versus the Euro, lower versus the Pound and lower against the Yen. Bitcoin is at $43,571 from $44,048 higher by 1.01% this morning.

Sector Action – (1/3/6/12/YTD Updated Daily this week):

- Daily Positive Sectors: All sectors were higher yesterday.

- Daily Negative Sectors: None of note.

- One Month Winners: Real Estate, Materials, Industrials, Consumer Cyclicals, Financials of note.

- Three Month Winners: Technology, Real Estate, Industrials, Consumer Cyclicals and Materials of note.

- Six Month Winners: Financial, Communication Services, Technology, Energy and Consumer Cyclical of note.

- Twelve Month Winners: Technology, Communication Services, and Industrials of note.

- Year to Date Winners: Technology, Communication Services, Industrials and Financials of note.

Stocks rose Thursday, putting the S&P 500 back on track for its eighth consecutive week of gains. The benchmark index rose 1%. The tech-heavy Nasdaq Composite advanced 1.3%. The blue-chip Dow Jones Industrial Average gained 0.9%, or about 322 points. All three indexes are up so far this week. All 11 sectors within the S&P 500 ended Thursday higher. Consumer-discretionary stocks were the top performer, rising 1.4%. Utilities were the day’s laggard, gaining 0.1%. (WSJ – edited by QPI)

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Friday After the Close: none of note

- Tuesday Before the Open: None of note.

Earnings of Note This Morning:

- Beats: None of note.

- Flat: None of note.

- Misses: None of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Mixed Guidance: None of note.

- Negative Guidance: None of note.

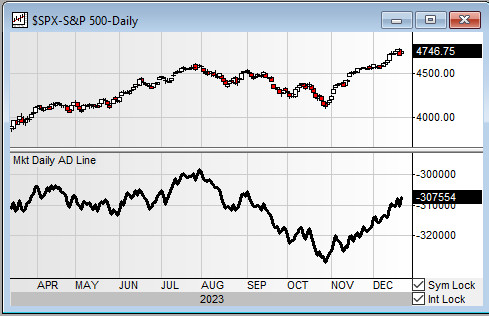

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market:

- Gap Up: KRTX +47%, GROM +18%, RKLB +16%, GLTO +16% of note.

- Gap Down: NCPL -40%, NTES -22%, NKE -12% of note.

Insider Action: Several stocks sees Insider buying with dumb short selling (rating of 4 or 5). No stocks see Insider buying with smart short sellers (rating of 1 to 3).

Rags & Mags.: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Stocks making the biggest moves before the bell: NKE BMY NTES COIN RKLB ADI (CNBC)

- What You Need To Know To Start Your Day. (Bloomberg)

- 5 Things To Know Before the Stock Market Opens on Thursday. (CNBC)

- Bloomberg Lead Story: Fed Rate Cuts Put Economists Against Market on Timing and Depth. (Bloomberg)

- Bloomberg Second Most Shared Story: Giuliani files for bankruptcy. (Bloomberg)

- Wall Street on edge before key economic data: Market Wrap. (Bloomberg)

- Top Chinese and U.S. military leaders hold first meeting in over a year. (CNBC)

- Bloomberg: Musk’s AI Chatbot “Grok” is weirdly good after all. (Podcast)

- NPR Marketplace: A week of legal troubles for Big Tech. (Podcast)

- NY Times Daily: Biden supports Israel. Does the rest of America? (Podcast)

- BBC Global Podcast: Gaza facing famine warns UN. (Podcast)

- Wealthion: AI impact on retail and potential retail revolution. (Podcast)

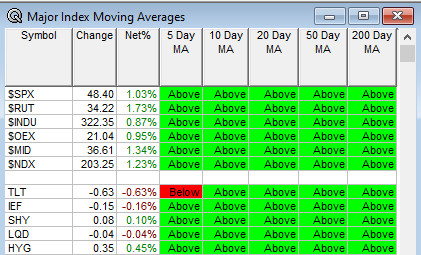

Moving Average Update:

- 100% from 80%. Day 7 ended the hype. We have added Bonds to show that TLT did break its weekly moving average.

Geopolitical:

- President’s Public Schedule:

- President Biden receives the Daily Briefing at 10:00 a.m. EST.

- President Biden and The First Lady visit the National Children’s Hospital at 3:45 p.m. EST.

Economic:

- November Personal Income is due out at 8:30 a.m. EST and is expected to rise to 0.40% from 0.20%

- November PCE Core is also due out at 8:30 a.m. EST and is expected to stay at 0.20%.

- November Durable Orders are also due out at 8:30 a.m. EST and are expected to rise to 2.5% from -5.4%.

- November New Home Sales are due out at 10:00 a.m. EST and are expected to rise to 689,000 from 679,000.

- The December University of Michigan Consumer Sentiment (Final) is due out at 10:00 a.m. EST and is expected to rise to 69.7 from 69.40.

Federal Reserve / Treasury Speakers: None of note.

M&A Activity and News:

- Bristol Myers (BMY) to buy Karuna Therapeutics (KRTX) for $14 billion. (CNBC)

Meeting & Conferences of Note:

- Sellside Conferences: None of note.

-

- Previously posted and ongoing conferences: None of note.

- Top Shareholder Meetings: None of note.

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: None of note.

- Update: None of note.

- R&D Day: None of note.

- PDUFA Dates today for IONS and GKOS.

- Company Event: None of note.

- Industry Meetings: None of note.

- Previously posted and ongoing conferences: None of note.

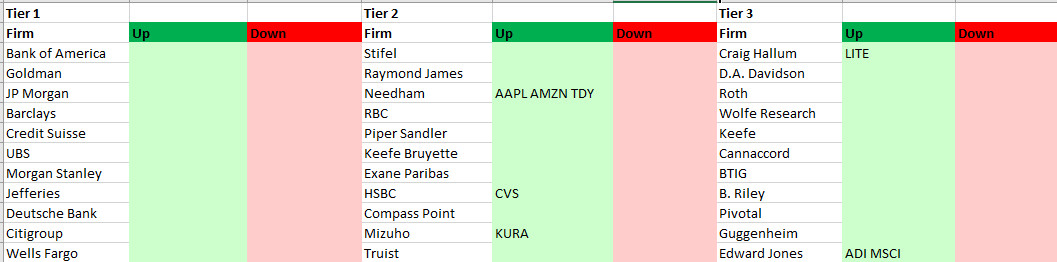

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades:

Previous Day’s Upgrades and Downgrades: