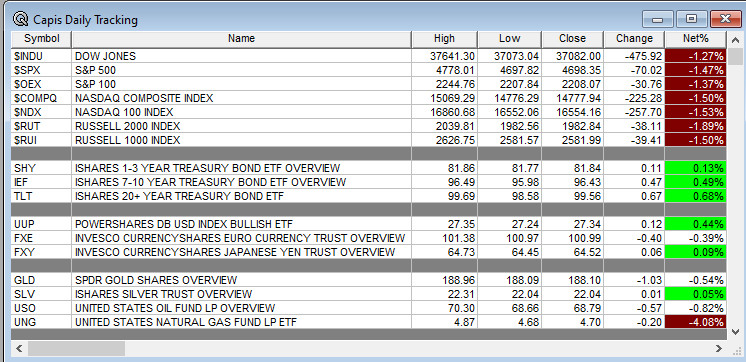

Overnight Summary: The S&P 500 closed Wednesday lower by -1.47% at 4698.35 from Tuesday higher by 0.59% at 4768.37. The overnight high was hit at 4778 at 4:30 a.m. EST while the low was hit at 4743.25 at 4:05 a.m. EST. The range overnight was 17 points as of 7:05 a.m. EST. The 10-day average of the overnight range is at 16.80 from 14.20. The average for May-November average was 21.43 from 22.06. Currently, the S&P 500 is higher by +20.50 at 6:00a.m. EST.

Breaking News: Angola announces its exit from OPEC. reports the state owned Jornal de Angola. (

Bloomberg)

Executive Summary: Well the idea that we “… should move into slower trading as the holidays are here with 7 trading days left in the year” got blown out of the water on Wednesday. The S&P 500 lost 1.47% and it is now lower for the week and its biggest one-day drop since the October low. Follow through or lack thereof will be key for today.

- Q3 GDP (revised) is due out at 8:30 a.m. EST and are expected to stay at 5.20%.

- December Philadelphia Fed Index is also due out at 8:30 a.m. EST and expected to improve to -3.0 from -5.90.

- November Leading Indicators are due out at 10:00 a.m. EST and are expected to improve to -0.4% from -0.8%.

Earnings Out After The Close:

- Beats: MU +0.06. BB +0.05 and MLKN +0.05 of note.

- Flat: None of note.

- Misses: None of note.

- IPOs Priced or News: None of note.

- New SPACs launched/News:

- Secondaries Priced: ANNX priced $125 million offering of common stock.

- Notes Priced of note: None of note.

- Common Stock filings/Notes:

- INPX filed a S-1 common stock offering of 10,000,000.

- Direct Offering: None of note.

- Selling Shareholders of note: None of note.

- KRRO: Files for 1,714,570 shares of common stock by selling shareholders.

- Private Placement of Public Entity (PIPE): None of note.

- Mixed Shelf Offerings:

- TEL: Files mixed shelf securities offering.

- FEAM: Files a $50M mixed securities shelf offering.

- AAT: Files a mixed shelf securities offering.

- NSC: Files a mixed shelf securities offering.

- WHR: Files a mixed shelf securities offering.

- GENE: Files a mixed shelf securities offering.

- NREF: Files a mixed shelf securities offering.

- Debt/Credit Filing and Notes: None of note.

- Tender Offer: None of note. None of note.

- Convertible Offering & Notes Filed: None of note.

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close and Over the Weekend:

- News Items After the Close:

- Forward Air (FWRD) sells Final Mile business to Hub Group for $262 million in cash.

- Southwest Air (LUV) reaches deal with their Airline Pilots Association, to be voted on by pilots.

- Erlanger Type 1 Short Squeezes and Type 4 Long Squeezes reporting earnings this week:

- Exchange/Listing/Company Reorg and Personnel News:

- Dave & Busters (DAVE) announces retirement of CFO Michael Quartieri on April 30, 2024.

- ADT (ADT) CFO Ken Porpora to step down to become CEO of a privately held company at year end.

- Buyback Announcements or News:

- BrightSphere Investment Group (BSIG) approves $100 million stock buyback.

- Autozone (AZO) authorizes and additional $2 billion repurchase.

- Stock Splits or News: None of note.

- After The Close Movers:

- Ups: CALT +27%, IMVT +6.4%.

- Downs: IPHA -4%, FEAM -3%, BB -2%.

- Dividends Announcements or News:

- Insider Sales Of Note: None of note.

What’s Happening This Morning: Futures value reflects the change with fair value.

S&P 500 +24, Dow Jones +153, NASDAQ +119, and Russell 2000 +18. (as of 8:10 a.m. EST). Asia and Europe are lower this morning. VIX Futures are at 15.75 from 14.95 this morning. Gold, Silver and Copper lower this morning. WTI Crude Oil and Brent Crude Oil are lower with Natural Gas higher as well. US 10-year Treasury sees yields at 3.885% unchanged from yesterday. The U.S. Dollar is lower versus the Euro, lower versus the Pound and lower against the Yen. Bitcoin is at $44,048 from $42,870 higher by 1.01% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Tuesday release):

- Daily Positive Sectors: Communication Services of note.

- Daily Negative Sectors: All others led by Consumer Cyclicals, Utilities and Consumer Defensive of note.

- One Month Winners: Real Estate, Materials, Industrials, Consumer Cyclicals, Financials of note.

- Three Month Winners: Technology, Real Estate, Industrials, Consumer Cyclicals and Materials of note.

- Six Month Winners: Financial, Communication Services, Technology, and Consumer Cyclical of note.

- Twelve Month Winners: Technology, Communication Services, and Consumer Cyclical of note.

- Year to Date Winners: Technology, Communication Services, Consumer Cyclical, and Industrials of note.

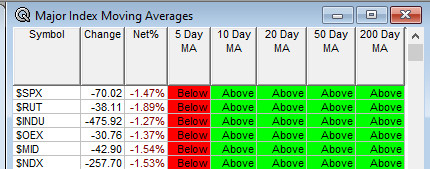

U.S. stocks pulled back Wednesday, pausing a rally that sent the Dow Jones Industrial Average to record highs. The S&P 500 fell 1.5% in its biggest one-day percentage drop since September. The Dow industrials shed about 476 points, or 1.3%, and the Nasdaq Composite eased 1.5%, marking their worst days since October. All three indexes were positive as of early Wednesday afternoon, then sold off to finish the session.

U.S. stock indexes had marched steadily higher since Federal Reserve Chair Jerome Powell at last week’s central bank policy meeting opened the door to interest-rate cuts. The Nasdaq and the Dow on Wednesday snapped nine-session winning streaks. The S&P 500 ended the day about 2% off its all-time high. Though the Fed’s latest projections suggested at least three rate cuts next year, investors’ expectations shifted toward even faster and deeper cuts. Traders are pricing in a roughly 73% chance of a rate cut at the Fed’s March policy meeting, up from around 28% a month ago, according to CME Group’s federal-funds futures.

Fed officials in recent public comments have tried to squelch speculation of a March cut. For the past year and half, markets have often reflected bets on a faster decline in inflation and more rate cuts than the Fed has signaled. “From our point of view, there is a danger that markets got a little bit overexcited,” said Christoph Schon, senior principal of applied research at Axioma.

Recent data suggest the economy is slowing enough for inflation to cool, but not enough to send the U.S. into a recession. The Fed’s preferred inflation gauge, the personal-consumption expenditures index, due Friday, will provide more clues for investors about the path ahead for inflation and rates. Though economic data show price pressures relaxing, some investors worry getting inflation all the way to the Fed’s target of 2% annual inflation could be challenging. “It’s like running a marathon. The last 2 miles are typically the hardest,” said Robert Conzo, CEO and managing director of The Wealth Alliance. Investors parsed fresh signals on the condition of the economy. A measure of consumer confidence jumped by nearly 10 points in December from November, according to the Conference Board. Existing home sales rose in November after five consecutive months of declines, topping economists’ forecasts.

The yield on the 10-year U.S. Treasury note—the benchmark for borrowing costs ranging from mortgages to corporate loans—dropped to 3.876% on Wednesday, the lowest level since July. Bond prices rise when yields fall. FedEx in its quarterly earnings report warned of weakening demand and lowered its forecast for annual revenue. Shares toppled 12%, their worst one-day drop since September 2022. General Mills dropped 3.6% after the packaged-foods maker reported a drop in sales for its recently ended quarter, citing softening demand for snacks and breakfast foods.

All 11 sectors in the S&P 500 fell on Wednesday. Communication services was the relative outperformer, down less than 0.1%, with Class A shares of Google parent Alphabet rising 1.2%. All 30 stocks in the Dow industrials closed lower. The small-cap Russell 2000 index also finished down 1.9%. The rally in oil markets continued, boosted by disruption to shipping through the Red Sea. Global benchmark Brent crude rose 0.6% to $79.70 a barrel.

(WSJ – edited by QPI)

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Thursday After the Close:

- Friday Before the Open: None of note.

Earnings of Note This Morning:

- Beats: APOG +0.13, KMX +0.10 of note.

- Flat: None of note.

- Misses: of note.

- Still to Report: CCL, CTAS and PAYX of note.

Company Earnings Guidance:

- Positive Guidance: MU of note.

- Mixed Guidance: MLKN, APOG of note.

- Negative Guidance: BB of note.

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market:

- Gap Up: MU +6%, KMX +4.4%, MLKN +3.3% of note.

- Gap Down: BB -2.0% of note.

Insider Action: Several stocks sees Insider buying with dumb short selling. see Insider buying with smart short sellers.

Rags & Mags.: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Stocks making the biggest moves before the bell: (CNBC)

- What You Need To Know To Start Your Day. (Bloomberg)

- 5 Things To Know Before the Stock Market Opens on Thursday. (CNBC)

- Bloomberg Lead Story: What Ruined The U.S. Stock Rally? Derivatives Trade. (Bloomberg)

- Bloomberg Second Most Shared Story: Vilified Zero Dated Options Blamed By Traders For the S&P 500 Decline. (Bloomberg)

- U.S. Equities Point To A Wall Street Rebound: Market Wrap. (Bloomberg)

- China revokes Taiwan tariff concessions, adding pressure before Taiwanese elections. (CNBC)

- U.N. Security Council to delay vote on resolution to stop fighting between Israel and Gaza. (NYT)

- President Biden considers increasing tariffs on some Chinese Goods including EVs made in China. (WSJ)

- Sudden Selloff confounds analysts. (CNBC)

- Every restaurant chain wants to beat Chick-fil-A, but they keep getting stronger. (CNBC)

- Holiday travel to be busier than last year. (Reuters)

- Bloomberg The Big Take: 5 Countries Acting as Economic Connectors in a fragmented world. (Podcast)

- NPR Marketplace: Demand for EV powering outpaces infrastructure. (Podcast)

- NY Times Daily: The rising toll of Israel’s War in Gaza. (Podcast)

- Wealthion: Hidden Dynamics behind banking. (Podcast)

Moving Average Update:

- 80% from 100%. Day 7 ended the hype. Drum beats on and on and it does not stop until the break of dawn which happened yesterday at 1:00 p.m. onward into the close.

Geopolitical:

- President’s Public Schedule:

- President Biden receives the Daily Briefing at 10:00 a.m. EST.

- Press Briefing at 1:00 p.m. by Press Secretary Karine Jean-Piere and NSC Coordinator for Strategic Communications John Kirby.

Economic:

- Q3 GDP (revised) is due out at 8:30 a.m. EST and are expected to stay at 5.20%.

- December Philadelphia Fed Index is also due out at 8:30 a.m. EST and expected to improve to -3.0 from -5.90.

- November Leading Indicators are due out at 10:00 a.m. EST and are expected to improve to -0.4% from -0.8%.

- Weekly Jobless Claims and Natural Gas Inventories due out at 8:30 a.m. EST and 10:00 a.m. EST.

Federal Reserve / Treasury Speakers: None of note.

M&A Activity and News:

- GMS to buy privately held Kamco Supply Corporation, no terms but Kamco did $245 million for fiscal 2023.

Meeting & Conferences of Note:

- Sellside Conferences: None of note.

-

- Previously posted and ongoing conferences: None of note.

- Top Shareholder Meetings: None of note.

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: None of note.

- Update: None of note.

- R&D Day: None of note.

- Company Event: None of note.

- Industry Meetings: None of note.

- Previously posted and ongoing conferences: None of note.

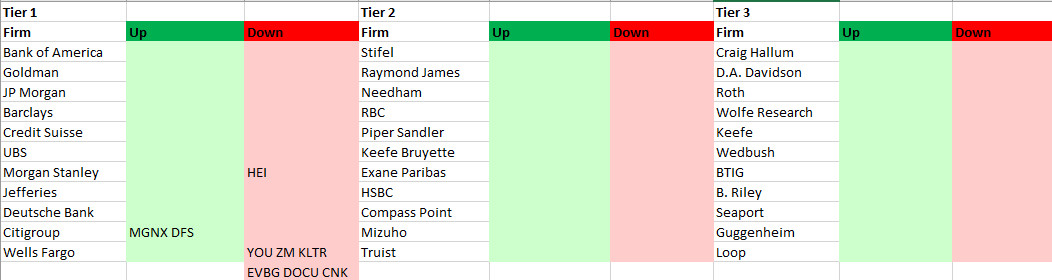

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades:

Previous Day’s Upgrades and Downgrades: