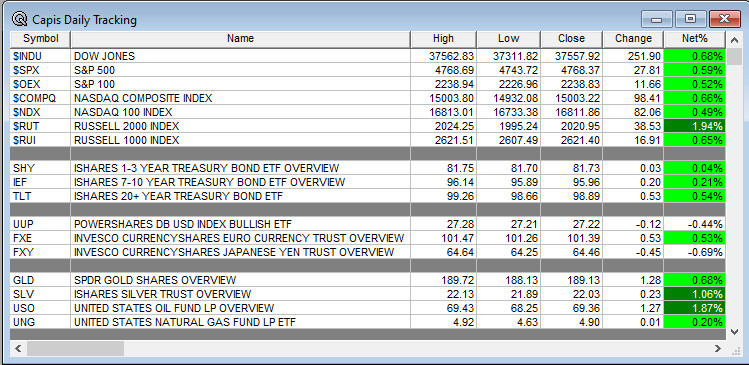

Overnight Summary: The S&P 500 closed Tuesday higher by 0.59% at 4768.37 from Monday higher by 0.57% at 4740.56. The overnight high was hit at 4824.25 at 12:30 a.m. EST while the low was hit at 4807.25 at 6:45 a.m. EST. The range overnight was 17 points as of 7:05 a.m. EST. The 10-day average of the overnight range is at 14.20 from 14.40. The average for May-November average was 21.43 from 22.06. Currently, the S&P 500 is lower by -9 at 7:15 a.m. EST.

Executive Summary: We should move into slower trading as the holidays are here with 7 trading days left in the year. Watch markets at 1 p.m. EST when the Treasury holds a 20 Year Auction as there has been some volatility around these auctions if buyers do not show up. Also, the weekly 10:30 Crude Oil numbers take on added significance today as Energy stocks are trying to rally off recent lows, a high inventory number would not be good for the short rally.

- December Consumer Confidence is due out at 10:00 a.m. EST and expected to rise to 104 from 102.

- November Existing Home Sales are also due out at 10:00 a.m. EST and are expected to improve to 3.80 million from 3.79 million.

Earnings Out After The Close:

- Beats: WOR+0.34, SCS +0.07 of note.

- Flat: None of note.

- Misses: FDX -0.20 of note.

- IPOs Priced or News: None of note.

- New SPACs launched/News:

- Secondaries Priced: BLUE priced 83,333,333 shares at $1.50.

- Notes Priced of note: None of note.

- Common Stock filings/Notes:

- GANX filed at S-1 for common stock and common stock with outstanding warrants.

- KULR filed a common stock public offering.

- NWHK filed a S-3 $200 mixed shelf offering.

- PHIO filed a S-1 common stock offering.

- Direct Offering: None of note.

- Selling Shareholders of note: None of note.

- : Files for 5,629,921 shares of common stock by selling shareholders.

- : Files for 5,859,375 shares of common stock by selling shareholder.

- Private Placement of Public Entity (PIPE): None of note.

- Mixed Shelf Offerings:

- CBRE: Files mixed shelf securities offering.

- INBK: Files a $200M mixed securities shelf offering.

- NWHK: Files a $200M mixed shelf securities offering.

- Debt/Credit Filing and Notes: None of note.

- Tender Offer: None of note. None of note.

- Convertible Offering & Notes Filed: None of note.

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close and Over the Weekend:

- News Items After the Close:

- Nasdaq 100 Closes At Another New Record .

- FedEx(FDX) lowers outlook to negative from flat in 2024.

- Guardant Health (GH) will have FDA Advisory Panel review their Shield Blood Test for colorectal cancer on 3/28/24.

- General Motors (GM) to halve the size of its Buick dealership in the U.S. through a buyout program. (CNBC)

- Enersys (ENS) raises Q3 guidance to $2.50 to $2.60 from $1.80 to $1.90.

- Goldman Sachs (GS) considering changes to the Management Committee. (Business Insider)

- Livent (LTHM) to replace NCR Voyix (VYX) in the S&P 400 and VYX to move to the S&P 600 replacing LTHM.

- Rush Enterprises (RUSHA) to replace RPT Realty (RPT) in the S&P 600 as being bought by Kimco Realty (KIM).

- Erlanger Type 1 Short Squeezes and Type 4 Long Squeezes reporting earnings this week:

- Exchange/Listing/Company Reorg and Personnel News:

- Methode Electronics (MEI) names Avi Avula as President and CEO of 1/29/24 following retirement of Donald Duda.

- Leslie’s (LESL) Chairman Steven Ortega to retire from the Board of Directors in March of 2024.

- Clear Channel (CCO) names David Sailer as EVP and CFO replacing Brian Coleman.

- Mitek Systems (MITK) names David Lyle as CFO.

- RTX CTO Mark Russell to retire January 1, 2024.

- Buyback Announcements or News:

- Fulton Financial (FULT) approves $125 million stock buyback.

- Stock Splits or News: None of note.

- Dividends Announcements or News:

- Fulton Financial (FULT) ups dividend of $0.17 a share from $0.16.

- Farmers & Merchants (FMAO) up quarterly dividend by 4.8% to $0.22 a share.

- Insider Sales Of Note: None of note.

What’s Happening This Morning: Futures value reflects the change with fair value.

S&P 500 -11, Dow Jones -60, NASDAQ -48, and Russell 2000 -1. (as of 8:10 a.m. EST). Asia is higher while Europe is higher ex the Germany this morning. VIX Futures are at 14.95 from 14.68 this morning. Gold and Silver lower with Copper higher this morning. WTI Crude Oil and Brent Crude Oil are higher with Natural Gas higher as well. US 10-year Treasury sees yields at 3.885% from 3.91% from yesterday. The U.S. Dollar is higher versus the Euro, higher versus the Pound and lower against the Yen. Bitcoin is at $42,870 from $42,975 higher by 1.51% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Tuesday release):

- Daily Positive Sectors: All were higher with Materials, Energy and Consumer Cyclicals of note.

- Daily Negative Sectors: None of note.

- One Month Winners: Real Estate, Materials, Consumer Cyclicals, Industrials, Financials of note.

- Three Month Winners: Technology, Industrials, Consumer Cyclicals and Materials of note.

- Six Month Winners: Financial, Communication Services, Technology, and Consumer Cyclical of note.

- Twelve Month Winners: Technology, Communication Services, and Consumer Cyclical of note.

- Year to Date Winners: Technology, Communication Services, Consumer Cyclical, and Industrials of note.

Growing optimism about the U.S. economy continued propelling the stock and bond markets Tuesday, pushing the Dow Jones Industrial Average to its fifth record in as many days. All three major indexes started the session in the green and didn’t look back. Led by Walgreens Boots Alliance and Caterpillar, the Dow rose 0.7%, or 252 points. The tech-heavy Nasdaq Composite also edged 0.7% higher, while the S&P 500 rose 0.6%.

Investors fearful of missing out on late-year gains have piled into equities after the Federal Reserve last week suggested rate cuts will be on the table next year. It has helped broaden the rally beyond this year’s big winners in the tech sector. Tuesday’s gains spanned every sector of the S&P 500, with energy and communications services leading the way. Smaller companies also continued outpacing the rest of the market as the Russell 2000 rose 1.9%. The projections putting each of the major indexes on pace for an eighth-straight weekly gain have also provided fuel for public and private debt alike.

Bryce Doty, senior portfolio manager at Sit Investment Associates, said his outlook for corporate bonds is the brightest it has been since the recovery from the global financial crisis. “We find ourselves strangely optimistic,” said Doty, who likened his team’s usual disposition to the depressed Winnie the Pooh character Eeyore. “Any relief from rates is going to benefit all companies.” Doty in recent weeks has funneled more money into corporate debt, including that of banks and insurance firms, even veering toward lower-quality debt to take full advantage of the rally. He suspects that his team could unwind some of those trades in the coming months if the Fed doesn’t cut rates fast enough to maintain U.S. economic growth. “There is a significant risk that they take too long,” Doty said.

The benchmark 10-year Treasury yield Tuesday inched down, to 3.921%, its lowest settle value since July 26. Yields fall when prices rise. In the stock market, shares in capital-intensive renewable-energy companies extended their Fed-fueled tear. The solar and battery-system supplier Enphase Energy advanced 9.1% after announcing that it would cut 10% of its workforce, while SolarEdge Technologies climbed 9.4% and First Solar rose 4%. The chip-maker Nvidia fell 0.9%, weighing on tech stocks. At the same time, Facebook-owner Meta reclaimed a $900 billion valuation after its share price rose by 1.7%.

For oil traders, threats to one of the world’s crucial trade routes are propping up prices. Benchmark U.S. crude rose 1.3%, to $73.44 a barrel, amid fears that Yemen’s Houthi rebels could keep attacking ships passing through the Red Sea on their way to or from the Suez Canal. Even as the U.S. assembles an international task force to protect commercial traffic, the risk from the Iranian-backed Houthis boosted shares in many energy firms. Shares in international oil majors, U.S. fuel refiners, shale drillers and tanker operators all gained Tuesday.

Despite the rosier economic projections for next year, some investors see reason to believe that the stock market’s current rally could soon slow. Emily Leveille, a portfolio manager at Thornburg Investment Management, said much of the good news has already been baked into share prices of American companies. Instead, Leveille is looking for valuable companies in regions including Latin America and Europe, where businesses are bought and sold at discounts, even when they perform as well as domestic firms. “Your risk-reward is very skewed to the upside,” she said.

(WSJ – edited by QPI)

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Wednesday After the Close:

- Thursday Before the Open:

Earnings of Note This Morning:

- Beats: GIS +0.09 of note.

- Flat: None of note.

- Misses: WGO -0.12 of note.

- Still to Report: of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Mixed Guidance: None of note.

- Negative Guidance: None of note.

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market:

- Gap Up: ACON +80%, RUSHA +6% of note.

- Gap Down: ARGX -28%, BLUE -40%, GH -12.5%, SCS -10%, FDX -10%, of note.

Insider Action: Several stocks sees Insider buying with dumb short selling. RILY VRCA see Insider buying with smart short sellers.

Rags & Mags.: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Stocks making the biggest moves before the bell: FDX GIS CRM WGO ARGX MARA (CNBC)

- What You Need To Know To Start Your Day. (Bloomberg)

- 5 Things To Know Before the Stock Market Opens on Wednesday. (CNBC)

- Bloomberg Lead Story: Trump Barred From Colorado Ballot in Unprecedented Ruling. (Bloomberg)

- Bloomberg Second Most Shared Story: Citi suite raises #metoo claims at Wall Streets top levels. (Bloomberg)

- Global Bond Rally speeds up as rate cut bets build: Market Wrap. (Bloomberg)

- Chinese President Xi warns President Biden that China will reunify Taiwan with China but timing not decided. (NBC News)

- Tesla (TSLA) cuts car prices more in China than BYD. (CNBC)

- Mortgage Demand drops despite another drop on interest rates. (CNBC)

- Bloomberg The Big Take: Public transit in the U.S. is about to get much worse. (Podcast)

- NPR Marketplace: Lab grown diamonds. (Podcast)

- NY Times Daily: Why a Colorado Court just knocked Trump off the ballot. (Podcast)

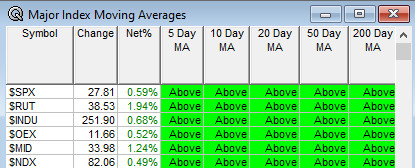

Moving Average Update:

- 100%. Day 6. Drum beats on and on and it does not stop until the break of dawn.

Geopolitical:

- President’s Public Schedule:

- President Biden receives the Daily Briefing at 9:00 a.m. EST.

- President Biden heads to Milwaukee, WI to deliver a speech at 1:45 p.m. EST to the Black Chamber of Commerce.

Economic:

- December Consumer Confidence is due out at 10:00 a.m. EST and expected to rise to 104 from 102.

- November Existing Home Sales are also due out at 10:00 a.m. EST and are expected to improve to 3.80 million from 3.79 million.

- EIA Petroleum Report at 10:30 a.m. EST.

- Treasury holds a 20 Year Treasury Bond Auction at 1:00 p.m. EST.

Federal Reserve / Treasury Speakers: Federal Reserve Chicago President Austan Goolsbee to speak but not a specific time.

M&A Activity and News:

Meeting & Conferences of Note:

- Sellside Conferences: None of note.

-

- Previously posted and ongoing conferences: None of note.

- Top Shareholder Meetings: None of note.

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: None of note.

- Update: None of note.

- R&D Day: None of note.

- Company Event: None of note.

- Industry Meetings: None of note.

- Previously posted and ongoing conferences: None of note.

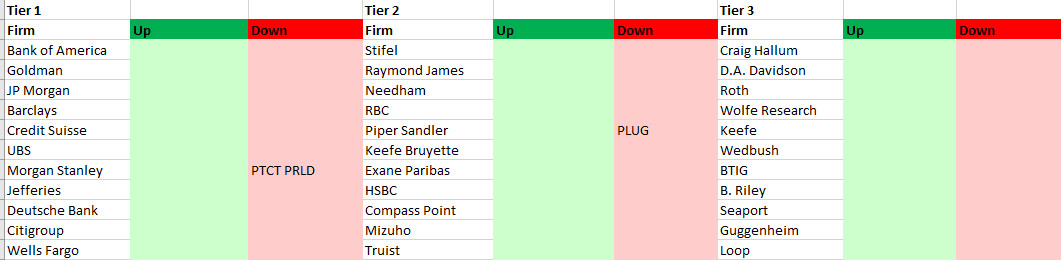

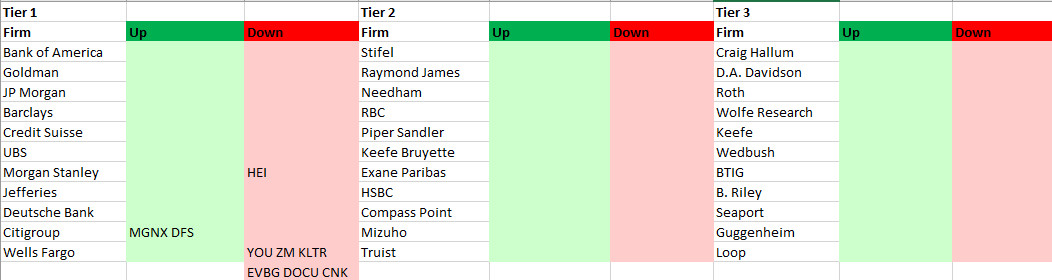

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades:

Previous Day’s Upgrades and Downgrades: