Overnight Summary: The S&P 500 closed Monday higher by 0.57% at 47 from Friday lower by -0.01% at 4719.19. The overnight high was hit at 4798.75 at 4:25 a.m. EST while the low was hit at 4787.50 at 8:40 p.m. EST. The range overnight was 11 points as of 7:05 a.m. EST. The 10-day average of the overnight range is at 14.40 from 15.40. The average for May-November average was 21.43 from 22.06. Currently, the S&P 500 is higher by +3 at 6:35 a.m. EST.

Executive Summary: We should move into slower trading as the holidays are here with 8 trading days left in the year.

- November Housing Starts are due out at 8:30 a.m. EST and are expected to rise to 1,385,000 from 1,360,000.

Earnings Out After The Close:

- Beats: HEI +0.06 of note.

- Flat: None of note.

- Misses: None of note.

- IPOs Priced or News: None of note.

- New SPACs launched/News:

- Secondaries Priced: None of note.

- Notes Priced of note: None of note.

- Common Stock filings/Notes:

- Bluebirdbio (BLUE) begins a $150 million stock offering

- MIRA filed a S-1 for 1,700,000 Shares of Common Stock.

- Direct Offering: None of note.

- Selling Shareholders of note: None of note.

- MAMA: Files for 5,629,921 shares of common stock by selling shareholders.

- TLSI: Files for 5,859,375 shares of common stock by selling shareholder.

- Private Placement of Public Entity (PIPE): None of note.

- Mixed Shelf Offerings:

- SEEL: Files $250M mixed shelf securities offering.

- : Files mixed securities shelf offering.

- : Files mixed shelf securities offering.

- Debt/Credit Filing and Notes: None of note.

- Tender Offer: None of note. None of note.

- Convertible Offering & Notes Filed: None of note.

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close and Over the Weekend:

- News Items After the Close:

- Nasdaq 100 Closes At A New Record .

- O’Reilly Automotive (ORLY) to buy Groupe Del Vasto and enters Canadian market, no terms.

- Comcast’s (CMCSA) Xfinity had a recent data breach of user names, passwords and personal information.

- Enphase Energy (ENPH) to cut global workforce by 10% and streamline operations.

- Tencent (TCEHY) shuts one of its U.S. video game studios. (Reuters)

- Erlanger Type 1 Short Squeezes and Type 4 Long Squeezes reporting earnings this week:

- Exchange/Listing/Company Reorg and Personnel News:

- Primerica (PRI) names Tracy Tan CFO as of 12/20/23.

- Seacoast Banking (SBCF) names Julie Kleffel as COO.

- Buyback Announcements or News:

- Churchill Downs (CHDN) to repurchase one million shares for $123.75 a share.

- Stock Splits or News: None of note.

- Dividends Announcements or News:

- Rayonier (RYN) declares a special cash dividend of $0.20 a share.

- Insider Sales Of Note: None of note.

What’s Happening This Morning: Futures value reflects the change with fair value.

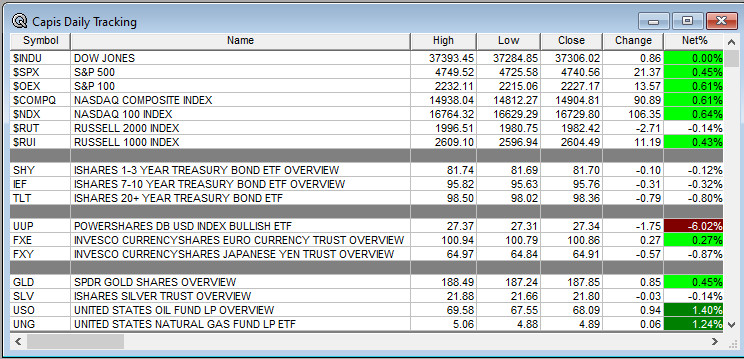

S&P 500 +11, Dow Jones +86, NASDAQ +30, and Russell 2000 +19. (as of 7:56 a.m. EST). Asia is higher ex the HSI while Europe is lower ex the Germany this morning. VIX Futures are at 14.68 from 14.60 this morning. Gold, Silver and Copper are higher this morning. WTI Crude Oil and Brent Crude Oil are lower with Natural Gas lower as well. US 10-year Treasury sees yields at 3.91% from 3.90% from yesterday. The U.S. Dollar is lower versus the Euro, lower versus the Pound and higher against the Yen. Bitcoin is at $42,975 from $40,938 higher by 2.72% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

- Daily Positive Sectors: Communication Services, Consumer Defensive and Energy of note.

- Daily Negative Sectors: Utilities and Real Estate of note.

- One Month Winners: Real Estate, Consumer Cyclical, Industrials, Financials of note.

- Three Month Winners: Technology, Industrials, and Real Estate of note.

- Six Month Winners: Financial, Technology, and Consumer Cyclical of note.

- Twelve Month Winners: Technology, Communication Services, and Consumer Cyclical of note.

- Year to Date Winners: Technology, Communication Services, Consumer Cyclical, and Industrials of note.

Investors dreaming of interest-rate cuts continued to push stocks higher on Monday. Coming off its seventh straight week of gains, the S&P 500 rose 0.5%. The tech-heavy Nasdaq Composite advanced 0.6%, while the Dow Jones Industrial Average was effectively unchanged, rising roughly one point to just eke out its fourth straight record close. The S&P 500’s weekly winning streak is its longest since 2017, underscoring the depth of Wall Street’s optimism right now. Stocks began rallying in late October, in large part due to growing hopes that the Federal Reserve will be able to pull off a “soft landing,” returning inflation to its 2% target while avoiding a recession.

After a series of encouraging inflation reports, investors dialed up bets that the Fed will start cutting rates next year. Last week’s Fed meeting reinforced those bets, with officials forecasting more cuts next year than many investors had expected them to do. A question now is what could stop the market rally. On Friday, the government will release major data on inflation, household income and spending. This week has the potential to be relatively quiet until then. “The market is kind of coasting on momentum,” said Michael Antonelli, market strategist at Baird. “When you get these year-end rallies after a year where people did a lot of hand-wringing, it’s mostly positioning…It’s people saying, ‘I can’t afford to be on the sidelines,’” he said.

In the days since the Fed meeting, a few officials have sent mixed messages about how seriously they are considering rate cuts. But investors have largely shrugged off those comments, judging that they didn’t add up to much new information. Shares of large technology companies were once again at the forefront of the market rally on Monday. Meanwhile, U.S. Steel jumped 26% after the company agreed to a $14.1 billion sale to Japan’s Nippon Steel . Shares of rival Cleveland-Cliffs rose 9.6%.

(WSJ – edited by QPI)

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Wednesday Before the Open:

Earnings of Note This Morning:

- Beats: ACN +0.13 FDS +0.01 FCEL +0.01 of note.

- Flat: None of note.

- Misses: None of note.

- Still to Report: of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Mixed Guidance: ACN of note.

- Negative Guidance: FDS of note.

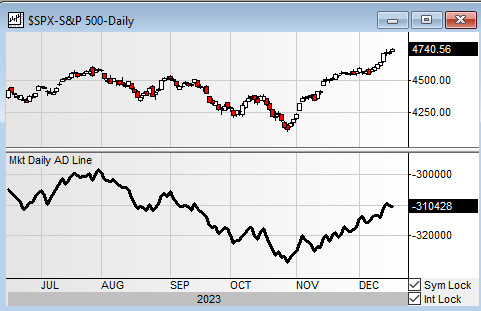

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market:

- Gap Up: ALDX +17% PTGC +6% KVUE +5% TSE +4% of note.

- Gap Down: QIPT -5% FCEL -4.6% FDS -2.7% ACN -2% of note.

Insider Action: Several stocks sees Insider buying with dumb short selling. TSE CHWY see Insider buying with smart short sellers.

Rags & Mags.: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Stocks making the biggest moves before the bell: (CNBC)

- What You Need To Know To Start Your Day. (Bloomberg)

- 5 Things To Know Before the Stock Market Opens on Tuesday. (CNBC)

- Bloomberg Lead Story: Apple Races to Tweak Software Ahead of Looming U.S. Watch Ban. (Bloomberg)

- Bloomberg Most Shared Story: Apple to halt sale of U.S. smartwatches after patent loss. (Bloomberg)

- BOJ’s hold hits Yen, offers fresh impetus to Bonds: Market Wrap. (Bloomberg)

- The Bank of Japan maintained its loose policy.

- Houthi attacks in the Red Sea threaten global supply chain. (CNBC)

- Iceland rocked by volcanic eruption. (Bloomberg)

- What if Putin wins? U.S. Allies fear defeat as Ukraine aid stalls. (Bloomberg)

- Cevian takes a $1.3 billion stake in UBS. (Bloomberg)

- Holiday spending to be up big, even as approval of Biden hits a new low. (CNBC)

- Bloomberg The Big Take: Equality trends of 2023 and what comes next. (Podcast)

- NPR Marketplace: EU tech regulatory framework protects consumers but slows down innovation. (Podcast)

- NY Times Daily: Football’s young victims. (Podcast)

- Wealthion: Rick Rule on Gold, Oil and Uranium. (Podcast)

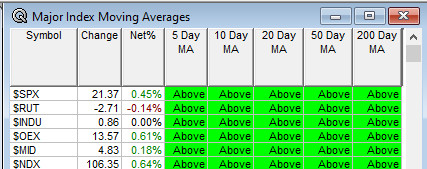

Moving Average Update:

- 100%. Day 6. Drum beats on and on and it does not stop until the break of dawn.

Geopolitical:

- President’s Public Schedule:

- President Biden receives the Daily Briefing at 8:30 a.m. EST.

- President Biden delivers remarks at a memorial service for Justice Sandra Day O’Connor.

- The White House holds a Press Briefing at 1:30 p.m. EST with Press Secretary Karine Jean-Pierre and NSC Coordinator John Kirby.

- President Biden attends a campaign reception in Bethesda, MD at 5:00 p.m. EST.

Economic:

- November Housing Starts are due out at 8:30 a.m. EST and are expected to rise to 1,385,000 from 1,360,000.

- API Crude Oil Weekly Data at 4:30 p.m. EST.

Federal Reserve / Treasury Speakers: Federal Reserve Atlanta President Raphael Bostic to speak at 12:30 p.m. EST and Federal Reserve Chicago President Austan Goolsbee at 6:00 p.m. EST.

M&A Activity and News:

- Salesforce (CRM) to acquire Spiff.

Meeting & Conferences of Note:

- Sellside Conferences: None of note.

-

- Previously posted and ongoing conferences: None of note.

- Top Shareholder Meetings: None of note.

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: holds a business update call.

- Update: None of note.

- R&D Day: None of note.

- Company Event: None of note.

- Industry Meetings: None of note.

- Previously posted and ongoing conferences: None of note.

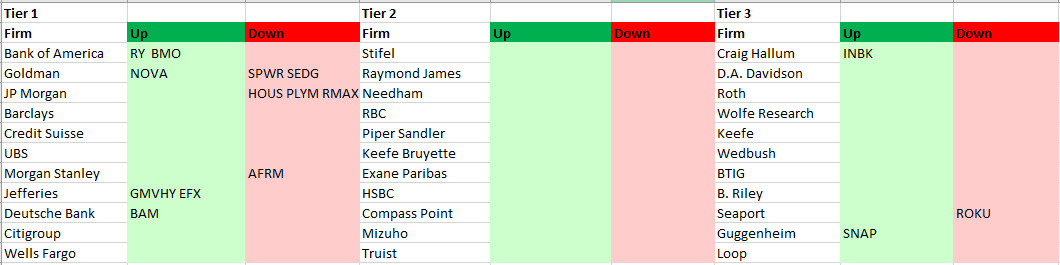

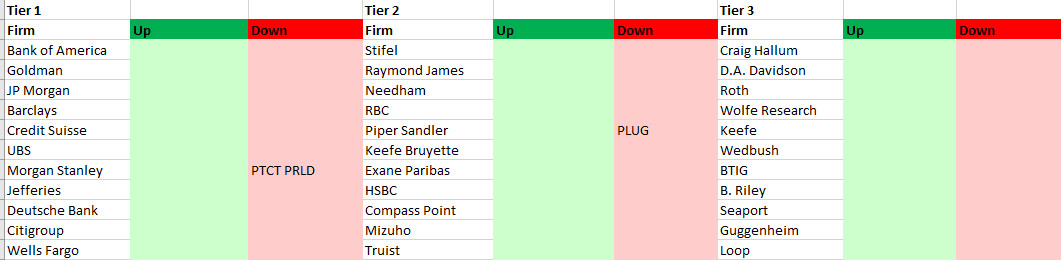

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades:

Previous Day’s Upgrades and Downgrades: