Overnight Summary: The S&P 500 closed Thursday lower by -1.35% at 4376.31 from Wednesday higher by 1.10% at 4436.01. Overnight ranges saw the high hit at 4399 at 6:40 a.m. EDT while the low was hit at 4378.50 at 4:35 p.m. EDT. The range overnight was 21 points. The 10-day average of the overnight range is at 28.70 from 28.60 yesterday. The average for May/June/July average was 18.81 from 19.94 in May/June. Currently, the S&P 500 is higher by +10 points and by +0.23% at 7:25 a.m. EDT.

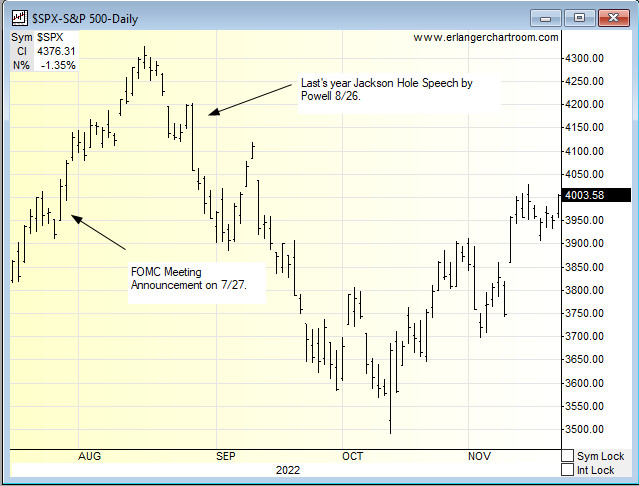

Last Year’s Jackson Hole Speech: The chart below shows the action after Powell’s speech. Here is the Morning Note from that day after (7/28) where you can read the about the speech.

Earnings Out After The Close:

- Beats: JWN +0.36, GPS +0.25, INTU +0.22, AFRM +0.18, ULTA +0.17, WDAY +0.17, DOMO +0.07, MRVL +0.01 of note.

- Flat: CRDO of note.

- Misses: None of note.

Capital Raises:

- IPOs Priced or News: None of note.

- New SPACs launched/News: None of note.

- Secondaries Priced:

- MYO: Pricing of $4.4 Million Public Offering — 7,333,334 shares of common stock (or common stock equivalents in lieu thereof) at a public offering price of $0.60 per share.

- Notes Priced of note: None of note.

- Common Stock filings/Notes:

- ECOR: Filed Form S-1.. 1,092,905 shares of Common Stock.

- MYO: Proposed Public Offering. (AGP Bookmanager)

- TBLT: Filed Form S-3.. 21,239,822 Shares of Common Stock.

- Direct Offering:

- EYEN: $12 Million Registered Direct Offering.. 4,198,633 shares. (Blair Bookmanager)

- Selling Shareholders of note:

- GRCL: Filed Form F-3.. 183,702,870 Ordinary Shares Represented by up to 36,740,574 American Depositary Shares by selling shareholders.

- PHVS: Filed Form 424B5..6,951,340 Ordinary Shares Offered by Selling Securityholders.

- Private Placement of Public Entity (PIPE):

- CYAD: Receives approximately EUR 9.8 million in private placement commitments from historical shareholders.

- Mixed Shelf Offerings:

- FLGC: Filed Form S-3.. $10,000,000 Mixed Shelf.

- MHUA: Filed Form F-3.. $100,000,000 Mixed Shelf.

- TTD: Filed Form S-3ASR.. Mixed Shelf.

- VMD: Files $150 million mixed shelf securities offering.

- Debt/Credit Filing and Notes:

- AMRC: Secures $300 Million Development and Construction Loan and Extends Maturity of Senior Secured Credit Facility Term Loan.

- CWK: Announces Closing of $400 Million Senior Secured Notes Offering and $1,000 Million Term Loan Facility.

- EPRT: Essential Properties Realty Trust, Inc. Announces New $450 Million 5.5 Year Unsecured Term Loan.

- LMT: Entered Into An Extension Agreement To Its $3.0 Billion Revolving Credit Agreement.

- Tender Offer: None of note.

- Convertible Offering & Notes Filed: None of note.

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close and Over the Holiday:

- After Hours:

- Trading Up: AFRM +6% of note.

- Trading Down: DOMO -22%, PAGS -6%, HE -4%, MRVL -4% of note.

- News Items After the Close:

- Stocks making the biggest moves after hours: AFRM, JWN, GPS, MRVL, ULTA, INTU, WDAY (CNBC)

- Hertz (HTZ) charges up to expand electric car fleet in NYC with Revel deal. (NYPost)

- Ulta (ULTA) says people are keeping their beauty routines post-pandemic, retailer raises outlook for the year. (MarketWatch)

- Domo’s (DOMO) stock drops more than 25% as outlook sours better-than-expected results. (MarketWatch)

- Workday’s (WDAY) stock is rising after another quarterly earnings beat. (MarketWatch)

- Biogen (BIIB) stock slips after FDA approves first biosimilar to Tysabri MS treatment. (MarketWatch)

- Nordstrom (JWN): “.. we have seen delinquencies rising gradually and they are now above pre-pandemic levels, which could result in higher credit losses in the second half and into 2024.”

- Amazon (AMZN) in Talks With Disney (DIS) About ESPN Streaming Partnership. (TheInformation)

- Lockheed Martin’s (LMT) Sikorsky Aircraft Corp awarded $2.77 billion U.S. Navy contract modification.

- Exchange/Listing/Company Reorg and Personnel News:

- AngloGold Ashanti (AU) appoints Richard Jordinson as COO

- Auddia Inc. (AUUD) Announces Filing of Delayed 10-Q Quarterly Report.

- DigitalOcean (DOCN) Announces Leadership Transition. CEO Yancey Spruill to step down; search underway for new CEO; Warren Adelman named exec chairman.

- Estee Lauder (EL) Chairman Emeritus Leonard A. Lauder not to stand for re-election to the Board.

- Kaman (KAMN) Announces Chief Financial Officer Transition.

- Kinetik (KNTK) promotes Trevor Howard to CFO, effective immediately.

- Owens Corning (OC) Announces Chief Financial Officer Transition. (MarketWatch)

- WSFS Financial (WSFS) announces that Arthur J. Bacci, Executive Vice President and Chief Wealth Officer, will also serve as interim CFO.

- Buyback Announcements or News: None of note.

- Stock Splits or News: None of note.

- Dividends Announcements or News:

- Hawaiian Electric (he) To Suspend Quarterly Cash Dividend. (MarketWatch)

- Insider Sales Of Note: None of note.

What’s Happening This Morning: Futures value reflects the change with fair value.

S&P 500 +8, Dow Jones +103, NASDAQ +10, and Russell 2000 +8. (as of 7:57 a.m. EDT). Asia lower while Europe is higher this morning. VIX Futures are at 17.85 from 16.88 yesterday. Gold lower with Silver and Copper higher this morning. WTI Crude Oil and Brent Crude Oil higher with Natural Gas lower. US 10-year Treasury sees yields at 4.251% from 4.217% yesterday. The U.S. Dollar is higher versus the Euro, lower versus the Pound and higher against the Yen. Bitcoin is at $26,091 from $26,503 yesterday, higher by 0.20%.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

- Daily Positive Sectors: None of note.

- Daily Negative Sectors: Technology, Communication Services, Industrials, Healthcare, Basic Materials, Energy, Consumer Defensive of note.

- One Month Winners: Energy, Communication Services of note.

- Three Month Winners: Energy, Consumer Cyclical, Industrials of note.

- Six Month Winners: Communication Services, Technology, Consumer Cyclical of note.

- Twelve Month Winners: Energy, Industrials, Technology of note.

- Year to Date Winners: Communication Services, Technology, Consumer Cyclical of note.

Nvidia’s (NVDA) record quarter wasn’t enough to lift the stock market on Thursday. The S&P 500 initially looked set to build on its best day since June, but finished 1.3% lower. Each of the benchmark’s 11 sectors closed in the red. Air came out of big tech stocks: Shares of Tesla (TSLA) and Amazon.com (AMZN), which comprise hefty portions of the market, dragged down the Nasdaq Composite to a 1.9% loss. Disney (DIS) shares extended this year’s rout, falling 3.9% to their lowest close in nearly nine years. Those losses weighed on the Dow industrials, which slid 1.1%.(WSJ – edited by QPI)

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Friday After the Close: None of note.

- Monday Before the Open: PDD, BZUN

Earnings of Note This Morning:

- Beats: HIBB +0.12 of note.

- Flat: None of note.

- Misses: None of note.

- Still to Report: None of note.

Guidance:

- Positive Guidance: OSIS, CRDO, AFRM of note.

- Negative Guidance: DOMO, GPS of note.

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market:

- Gap Up: AFRM +8%, CRDO +4% of note.

- Gap Down: DOMO -30%, HE -20%, PAGS -7%, DOCN -6% of note.

Insider Action: HTLD sees Insider buying with dumb short selling. No stock sees Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- 5 Things to Know Before the Stock Market Opens. (CNBC)

- Five Things You Need to Know to Start Your Day. (Bloomberg)

- Bloomberg Lead Story: China Stimulus Rally Lasts 10 Minutes. (Bloomberg)

- Bloomberg Most Shared Story: Zillow Offers 1% Down Payment to Lure Struggling Homebuyers. (Bloomberg)

- Stocks set for weekly gains as traders await Powell: Market Wrap. (Bloomberg)

- Jackson Hole Conference is underway. What to expect. (Bloomberg)

- Trump arrest, full recap. (CNBC)

- Alibaba (BABA) launches AI model that can understand images. (CNBC)

- CDC expects new Covid vaccines to be available by mid September. (CNBC)

- NPR Marketplace: Nearly every business had to pivot during the pandemic. But domestic manufacturing has been weak for a while now. On today’s show, we hear how businesses in the sector are looking to pivot yet again. Plus: the challenges faced by schools as pandemic funding ends, and the risks around chipmaker Nvidia’s dominance of a very concentrated market. Later: Wordle, but make it global trade. (Podcast)

- BBC Global News: Trump surrenders in Georgia. (Podcast)

- NY Times The Daily: Putin’s revenge. (Podcast)

- Bloomberg: Why is the U.S. dependent on Russian Uranium. (Podcast)

Moving Average Update:

- The score retreats down to 20% from 51%. Short term all got wiped out and we have a sizable gap down to the 200 day moving average.

Geopolitical:

- President’s Public Schedule:

- On Friday, the President has no public events scheduled.

Economic:

- August University of Michigan Consumer Sentiment (Final) is due out at 10:00 a.m. EDT and is expected to remain at 71.20.

- Inflation Expectations 10:00 a.m. EDT

- Baker Hughes Rig Count 1:00 p.m. EDT

Federal Reserve / Treasury Speakers:

- Jackson Hole Economic Policy Symposium

- Federal Reserve Chair Jerome Powell Jerome Powell 10:05 a.m. EDT

M&A Activity and News:

- HollySys (HOLI): Buyer consortium confirms its reiterated non-binding all-cash offer of $25 per share, or approximately $1.55 bln to acquire Hollysys.

- PHX Minerals (PHX) Announces Accretive Acquisitions in Haynesville and SCOOP.

- Burke & Herbert Financial Services Corp. and Summit Financial Group, Inc. (SMMF) Announce Merger of Equals.

Meeting & Conferences of Note:

- Sellside Conferences: None of note.

-

- Previously posted and ongoing conferences:

- Truist Atlanta Bank Summit

- Wolfe Research Consumer Conference

- Previously posted and ongoing conferences:

-

- Top Shareholder Meetings: MOXC, ZYNE.

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: TARS

- Update: None of note.

- R&D Day: None of note.

- Company Event: None of note.

- Industry Meetings:

- European Society of Cardiology (ESC) Congress 2023 (08/25/23-08/28/23)

- 7th Annual Gulfcoast Orthopaedic Rehabilitation Conference 2023 (08/26/23)

- International Congress of Parkinsons Disease and Movement Disorders 2023 (08/27/23-08/31/23)

- Previously posted and ongoing conferences:

- 6th Annual Conference of the American Association for Bronchology and Interventional Pulmonology (AABIP) 2023 (08/24/23-08/26/23)

- International Meeting on Information Display

- Previously posted and ongoing conferences:

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades:

Previous Day’s Upgrades and Downgrades: