Overnight Summary: The SP 500 closed Wednesday higher by 0.02% at 5071.63 from Tuesday higher by 1.20% at 5070.55. The overnight high was hit at 5,109 at 4:05 p.m. while the overnight low was hit at 5066.50 at 2:35 a.m. EDT. The range overnight is 42 points as of 6:15 a.m. EDT. Currently, the S&P 500 is lower by -28 points at 6:15 a.m. EDT.

Executive Summary: The big story is earning’s beats but poor guidance making stocks head lower. Case in point Meta. Be careful of stocks up into earnings.

- 7 Year Auction at 1 p.m. EDT.

- Q1 GDP (Advanced) is due out at 8:30 a.m. EDT and expected to fall to 2.4% from 3.4%.

- March Pending Home Sales are due out at 10:00 a.m. EDT and are expected to fall to 1.0% from 1.6%.

Earnings Out After The Close:

- Beats: CMG +1.68, MTH +1.51, CCS +0.83, URI +0.78, LRCX +0.49, KALU +0.46, META +0.39, CHDN +0.34, NOW +0.27, WM +0.24, ALGN +0.17, BMRN +0.14, CACI +0.11, PI +o.11, WHR +0.11, AR+0.09, IBM +0.09, OII +0.07, F +0.06, MOH +0.05, WCN +0.04, WU +0.04, WH +0.04, CLB +0.03, VKTX +0.02, RJF +.01 of note.

- Flat: None of note.

- Misses: NBR -2.93, PFSI -1.53, CHE -0.28, KNX -0.18, ETD -0.16, ORLY -0.09, GGG -0.09, FAF -0.06, HP -0.01 of note.

- IPOs Priced or News:

- Rubrick is priced at $32 a share, above range.

- New SPACs launched/News:

- Secondaries Priced:

- Notes Priced of note:

- Common Stock filings/Notes:

- AZZ filed proposed offering of common stock.

- DYAI filed offering of 3,351, 954 shares of common stock.

- ITCI closing of $575 million of common stock including full exercise of underwriter’s option to purchase additional shares.

- LHRC files 6,950,334 shares of common stock.

- SOAR files for shares of common stock.

- UPC files up to 20,000,000 share of ordinary shares.

- Direct Offering:

- Exchangeable Subordinate Voting Shares:

- Selling Shareholders of note:

- Private Placement of Public Entity (PIPE):

- Mixed Shelf Offerings:

- Debt/Credit Filing and Notes:

- Tender Offer:

- Rights Offering:

- VATE announces closing of rights offering.

- Convertible Offering & Notes Filed:

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close :

- After Hours Movers:

- PI +12%, TER +7%, CLS +6%, ALGN +5%, CMG +3%

- META -16%, IBM -9%, NOW -5%, ORLY -4%,

- News Items After the Close:

- Taiwan Semiconductor (TSM) announces alliance with Synopsys (SNPS) and Cadence Design (CDNS) to accelerate designs, after the close.

- Meta (META) ups cap-ex to $35 to $40 billion from $30 to $37 billion.

- META conference call update shifting focus to AI which will be a multi-year investment cycle. More than 50% of content on Instagram is AI driven.

- BHP considering a takeover of AngloAmerican Plc.

- Exchange/Listing/Company Reorg and Personnel News:

- CNMD names Patrick Beyer Chief Operating Officer.

- PLAY names Darin Harper as CFO , as of June 17th.

- ADT names Jeff Likosar as CFO in addition to serving as President of Corporate Development and Chief Transformation Officer.

- Buyback Announcements or News:

- BALL Board of Directors approves repurchase of 40 million shares of its common stock.

- Stock Splits or News:

- Dividends Announcements or News:

What’s Happening This Morning: Futures value reflects the change with fair value.

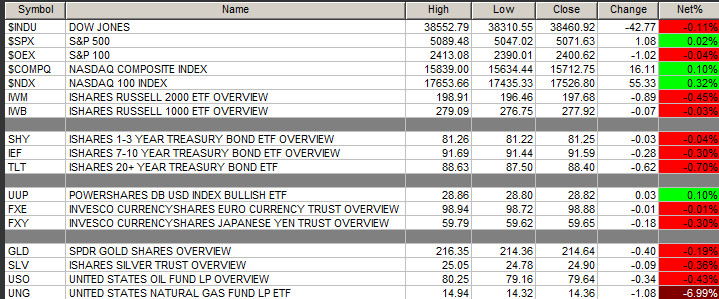

S&P 500 – , Dow Jones – , NASDAQ – , Russell +9.97. (as of 8:05 a.m. EST). Asia is lower and Europe is lower this morning ex the FTSE. VIX Futures are at 16.05 from 15.75. Gold is lower with Silver and Copper are higher this morning. WTI Crude Oil and Brent Crude Oil are lower with Natural Gas lower as well. US 10-year Treasury sees its yield at 4.64% unchanged from yesterday. The U.S. Dollar is lower versus the Euro, lower versus the Pound and higheragainst the Yen. Bitcoin is at $63,575 from $66,405 lower by -0.99% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

- Daily Positive Sectors: Consumer Defensive, Utilities, Consumer Cyclical and Real Estate of note.

- Daily Negative Sectors: Industrials, Healthcare and Financials of note.

- One Month Winners: Energy and Utilities of note.

- Three Month Winners: Energy, Basic Materials, Industrials, and Financial of note.

- Six Month Winners: Financials, Industrials, Technology and Communication Services of note.

- Twelve Month Winners: Communication Services, Technology, Industrials, and Financial of note.

- Year to Date Winners: Communication Services, Energy, Financials, Industrials, and Technology of note.

(WSJ – Edited by QPI)

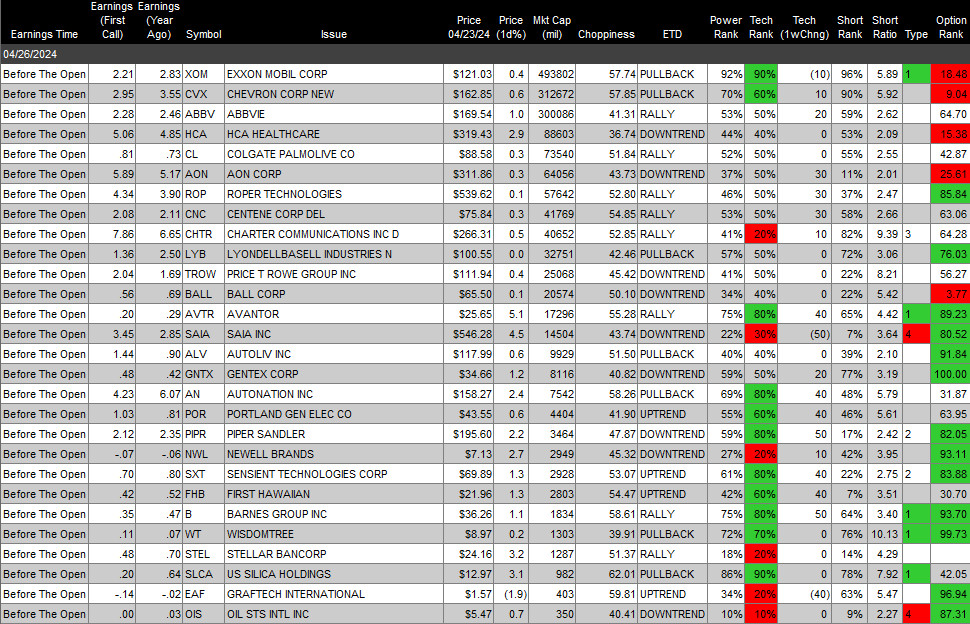

Upcoming Earnings Of Note:

- Thursday After the Close:

Earnings of Note This Morning: (Greater Than $0.10 and Lower Than $-0.00)

- Beats: SNY +1.59, HES +1.45, EME +1.33, AZN +1.10, CWT +1.06, OSK +0.64, VLO +0.60, NOC +0.54, CAT +0.46, RCL +0.44, FCN +0.36, HOG +0.21, NEM +0.19, UNP +0.18, CARR +0.12, LAZ +0.11, TSCO +0.11, TRU +0.11, XEL +0.11 of note.

- Flat: of note.

- Misses: HTZ -0.83, ABG -0.55, HZO -0.48, RS -0.23, SAGE -0.15, STM -0.08, AAL -0.07, VC -0.06, IP -0.05, TXT -0.02, LUV -o.o2, NDAQ -0.02, VLY -0.01, MBLY -0.01 of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: EME OSK RCL of note.

- Negative Guidance: RS HZO of note.

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: PI +15.8%, MTH +12.7%, ACRV +11.3%, TER +9.1%, IBRX +8.9%, CYH +7.3%, CLS +6.6%, AZN +6.1%, BCS +5.9%, UL +5.9%, ALGN +5.8%, SNY +5.3%, CASH +5%, HCP +4.8%, EPRT +4.4%, IRT +4.1%, ASX +4%, EQNR +3.8%, CHDN +3.7%, AR +3.5%, CCS +3.5%, OSK +3.1%, CWT +3.1%, SLM +2.9%, CLB +2.8%, F +2.7%, CMG +2.7%, HON +2.7%, OII +2.5%, STM +2.5%, ANET +2.4%, URI +2.3%, MEOH +2.2%, TYL +2.1%, UHS +2%of note.

- Gap Down: META -13.1%, ATNI -10.3%, IBM -8.9%, SNBR -6.8%, ETD -5.7%, MXL -5.3%, GGG -4.8%, SNAP -4.7%, PINS -4.5%, NOW -4.5%, RJF -4.5%, BMRN -4.3%, NBR -3.9%, PEGA -3.6%, BHP -3.3%, LH -3.3%, ORLY -3.2%, TTD -3%, AZZ -2.9%, CNMD -2.9%, HLX -2.7%, COCO -2.5%, BC -2.5%, HP -2.2%, IPAR -2.1%, ADT -2% of note.

Insider Action: No stock sees Insider buying with dumb short selling. No stock sees Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Bloomberg Lead Story: Meta Miss Sparks Fears in Tech With More Earnings Ahead. (Bloomberg)

- Secretary of State Blinken raises trade concerns with China. (Bloomberg)

- Tech stocks drag down U.S. before GDP data: Markets Wrap. (Bloomberg)

- Rubrick priced IPO at $32 above range. (CNBC)

- Bloomberg: Daybreak Podcast: (Podcast)

- Bloomberg: The Big Take: How to get a meeting with UAE’s $1.5 trillion dollar man. (Podcast)

- Marketplace: Inside Amazon’s Business Tactics and Company Culture. (Podcast)

- NY Times Daily: Crackdown on Student Protestors. (Podcast)

- Wealthion: No recession? Why the economy is stronger than you think. (Podcast)

- Adam Taggart’s Thoughtful Money: “Something is going to break”. (Podcast)

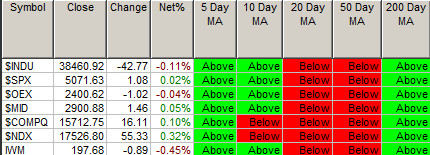

Moving Average Update: Score improves to 54.28% from 51%.

Geopolitical:

- President’s Public Schedule:

- President Biden receives the Daily Briefing at 10:00 a.m. EDT.

- President Biden then departs to Syracuse to speak about the CHIPS Act at 2:00 p.m. EDT.

- President Biden then heads to a campaign event in Westchester County at 6:15 p.m. EDT before heading to Wall Street at 7:50 p.m. EDT.

Economic:

- Q1 GDP (Advanced) is due out at 8:30 a.m. EDT and expected to fall to 2.4% from 3.4%.

- March Pending Home Sales are due out at 10:00 a.m. EDT and are expected to fall to 1.0% from 1.6%.

Federal Reserve / Treasury Speakers:

- No Fed Speakers as in Blackout Period due to next week’s FOMC meeting.

M&A Activity and News:

- IBM to buy HashiCorp (HCP) for $35 a share in cash.

- BHP makes a bid for Anglo-American. (CNBC)

Meeting & Conferences of Note:

- Sellside Conferences:

- Top Shareholder Meetings: AES, CLS, EIX, ERJ, FAST, GRC, HIFS, HLF, JNJ, MYE, NGMS, ODP, PAC, PBR, PFE, PFS, SBS, SNA, TFII, TXN.

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: ALDX, BPMC, HOOK

- Update: None of note.

- R&D Day: None of note.

- Company Event:

- Industry Meetings:

- Alzheimer’s & Parkinson’s Drug Development Summit

- Horizon User Conference

- Inaugural Connect+ Customer Conference

- Spinal Cord Injury Investor Symposium

- The Future of Protein Production

- TikTok Partnership Event

- World Orphan Drug Congress

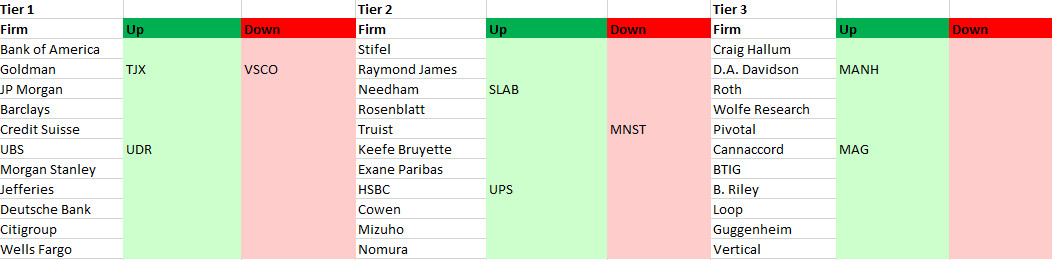

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades: