Overnight Summary: The SP 500 closed Tuesday higher by 0.14% at 5209.91 from Monday lower by -0.04% from 5202.39. The overnight high was hit at 5,272 at 4:05 p.m. while the overnight low was hit at 5262 at 2:05 a.m. EDT. The range overnight is 10 points as of 5:40 a.m. EDT. Currently, the S&P 500 is higher by +5 points at 5:45 a.m. EDT.

Executive Summary: All eyes are focused on the latest CPI number today. Estimates are for an increase of 0.3% from 0.4% last month. Note there is a 10-year Auction at 1:00 p.m. and yesterday’s 3-year did not do well so traders will be watching it as well.

- The latest NYSE And NASDAQ Short Interest is out and both increased. NYSE rose by 0.13% and NASDAQ by 1.24%. NASDAQ has seen increases in the first six updates of the year while NYSE has seen increased in five of the first six updates. Shorts continue to remain brazen.

Earnings Out After The Close:

- Beats: PSMT +0.07, WDFC +0.03, SGJ +0.02.

- Flat: None of note.

- Misses: None of note.

- IPOs Priced or News:None of note.

- New SPACs launched/News: None of note.

- Secondaries Priced: None of note.

- Notes Priced of note:

- FANG prices Senior Notes.

- Common Stock filings/Notes:

- XXII files 1,855,000 shares of common stock.

- ASUR files 12,500,000 shares of common stock.

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares:

- Selling Shareholders of note:

- RGLS files for 62,500,167 shares of common stock by selling shareholders.

- VYTX files for 11,174,000 shares of common stock by selling shareholders.

- FGI files 6,816,250 shares of common stock by selling shareholders.

- Private Placement of Public Entity (PIPE): None of note.

- Mixed Shelf Offerings:

- BLK file for a mixed-shelf offering.

- SONM files a $75 million mixed-shelf offering.

- ASUR files a $150 million mixed-shelf offering.

- FGI files a $25 million mixed-shelf offering.

- Debt/Credit Filing and Notes: None of note.

- HST $2 billion of debt shelf.

- Tender Offer: None of note.

- Convertible Offering & Notes Filed: None of note.

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close :

- After Hours Movers:

- INAB +29.4%, PSMT +4.1%

- RGLS -7.4%, SGH -5.9%, HEAR -5.5%, DCGO -4.2%, HXL -3%, WDFC -2.8%

- News Items After the Close:

- Alliance Bernstein (AB) sees assets grow from $746 billion in February to $759 billion at end of March.

- Invesco ((IVZ) sees assets grow 2% in March by $1.663 billion.

- Artisan Partners (APAM) assets at $160.4 billion at the end of Q1.

- Victory Capital (VCTR) grows assets in March by $3 billion to reach $170.3 billion.

- Centene (CNC) picks up the Michigan Medicaid Health Plan for Comprehensive Health Care Program serving 2 million in the state.

- Lockheed Martin (LMT) awarded $181 million Navy contract.

- Exchange/Listing/Company Reorg and Personnel News:

- Hexcel (HXL) names Tom Gentile CEO and President with Nick Stanage moving to Executive Chairman.

- Illumina (ILMN) names Ankur Dhingra as CFO, Joydeep Goswami to leave June 30th. Reiterates outlook.

- Honest Company (HNST) reaffirms FY24 Guidance but that Founder Jessica Alba will step down as Chief Creative Officer.

- Buyback Announcements or News: None of note.

- Stock Splits or News: None of note.

- Dividends Announcements or News:

- Proctor & Gamble (PG) ups quarterly dividend by 7% $ $1.0065 a share, yield of 2.6%.

What’s Happening This Morning: Futures value reflects the change with fair value.

S&P 500 +7, Dow Jones +65, NASDAQ +16, Russell +6.40. (as of 7:56 a.m. EST). Asia lower ex the ASX 200 and Europe is higher this morning. VIX Futures are at 15.01 from 15.40. Gold, Silver and Copper are higher this morning for a third consecutive day. WTI Crude Oil and Brent Crude Oil are higher with Natural Gas higher as well for a second day in a row. US 10-year Treasury sees its yield at 4.36% from 4.395%. The U.S. Dollar is lower versus the Euro, lower versus the Pound and higher against the Yen. Bitcoin is at $69,124 from $70,473 higher by +0.27% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

- Daily Positive Sectors: Real Estate, Materials, Consumer Cyclicals and Utilities of note.

- Daily Negative Sectors: Financials, Industrials and Energy of note.

- One Month Winners: Energy, Communication Services, Basic Materials and Industrials of note.

- Three Month Winners: Technology, Communication Services, Industrials, Energy and Financials of note.

- Six Month Winners: Technology, Financials, Industrials of note.

- Twelve Month Winners: Technology, Communication Services, and Financial of note.

- Year to Date Winners: Energy, Communication Services, Technology and Financials of note.

Upcoming Earnings Of Note:

- Wednesday After the Close: None of note.

- Thursday Before the Open: KMX, STZ, FAST and LOVE.

Earnings of Note This Morning:

- Beats: DAL +0.09.

- Flat: None of note.

- Misses:

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: DAL.

- Negative Guidance: .

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: INAB +22%, IMRN +9.6%, IPI +8%, PSMT +4.6%, LSCC +4.4%, XPEV +3.3%, QSI +3.2%, STTK +2.8%, PHG +2.4%, ADCT +2.3% of note.

- Gap Down: SGH -6.3%, DCGO -6%, RGLS -3.7%, HXL -3.6%, RICK -3.1%, HEAR -2.6%, WDFC -2.6%, Sof note.

Insider Action: No stock see Insider buying with dumb short selling. No stock see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- 5 Things To Know Before the Stock Market Opens Today. (CNBC)

- What You Need To Know To Start Your Day. (Bloomberg)

- Bloomberg Lead Story: March Inflation Data to Prolong Drama Around Fed Rate Cut Timing. (Bloomberg)

- European Stocks stage rebound in front of U.S. CPI data: Markets Wrap. (Bloomberg)

- Fitch downgrades China Outlook to Negative on steady rise in debt. (Bloomberg)

- Jack Ma sends employees of Alibaba (BABA) a rare email. (South China Morning Post)

- Large U.S. Investors are selling Treasuries and buying European bonds. (FT)

- $200 Billion of M&A in the Energy Patch was not enough. (Bloomberg)

- Mortgage refinance debt climbs even though rates move above 7%. (CNBC)

- Nvidia (NVDA) enters correction territory as stock corrects 10%. (CNBC)

- Bloomberg: Daybreak Podcast: TSMC Sales surge, U.S. CPI may moderate. (Podcast)

- Bloomberg: The Big Take: How U.S. Steel (X) takeover became about Biden and swing states. (Podcast)

- NYT The Daily: Trump’s about face on abortion. (Podcast)

- Marketplace: South Korea votes as economic issues weigh on population. (Podcast)

Moving Average Update: Score improves to 82% to 71%.

Geopolitical:

- President’s Public Schedule:

- President Biden receives the Daily Briefing at 9:00 a.m. EDT.

- The President and First Lady greet the Prime Minister of Japan and First Lady in official arrival ceremony at 10:00 a.m. EDT.

- President Biden holds a bilateral meeting with the Prime Minister of Japan at 11:00 a.m. EDT. Joint News Conference to follow at 12:30 p.m. EDT.

- President Biden and First Lady greet the Prime Minister of Japan and First Lady at the State Dinner that begins at 6:30 p.m. EDT and continues to 9:30 p.m. EDT.

Economic:

- March CPI is due out at 8:30 a.m. EDT and is expected to fall to 0.30% from 0.40%.

- Bank of Canada is out with its latest rate announcement.

- Treasury holds a 10-year auction at 1:00 p.m. EDT.

- The latest FOMC Minutes from the meeting on March 6th and 7th are due out at 2:00 p.m. EDT.

Federal Reserve / Treasury Speakers:

- Federal Reserve Governor Bowman speaks at 8:00 a.m. EDT.

- Federal Reserve Chicago President Austan Goolsbee speaks at 12:45 p.m. EDT.

M&A Activity and News: None of note.

Meeting & Conferences of Note:

- Sellside Conferences:

- BMO CAPP Energy Conference

- Deutsche Bank Private FinTech Conference

- Goldman Sachs Private Software and Internet Conference

- Jefferies Latin America Summit

- Needham Healthcare Conference

- Wells Fargo Software Symposium

- Top Shareholder Meetings: None of note.

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: AMLX CMMB COST FNV KKR

- Update: None of note.

- R&D Day: None of note.

- Company Event: None of note.

- Industry Meetings:

- Space Symposium

- Google Cloud Next

- Gold Forum Europe

- Spinal Cord Injury Investor Symposium

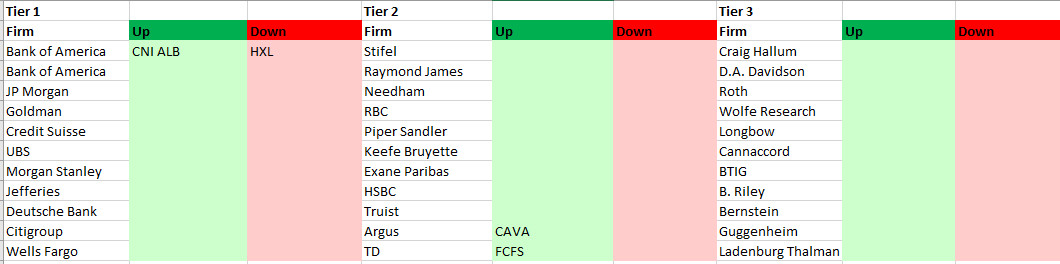

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades: