Overnight Summary: The SP 500 closed Monday lower by -0.04% from 5202.39 from Friday higher by 1.11% at 5204.34. The overnight high was hit at 5,259.25 at 5:58 a.m. while the overnight low was hit at 5248.50 at 4:05 a.m. EDT. The range overnight is 11 points as of 7:02 a.m. EDT. Currently, the S&P 500 is higher by +10 points at 8:05 a.m. EDT.

Executive Summary: Expect a sideways day as everyone is waiting to see what inflation looks like tomorrow/

- Treasury holds a 3-Year Note Auction at 1:00 p.m. EDT.

Earnings Out After The Close:

- Beats: None of note.

- Flat: None of note.

- Misses: None of note.

- IPOs Priced or News:None of note.

- New SPACs launched/News: None of note.

- Secondaries Priced:None of note.

- Notes Priced of note:

- Common Stock filings/Notes:

- AIMD offers 4,430,732 shares of common stock.

- BIOR offers 10,700,846 shares of common stock.

- HWH offers 149,443 shares of common stock.

- VERO offers 1,644,000 shares of common stock.

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares:

- Selling Shareholders of note:

- PSTX files 8,333,333 offering by selling shareholders.

- Private Placement of Public Entity (PIPE): None of note.

- Mixed Shelf Offerings:

- AMPY files a $250 million mixed shelf offering.

- Debt/Credit Filing and Notes: None of note.

- Tender Offer: None of note.

- Convertible Offering & Notes Filed: None of note.

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close :

- After Hours Movers:

- BE +2.9%, IPSC +2.1%

- VINCE -58.4%, MAXN -8.1%, MEI -4.2%,

- News Items After the Close:

- Norwegian Cruise Lines (NCLH) to build eight new vessels and construct a multi-ship pier at Great Stirrup Cay.

- Grupo Aeroportuario Del Sureste (ASR) announces that passenger traffic for March 2024 reached a total of 6.5 million passengers, representing an increase of 6.6% year over year.

- Cohen & Steers (CNS) sees AUM grow to $81.2 billion from $79.6.

- Lifecore (LFCR) delays its 10Q.

- Lockheed Martin (LMT) awarded $272 million increase to existing contract with Missile Defense Agency,

- Exchange/Listing/Company Reorg and Personnel News:

- Methode Electronics (MEI) announces that CFO Ronald Tsoumas is retiring on July 12 and no successor named as company starts a search.

- Nova Measuring (NVMI) promotes Guy Kizner to CFO effective July 1st, he will succeed Dror David.

-

Harmonic (HLIT) CEO Patrick Harshman to retire; Nimrod Ben-Natan named new CEO.

|

- Angi Inc. (ANGI) announces the appointment of President and IAC executive Jeff Kip to CEO, succeeding Joey Levin, effective immediately

- Buyback Announcements or News: None of note.

- Stock Splits or News: None of note.

- Dividends Announcements or News: None of note.

What’s Happening This Morning: Futures value reflects the change with fair value.

S&P 500 +10, Dow Jones +50, NASDAQ +33, Russell +3. (as of 7:56 a.m. EST). Asia higher ex South Korea and Europe is lower ex FTSE this morning. VIX Futures are at 15.40 from 15.70. Gold, Silver and Copper are higher this morning for a second consecutive day. WTI Crude Oil and Brent Crude Oil are higher with Natural Gas higher as well. US 10-year Treasury sees its yield at 4.395% from 4.445%. The U.S. Dollar is lower versus the Euro, lower versus the Pound and higher against the Yen. Bitcoin is at $70,473 from $72,545 lower by -1.81% this morning.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

- Daily Positive Sectors: Utilities, Real Estate, Materials and Consumer Cyclicals of note.

- Daily Negative Sectors: Energy, Healthcare, Technology and Consumer Defensive of note.

- One Month Winners: Energy, Communication Services, Basic Materials and Industrials of note.

- Three Month Winners: Technology, Communication Services, Industrials, Energy and Financials of note.

- Six Month Winners: Technology, Financials, Industrials of note.

- Twelve Month Winners: Technology, Communication Services, and Financial of note.

- Year to Date Winners: Energy, Communication Services, Technology and Financials of note.

Upcoming Earnings Of Note:

- Wednesday Before the Open:

Earnings of Note This Morning:

- Beats: NEOG +0.11, CGNT +0.04.

- Flat: None of note.

- Misses: TLRY -0.07

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: CGNT.

- Negative Guidance: NEOG.

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: CDE +7%, NUVL +5%, NVMI +4.5%, OPFI +3.9%, PAG +3.7%, HL +3.3%, CRDF +2.9%, RKLB +2.4% of note.

- Gap Down: VINC -52.1%, MAXN -15.8%, HLIT -8.4%, LMT -2.5% of note.

Insider Action: No stock see Insider buying with dumb short selling. No stock see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- 5 Things To Know Before the Stock Market Opens Today. (CNBC)

- What You Need To Know To Start Your Day. (Bloomberg)

- Bloomberg Lead Story: Iran’s better, stealthier drones are remaking global warfare. (Bloomberg)

- Bonds recover with traders on U.S. inflation watch: Markets Wrap. (Bloomberg)

- Pfizer (PFE) sees wider use of RSV vaccine. (Bloomberg)

- March Inflation Data, expect another hot month. (Fox News)

- Bloomberg: Daybreak Podcast: Bullard sees three rate cuts this year. (Podcast)

- Bloomberg: The Big Take: Yellen warns China on overcapacity, Russia. (Podcast)

- NYT The Daily: How Tesla planted the seeds for its potential downfall. (Podcast)

- Marketplace: The hidden meanings of the AIs industry favorite words. (Podcast)

- Wealthion: Can gold thrive through inflation, Nick Colas. (Podcast)

Moving Average Update: Score improves to 71% to 51%.

Geopolitical:

- President’s Public Schedule:

- President Biden receives the Daily Briefing at 9:00 a.m. EDT.

- President Biden delivers comments on the care economy at 12:30 p.m. EDT.

- Press Briefing by Press Secretary Jean-Pierre and National Security Advisor Sullivan at 1:30 p.m. EDT.

- The President and First Lady welcome the Prime Minister of Japan and First Lady at 6:00 p.m. EDT.

Economic:

- March NFIB Small Business Optimism is due out at 6:00 a.m. EDT and came in last month at 89.40. Came in at 88.50.

- 3-Year Note Auction at 1:00 p.m. EDT.

- API Crude Oil Data at 4:30 p.m. EDT.

Federal Reserve / Treasury Speakers:

M&A Activity and News: None of note.

Meeting & Conferences of Note:

- Sellside Conferences:

- BMO CAPP Energy Conference

- Deutsche Bank Private FinTech Conference

- Goldman Sachs Private Software and Internet Conference

- Jefferies Latin America Summit

- Needham Healthcare Conference

- Top Shareholder Meetings: None of note.

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: ADCT BCLI FHTX IMUX OKYO RICK

- Update: None of note.

- R&D Day: None of note.

- Company Event: None of note.

- Industry Meetings:

-

- LD Micro

- Space Symposium

- Google Cloud Next

- Gold Forum Europe

- Spinal Cord Injury Investor Symposium

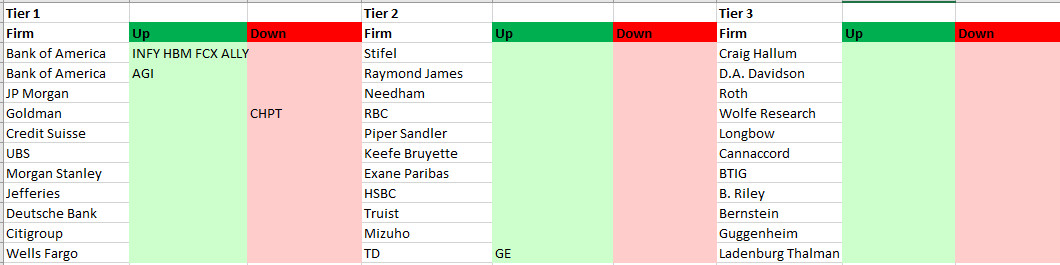

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades: