By: Bryan Gibbs, Senior Vice President, Manager of Transition Management at CAPIS

In the last article in our series on transition management, we examined how to select the proper start day and time for an event. In addition to targeting times when conditions are more favorable, this decision can be heavily influenced by the client’s individual goals.

For example, is the client going from a separately managed account to a mutual fund? If so, the transition should likely be traded on the close to whatever extent possible to minimize time out of the market and line up with the purchase of the ’40 Act fund. Other considerations abound. Is the transition multi-asset or global in nature? Are there any limitations based on desired tax outcomes? Or is it a more straightforward US equity event where one manager is being terminated and a new one is being hired? Also, why does any of this even matter?

It all comes down to performance and how to assess it. A transition manager is hired to mitigate risk on whatever asset allocation restructuring road the client chooses to take. The overall goal is to minimize costs as much as possible, but how should we go about assessing whether that was accomplished?

The simple answer: a transition manager should identify the benchmark they believe is best for the transition event well before the event occurs. This should happen on the initial planning calls – it goes hand in hand with any strategy talk. By ensuring alignment in advance, the client and transition manager can set clear expectations, establish accountability, and ensure the chosen benchmark accurately reflects the goals and constraints of the transition.

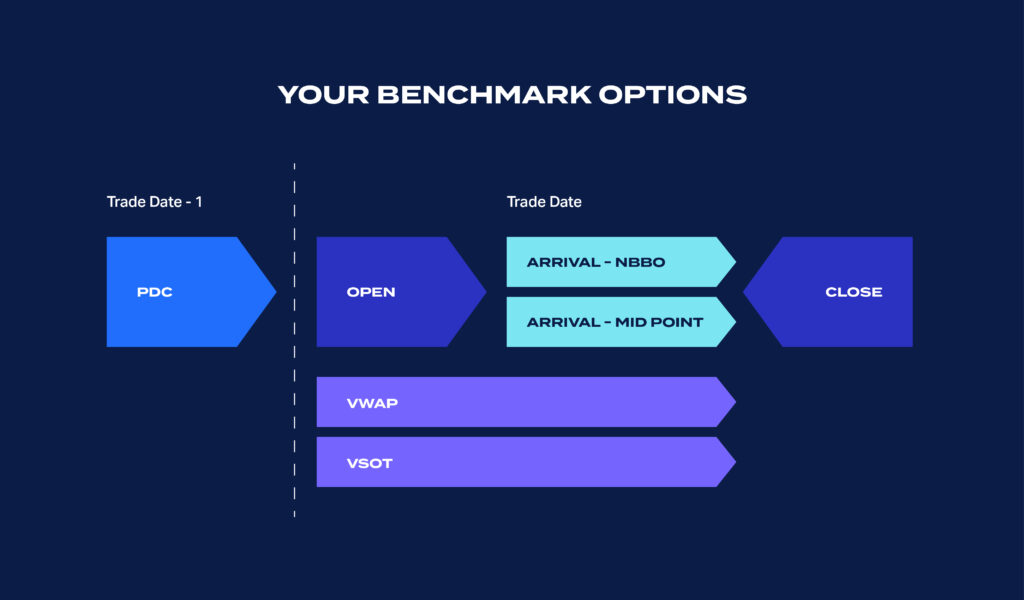

Transition Management Benchmarks: An Array of Options

Now for the more complex answer. Decades ago, when transition managers entered the scene, benchmarks were a bit of a fuzzy topic. In many ways, they still are – and too many providers fail to do their part to add clarity to the process.

We have seen post-trade analyses where providers claim to have hit their estimate spot-on, only to include an additional line item for opportunity costs that reveal they actually exceeded their estimate but are avoiding accountability for the extra cost. We’ve seen other cases where providers move the goalpost after the event is over to make them look better. To be sure, most providers handle things responsibly, but unless the client is crystal-clear from the outset on how the success of the transition will be measured, there is room for confusion, disappointment, and misdirection. With that said, what approach makes sense?

While not all approaches are created equal, there are technically situations where each of the below measures could serve as a reasonable primary benchmark. Assuming a “standard” US equity event where a terminated manager is being liquidated and a new manager is being funded, they present the following pros and cons:

Previous Day’s Close (PDC)

- Pros: Simplicity; easy visibility; not influenced by trading (as long as there is no trading that starts on the benchmark itself).

- Cons: Overnight performance can vary due to macro-level or stock-specific news before trading even starts.

Open

- Pros: Simplicity; eliminates PDC’s overnight period; earliest benchmark in the day to minimize opportunity cost risk; useful for some international events.

- Cons: Not all stocks open at the same time, so this benchmark can be highly variable, especially for small caps and micro caps. It can also be gamed – if you load illiquids on the open and get the benchmark, you will show zero cost but there will be “invisible” market impact.

Volume Weighted Average Price (VWAP)

- Pros: Looks at where the volume traded on average over the whole day; can be used in liquidation-only events going to cash where the client does not want a single point-of-time exit (or entry if a one-sided buy event). It can help tell the story by showing differences in the timing of the client’s trades versus when the majority of the volume traded on the Street.

- Cons: Can be heavily gamed in illiquid stocks, allowing providers to outperform the benchmark while masking the true market impact. Transitions aiming for this benchmark usually are open to higher opportunity cost risk.

VWAP Since Order Time (VSOT)

- Similar to VWAP, but this benchmark only references the period between the first and last trade on each stock.

Arrival Price

- Pros: An accurate indicator of performance, as there is no overnight gap and all pricing is examined at a set time; measures everything from the set time regardless when trading of specific names starts or ends.

- Cons: The set time must be agreed upon with all relevant parties before the trade date – otherwise, it can be moved around on the trade date to create better results on post-trade analysis. The provider should give clear reasons for suggesting a given start time; it can be manipulative if the provider estimates bid-ask spread cost in the pre-trade analysis but then uses Arrival NBBO (best bid or offer at the time) as the benchmark versus midpoint. In this case, the provider can get a bit of a head start and inflate performance results.

Close

- Pros: A straightforward benchmark, very useful for funds that utilize NAV end-of-day pricing; great for liquidation-only events going to passive investments to minimize time out of the market.

- Cons: Similar to the open and VWAP, trading illiquid names on the close can hide impact because you are trading on the benchmark.

For most standard transitions involving legacy and target assets, we often recommend Arrival – Midpoint as the best benchmark. While it does require a conversation beforehand and an explanation of why we want to use a given start time, this benchmark provides one of the more accurate assessments of transition manager performance. Once the primary benchmark is selected, the best practice is for the transition manager to disclose performance relative to all benchmarks somewhere in the post-trade analysis. All cards should be on the table.

When in doubt, ask questions. Remember: it is the provider’s responsibility to ensure you are comfortable with the benchmark selected and that you know their methodology, so there is no confusion when the post-trade analysis hits your inbox.