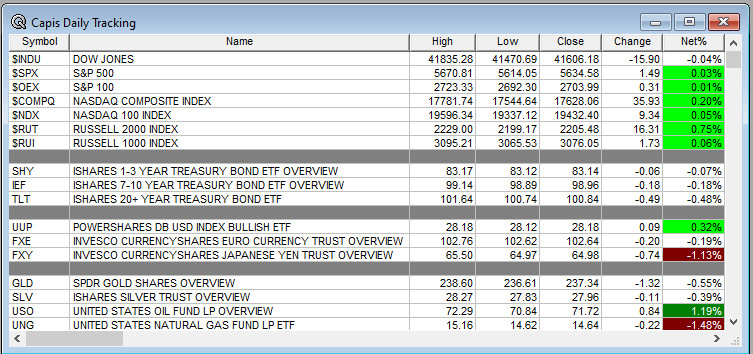

Overnight Summary: The S&P 500 closed Tuesday higher by 0.03% at 5634.58 from Monday higher by 0.13% at 5633.09. The overnight high was hit at 5711 at 2:15 a.m. EDT and the low was hit at 5698.25 at 4:15 a.m. EDT. The overnight range is 13 points. The current price is 5708 at 6:50 a.m. EDT higher by +8 points.

Most Important Article Of the Morning: “Fed Prepares to Lower Rates, With Size of First Cut In Doubt” by Nick Timiraos.

Executive Summary: Stocks are higher this morning as the Federal Reserve Open Market Committee (FOMC) concludes their two-day meeting. Yesterday, Fed Mouthpiece Nick Timiraos wrote an article in The Wall Street Journal debating 25 versus 50 basis point increase. The conclusion is they are going only 25 basis points.

- The latest FOMC Announcement is due out at 2:00 p.m. EDT.

- Presser at 2:30 p.m. EDT.

Earnings Out After The Close:

- Beats: None of note.

- Flat:

- Misses: None of note.

- IPOs For The Week: AAM, CUPR, DTSQ, FLAI, IBO, KAPA, VTRO

- New IPOs/SPACs launched/News:

- IPOs Filed/Priced:

- Secondaries Filed or Priced:

- CWST commences a proposed underwritten public offering of $400 million of its Class A common stock

- CBUS announces proposed public offering of Class A common stock

- CYTO: Pricing of up to $12.0 Million Public Offering

- FCPT: Filed Form 424B5..Up to $500,000,000

- ISPO: FORM S-3 – Secondary Offering of 9,753,105 Shares of Class A Common Stock

- Notes Priced:

- Direct Offering:

- Exchangeable Subordinate Voting Shares:

- Selling Shareholders of note:

- INVX files for 29,369,822 shares of common stock by selling shareholders

- SON: Pricing of $1.8 Billion of Senior Unsecured Notes

- Debt/Credit Filing and Notes:

- Mixed Shelf Offerings:

- EG files mixed shelf securities offering

- PIPE:

- Convertible Offering & Notes Filed:

- RUN: Prices $365 million Senior Securitization of Residential Solar & Battery Systems

- Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down After The Close:

- Movers Up: LUNR +32.6%, QTRX +4.8%, CMPO +4.5%,

- Movers Down: CBUS -11.1%, CWST -2.8%

News After The Close :

-

- EWTX to host webcast event to discuss top-line data from Phase 1 trial in Healthy Subjects and Phase 2 CIRRUS-HCM trial in patients with Obstructive Hypertrophic Cardiomyopathy (HCM) on Thursday, September 19 at 8:30 am EDT

- Microsoft (MSFT) and BlackRock (BLK) planning a $30 bln AI investment fund; Nvidia (NVDA) is joining effort as well (FT)

- Elliott Investment Management still wants to replace Southwest (LUV) CEO Robert Jordan (Reuters)

- Salesforce (CRM) and NVIDIA (NVDA) announce a strategic collaboration to develop advanced AI capabilities for the enterprise with autonomous agent and interactive avatar experiences

- LMT selected by NASA to develop lightning mapper for NOAA

- LUNR awarded a Near Space Network contract for communication and navigation services from NASA with maximum potential value of $4.82 billion

- SHAK CEO Rob Lynch appears on CNBC after the close and says time to scale

- AZPN outlines multi-year financial outlook at Investor Day; reiterates FY25 guidance

- 10-Q or 10-K Delays – None of note.

- NASDAQ Delisting Notice – None of note.

Buybacks or Repurchases: Buybacks should be slow as most companies are in a blackout period as earnings season kicks into gear.

Exchange/Listing/Company Reorg and Personnel News:

-

- GPCR promotes Blai Coll to Chief Medical Officer, effective September 18

- BLNK cutting workforce by 14%

Dividends Announcements or News:

- Stocks Ex Div Today: CRM VICI LAMR WHF JILL

- Stocks Ex Div Tomorrow: AVGO HPE BBY UWMC SNV ASO KFY VAC KLIC ELME FDUS SWBI

- JPM increases its quarterly dividend by 8.7% to $1.25/share; annual yield of 2.4%

What’s Happening This Morning: Futures S&P 500 +3 NASDAQ 100 +19.50 Dow Jones +24 Russell 2000 -1.70. Asia is higher ex China with Europe is lower this morning. VIX Futures are at 18.42 from 18.22 yesterday while Bonds are at 3.685% from 3.612% on the 10-Year. Crude Oil and Brent are lower with Natural Gas higher. Gold, Silver and Copper higher. The U.S. Dollar is lower versus the Euro, lower versus the Pound and lower against the Yen. Bitcoin is at $59,757 from $59,101 lower by -0.73% this morning.

- Daily Positive Sectors: Energy, Consumer Cyclicals and Industrials of note.

- Daily Negative Sectors: Healthcare, Consumer Defensive and Real Estate of note.

- One Month Winners: Real Estate, Utilities, Consumer Defensive, Financials, Consumer Cyclicals and Industrials of note.

- Three Month Winners: Real Estate, Utilities, Financials, Consumer Defensive, Healthcare and Industrials of note.

- Six Month Winners: Utilities, Consumer Defensive, Real Estate, Technology, Financials and Communication Services of note.

- Twelve Month Winners: Technology, Financials, Communication Services, Industrials, Utilities and Healthcare note.

- Year to Date Winners: Technology, Utilities, Financials, Communication Services, Consumer Defensive and Healthcare of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Wednesday After the Close: SCS of note

- Thursday Before The Open: FDS DAVA CBRL of note

Earnings of Note This Morning:

- Beats: GIS +0.01 of note.

- Flat:

- Misses: None of note.

- Still to Report:

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative or Mixed Guidance: None of note.

Advance/Decline Weekly Update With Both Daily and Weekly Stats: Markets have improved nicely in the last week. The Daily A/D Line has made a new high while the S&P 500 has yet to. A bit of a divergence currently.

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: LUNR +47.6%, IAUX +6.5%, BAK +3.3%, QTRX +3.2%, GLNG +3.1%, EWTX +2.6%, CMPO +2.5%

- Gap Down: CBUS -16.8%, CWST -3.5%

Insider Action: QTRX see Insider buying with dumb short selling. None of note see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- What You Need To Know to Start Your Day. (Bloomberg)

- 5 Things To Know Before The Market Opens. (CNBC)

- Pre-Market Movers: (CNBC)

- Bloomberg Lead Story: Fed to Kick Off Rate Cuts. (Bloomberg)

- Markets Wrap: US Futures in Watchful Mood. (Bloomberg)

- Weekly Mortgage Applications were out at 7:30 a.m. EDT and rose 14.2% from 1.4% last week.

- Speaker Mike Johnson (R-LA) interviewed on CNBC over potential government shutdown in 13 days.

- Chevron (CVX) CEO blames White House for increased energy prices. (FT)

- Taiwan Semi (TSM) to fabricate chips for Apple (AAPL) in Arizona. (Tim Culpan)

- Google (GOOGL) will not have to pay 1.49 billion EURO fine for blocking rival advertisers. (BBC)

- EU however may go after META now. (FT)

- FDA approves Merck’s (MRK) treatment for pleural mesothelioma. (OncLive)

- Bloomberg: The Big Take – Hedge Funds breed startups to the tune of $14 billion. (Podcast)

- Bloomberg: Odd Lots – PIMCO take on Fed Day and Beyond. (Podcast)

- Wealthion: Weekly Recap – A concerned Fed will drive liquidity and markets higher. (Podcast)

Economic:

- August Housing Starts is due out at 8:30 a.m. EDT and are expected to rise to 1,320,000 from 1,238,000.

- Weekly Crude Oil Numbers are due out at 10:30 a.m. EDT.

Geopolitical:

- President Biden receives the Daily Briefing at 12:45 p.m. EDT.

- Press Briefing at 1:30 p.m. EDT by Press Secretary Karine Jean-Pierre.

- President Biden meets with at 2:15 p.m. EDT.

Federal Reserve Speakers:

- Blackout period ends today when Chairman Powell speaks.

- The latest FOMC Announcement is due out at 2:00 p.m. EDT.

M&A Activity and News:

- None of note.

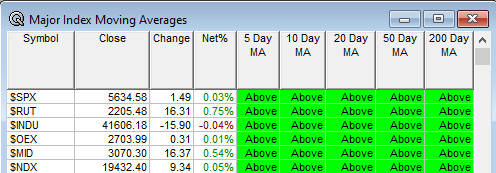

Moving Averages On Major Indexes: Remains at 100% of the moving averages being positive.

Meeting & Conferences of Note:

-

- Sellside Conferences:

- Bank of America Global Healthcare Conference

- Cantor Fitzgerald Global Healthcare Conference

- D. A. Davidson Diversified Industrials & Services Conference

- JP Morgan U.S. All Stars Conference

- Noble Basic Industries Equity Conference

- Pickering Energy Conference

- Sidoti Small Cap Conference

- Stifel Immunology and Inflammation Virtual Summit

- Wells Fargo Consumer Conference

- Fireside Chat: None of note.

- Top Shareholder Meetings: CAG, DRI, SCHL, TTWO

- Investor/Analyst Day/Calls: AVY, CRWD, FDMT, HUBS, IMNN, PECO, SSNC, TMUS, TRUP, VNDA

- Update: None of note.

- R&D Day: None of note.

- Sellside Conferences:

-

- FDA Presentation:

- VNDA: Data Presentation Tradipitant

- RHHBY: Data Presentation Fenebrutinib

- Company Event:

- Industry Meetings or Events:

- Denver Gold Forum

- European Geriatric Medicine Society (EuGMS) Congress

- LABScon: The Ultimate Cybersecurity Research Conference

- Single Cell Genomics Conference

- World Satellite Business Week (WSBW)

- FDA Presentation:

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Upgrades:

Downgrades: