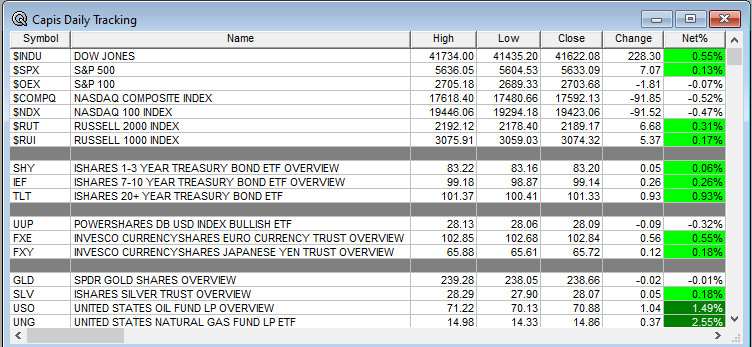

Overnight Summary: The S&P 500 closed Monday higher by 0.13% at 5633.09 from Friday higher by 0.54% at 5626.02. The overnight high was hit at 5721.25 at 6:10 a.m. EDT and the low was hit at 5690.50 at 9:20 p.m. EDT. The overnight range is 31 points. The current price is 5716 at 6:55 a.m. EDT higher by +16.75 points.

Most Important Article Of the Morning: Fed to Cut Quarter of a Point According to CNBC Survey. (CNBC)

Executive Summary: Stocks are higher this morning as the Federal Reserve Open Market Committee (FOMC) begins their two-day meeting. In a rather laughable move, Intel flooded the market with a series of news stories is a desperate attempt to right its stock that is near lows not seen since 2013.

- 20-Year Bond Auction at 1:00 p.m. EDT.

Earnings Out After The Close:

- Beats: None of note.

- Flat:

- Misses: None of note.

- IPOs For The Week: AAM, CUPR, DTSQ, FLAI, IBO, KAPA, VTRO

- New IPOs/SPACs launched/News:

- IPOs Filed/Priced:

- Secondaries Filed or Priced:

- APVO: $3.0 Million Offering Priced At-the-Market Under Nasdaq Rules

- GCTK: Form S-1 Offering common stock

- NUVL: Pricing of Upsized Public Offering of Common Stock.. 5,000,000 shares @$100

- SONM: Form S-3.. Up to 700,000 Shares of Common Stock Including up to 350,000 Shares of

Common Stock Issuable upon Exercise of Warrants - VMAR – Closing of Common Share Offering

- XXII – Form S-3.. 1,399,776 Shares of Common Stock

- Notes Priced:

- Direct Offering:

- Exchangeable Subordinate Voting Shares:

- Selling Shareholders of note:

- Debt/Credit Filing and Notes:

- Mixed Shelf Offerings:

- EG files mixed shelf securities offering

- PIPE:

- BOX files $400 mln convertible notes offering in a private placement to qualified institutional buyers

- DRMA: $3.5 Million Private Placement Priced At-The-Market Under Nasdaq Rules

- Convertible Offering & Notes Filed:

- MSTR to offer $700 mln aggregate amount of convertible senior notes due 2028

- Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down After The Close:

- Movers Up: INTC +8.7%, CMNC +3%, IMAB +2.8%

- Movers Down: ARAY -5%, BOX -2.4%, RCAT -2%, CPF -2%

News After The Close :

-

- INTC and AMZN announce co-investment in custom chip designs under a multi-year, multi-billion-dollar framework involving product and wafers from Intel.

- INTC to turn foundry business into a subsidiary that could allow it to raise outside funding. (CNBC)

- INSG enters into a definitive agreement to sell its fleet management and telematics business in an all-cash transaction for $52 million

- INTC continues to climb afterhours; to postpone new factories in Germany and Poland. (Bloomberg)

- Steel Dynamics (STLD) guides lower with EPS of $1.94 to $1.98 from $2.04.

- Starbucks (SBUX) North America CEO Michael Conway to retire, effective November 30

- 10-Q or 10-K Delays – ARAY, RCAT of note.

- NASDAQ Delisting Notice – None of note.

Buybacks or Repurchases: Buybacks should be slow as most companies are in a blackout period as earnings season kicks into gear.

- Microsoft (MSFT) plans $60 billion stock buyback. (Bloomberg)

Exchange/Listing/Company Reorg and Personnel News:

-

- UDMY to eliminate approximately 280 of its employees; expects to rehire around half of the impacted roles, primarily in lower cost geographies

- TCPC Chairman and CEO Rajneesh Vig to resign as Chairman and CEO and continue serving on Board until January 31, 2025; appoints new Chairman and CEO

- SGA promotes Wayne Leland to COO

- CHD promotes Richard Dierker to President and CEO, effective March 31; Matt Farrell to continue as Chairman through transition period

- HR CFO Kris Douglas to step down; names Rob Hull as COO; reaffirms Q3 and FY24 guidance

- Starbucks (SBUX) North America CEO Michael Conway to retire, effective November 30

Dividends Announcements or News:

- Stocks Ex Div Today: LRCX APH ECL VRT PHM CINF HBAN BSY EXP JJSF ATAT GDEN

- Stocks Ex Div Tomorrow: CRM VICI LAMR WHF JILL

- Microsoft (MSFT) to raise dividend 10%. (Bloomberg)

What’s Happening This Morning: Futures S&P 500 +23 NASDAQ 100 +126 Dow Jones +131 Russell 2000 +13. Asia is higher ex Japan with Europe is higher this morning. VIX Futures are at 18.22 from 18.17 yesterday while Bonds are at 3.612% from 3.63% on the 10-Year. Crude Oil and Brent are higher with Natural Gas lower for a second day in a row. Gold and Silver are lower with Copper higher. The U.S. Dollar is lower versus the Euro, lower versus the Pound and lower against the Yen. Bitcoin is at $59,101 from $58,747 higher by 2.02% this morning.

- Daily Positive Sectors: Energy, Financials, Utilities, Communication Services and Materials of note.

- Daily Negative Sectors: Technology and Consumer Cyclicals of note.

- One Month Winners: Real Estate, Utilities, Consumer Defensive, Financials,

Healthcare, Consumer Cyclicals and Industrials of note. - Three Month Winners: Real Estate, Utilities, Financials, Consumer Defensive, Healthcare and Industrials of note.

- Six Month Winners: Utilities, Consumer Defensive, Real Estate, Technology, Financials and Communication Services of note.

- Twelve Month Winners: Technology, Financials, Communication Services, Industrials, Utilities

Consumer Defensiveand Healthcare note. - Year to Date Winners: Technology, Utilities, Financials, Communication Services, Consumer Defensive and Healthcare of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Tuesday After the Close: None of note

- Wednesday Before The Open: None of note

Earnings of Note This Morning:

- Beats: None of note.

- Flat:

- Misses: None of note.

- Still to Report:

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative or Mixed Guidance: None of note.

Advance/Decline Weekly Update With Both Daily and Weekly Stats: Markets have improved nicely in the last week.

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: INTC +6.7%, DADA +6.6%, HITI +5.5%, IMAB +4.7%, HPE +3.5%, MSTR +2.8%, INSG +2.3%, TPG +2.3%, SGML +2%, CLF +2%, MSFT +2%

- Gap Down: NUVL -2.9%, BOX -2.5%

Insider Action: ACDC GTLS see Insider buying with dumb short selling. TTSH sees Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- What You Need To Know to Start Your Day. (Bloomberg)

- 5 Things To Know Before The Market Opens. (CNBC)

- Pre-Market Movers: MSFT SHOP INTC (CNBC)

- Bloomberg Lead Story: Markets Hinge On Powell Emulating Greenspan’s Soft Landing. (Bloomberg)

- Markets Wrap: Stocks rise with retail data in focus ahead of Fed. (Bloomberg)

- Hedge Fund Managers David Tepper and Michael Burry up their bets on China. (CNBC)

- Bloomberg: The Big Take – Trump’s Banker Brawls With Whistleblowers, Marxists and Shorts. (Podcast)

- Wealthion: Weekly Recap – Why Fed Rate Cuts won’t save us. (Podcast)

Economic:

- August Retail Sales is due out at 8:30 a.m. EDT and expected to fall by -0.20% after last month at 1.0%.

- At the same time, August Industrial Production is due out and expected to rise by 0.1% from -0.60% in July.

- September NAHB Housing Market Index is due out at 10:00 a.m. EDT and is expected to grow to 41 from 39.

- Weekly API Crude Oil Numbers are due out at 4:30 p.m. EDT.

Geopolitical:

- President Biden receives the Daily Briefing at 12:45 p.m. EDT.

- Press Briefing at 1:30 p.m. EDT by Press Secretary Karine Jean-Pierre.

- President Biden meets with the President of the World Bank at 2:15 p.m. EDT.

Federal Reserve Speakers

- Federal Reserve speakers are in blackout period this week and through Wednesday.

M&A Activity and News:

- None of note.

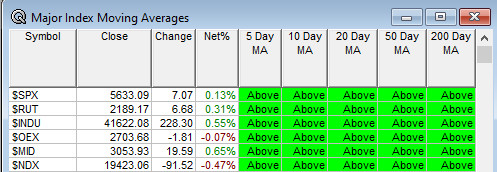

Moving Averages On Major Indexes: Remains at 100% of the moving averages being positive.

Meeting & Conferences of Note:

-

- Sellside Conferences:

- Cantor Fitzgerald Global Healthcare Conference

- CL King & Associates Best Ideas Conference

- Goldman Sachs European Communacopia Conference

- Janney Financial Services Conference

- JP Morgan U.S. All Stars Conference

- Maxim Gaming Media & Entertainment Virtual Conference

- Stephens Annual Bank Forum

- Stifel Immunology and Inflammation Virtual Summit

- TD Cowen Sip Snack and Scrub Summit

- Fireside Chat: None of note.

- Top Shareholder Meetings: AIR, BBLG, GOVX, SWBI

- Investor/Analyst Day/Calls: AIRE, AZPN, EA, KOP, RRX, SNAP, WDAY

- Update: None of note.

- R&D Day: None of note.

- Sellside Conferences:

-

- FDA Presentation:

- ADAG: Data Presentation ADG126 (CTLA4) + Pembrolizumab

- PRLD: Data Presentation PRT3789

- Company Event:

- Industry Meetings or Events:

- AACR Special Conference on Advances in Pancreatic Cancer Research

- CIRSE Annual Congress

- Denver Gold Forum

- ESMO Congress

- GENEWIZ Week Event

- Insight Tech Conference

- Pickering Energy Partners TE&M Fest

- Single Cell Genomics Conference

- Snap Partner Summit

- FDA Presentation:

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Upgrades: SHOP RLMD LSCC HPE GEV DCOM BNTX APP

Downgrades: SEDG