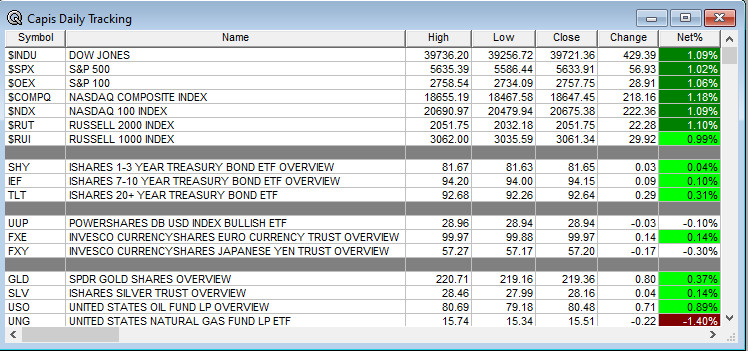

Overnight Summary: The S&P 500 closed Wednesday higher by 1.02% at 5633.91 from Tuesday higher by 0.07% at 5576.98. The overnight high was hit at 5,687 at 4:05 p.m. EDT and the low was hit at 5680.25 at 7:25 a.m. EDT. The overnight range is 7 points. The current price is 5680.75 at 7:33 a.m. EDT lower by -7.25 points.

- June CPI is due out at 8:30 a.m. EDT and is expected to rise to 0.1% from 0.0%.

- 30-Year Treasury Note Auction at 1:00 p.m. EDT.

- Beats: AZZ +0.16, PSMT +0.07, WDFC +0.07 of note.

- Flat: None of note.

- Misses: of note.

- Yet to Report:

Capital Raises:

- IPOs For The Week: ACTU, AZI, MJID, MSW, ORKT, OSTX, PGHL, QMMM, WOK

- New IPOs/SPACs launched/News:

- IPOs Filed/Priced:

- Secondaries Filed or Priced:

- CTNT: FORM S-1 – Up to 6,479,665 Shares of Class A Common Stock.

- DMAC: FORM S-3 – 4,720,000 COMMON SHARES

- ECOR: FORM S-1 – 1,924,960 shares of Common Stock

- SEZL: FORM S-3 – Common Stock 3,414,736 Shares

- Notes Priced:

- REZI: Upsize and Pricing Of 6.500% Senior Notes Due 2032

- Direct Offering:

- Exchangeable Subordinate Voting Shares:

- Selling Shareholders of note:

- SEZL files for 3,414,736 shares of common stock by selling shareholders.

- DMAC files for 4,720,000 shares of common stock by selling shareholders.

- Debt/Credit Filing and Notes:

- Mixed Shelf Offerings:

- CBAT files $500 mln mixed shelf securities offering.

- .

- PIPE:

- Convertible Offering & Notes Filed:

- Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down After The Close:

- Movers Up: WDFC +11.5%, PSMT +5.1%, COST +2.2%.

- Movers Down: SEZL -11%, ETWO -10.2%, CBAT -3.4%, BSET -2.1%.

News After The Close :

-

- S&P 500 sets 37th record close in 2024.

- Franklin Resources (BEN) sees AUM rise to $1.65 from $1.64 trillion.

- AllianceBernstein (AB) sees AUM rise $769 from $757 billion.

- Invesco (IVZ) sees AUM rise to 1.715 a rise of 1.7% from May.

- COST reports June adjusted comps of +6.9%; also to increase membership fees by $5 for non-exec and $10 for executive memberships.

- AA guides Q2 EPS and revs above consensus.

- C down over 1% after U.S. regulators fine the company $136 mln for failing to make adequate progress fixing data issues. (Reuters)

Buybacks or Repurchases:

- None of note.

Exchange/Listing/Company Reorg and Personnel News:

- ZWS promotes Dave Pauli to CFO.

- IPI elects Barth Whitham as its Board Chair; initiates search for a successor to CEO Bob Jornayvaz.

Dividends Announcements or News:

- Stocks Ex Div Today: ORCL ACN GE KAI GNL

- Stocks Ex Div Tomorrow: MRVL AMX IEX MORN AEO AAP BKE TEN

What’s Happening This Morning: Futures S&P 500 -7, NASDAQ 100 -13.25, Dow Jones -73 Russell 2000 +0.25. Asia and Europe are higher this morning. VIX Futures are at 13,00 from 13.01 yesterday while Bonds at 4.201% from 4.277% yesterday on the 10-Year. Crude Oil and Brent are higher with Natural Gas lower. Gold and Silver are higher with Copper lower. The U.S. Dollar is lower versus the Euro, lower versus the Pound and lower against the Yen. Bitcoin is at $58.875 from $58,548 higher by 2.47% this morning.

- Daily Positive Sectors: All positive of note.

- Daily Negative Sectors: None were negative of note.

- One Month Winners: Technology, Communication Services, Consumer Cyclical and Energy of note.

- Three Month Winners: Technology, Communication Services, Utilities, Consumer Cyclical and Consumer Defensive of note.

- Six Month Winners: Technology, Communication Services, Financials and Consumer Cyclicals of note.

- Twelve Month Winners: Technology, Communication Services, Financials, Energy, Industrials, and Consumer Cyclical of note.

- Year to Date Winners: Technology, Communication Services, Financials, Consumer Defensive, Energy and Healthcare of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Thursday After the Close: None of note.

- Friday Before The Open: JPM WFC C FAST ERIC of note.

Earnings of Note This Morning:

- Beats: PEP +0.12, CAG +0.04 of note.

- Flat: None of note.

- Misses: DAL -0.01 of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative Guidance: CAG DAL PEP of note.

Erlanger Research Advance/Decline Chart: Remains awful for NASDAQ and weak for NYSE.

Gap Ups & Down In Early Pre-Market (+4% or down more than -4%):

- Gap Up: WDFC +12.4%, AKBA +6.5%, PSMT +5.1%, RPAY +4.4%, COST +3.1%, AA +2.6%, DSGR +2% of note.

- Gap Down: ETWO -11.2%, CBAT -9.4%, DAL -7.3%, NKLA -5.1%, AZZ -4.6%, CPA -3%, HEAR -2.6%, SEZL -2.5%, PEP -2.4%, SBSW -2.1% of note.

Insider Action: ASPI and BNED see Insider buying with dumb short selling. No stocks sees Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- What Your Need to Know to Start Your Day. (Bloomberg)

- Market Wrap: U.S. futures stay in holding pattern before CPI data. (Bloomberg)

- Bloomberg Lead Story: U.S. Inflation Data to Bolster Case For Fed Rate Cut in September. (Bloomberg)

- China cracks down on short sales. (Bloomberg)

- Barron’s out positive on TSLA, DPZ and RMD. (Barron’s)

- Delta’s (DAL) outlook falls short of expectations. (CNBC)

- Pepsi (PEP) sees U.S. demand weaken. (CNBC)

- Pfizer (PFE) moves forward with once daily weight loss pill. (CNBC)

- Bloomberg: The Big Take: Drones reshape Ukraine frontlines. (Podcast)

Economic:

- June CPI is due out at 8:30 a.m. EDT and is expected to rise to 0.1% from 0.0%.

- Weekly Jobless Claims are due out at 8:30 a.m. EDT.

- Weekly Natural Gas Inventories are due out at 10:30 a.m. EDT.

Geopolitical:

- President Biden receives the President’s Daily Briefing at 9:00 a.m. EDT.

- President Biden meets with NATO Allied Leaders to the NATO Summit at 10:00 a.m. EDT. Then continues after 2:00 p.m. EDT.

- President Biden meets with Ukraine President Zelensky at 1:30 p.m. EDT.

Federal Reserve Speakers

- Federal Reserve Atlanta President Raphael Bostic speaks at 11:30 a.m. EDT.

- Federal Reserve St, Louis President Alberto Musalem speaks at 1:00 p.m. EDT.

M&A Activity and News:

- None of note.

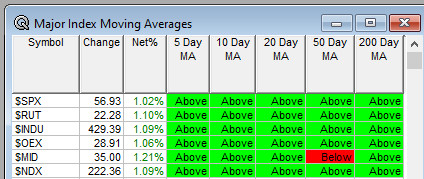

Moving Averages On Major Indexes: Moves from 70% to 97% of the moving averages are now positive.

Meeting & Conferences of Note:

- Sellside Conferences:

- Bank of America Healthcare Conference

- Mizhuo Therapeutics Expert Seminar

- UBS Retail Bus Tour

- Fireside Chat: None of note.

- Top Shareholder Meetings: CHWY, DUO, FAM, GTLB, MFD, MGRC, PL, RENT, SNES

- Investor/Analyst Day/Calls: ACLS, IMMP, PPBT, SEED, SKIL

- Update: None of note.

- R&D Day: None of note.

- FDA Presentation:

- Company Event:

- Industry Meetings:

- SEMICON West

- European Society for Medical Oncology (ESMO) Virtual Plenary Session

- AI Governance Conference

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Upgrades: CASY RSG OC ITRI ASTH

Downgrades: ON MCHP DRI