Overnight Summary & Early Morning Trading:

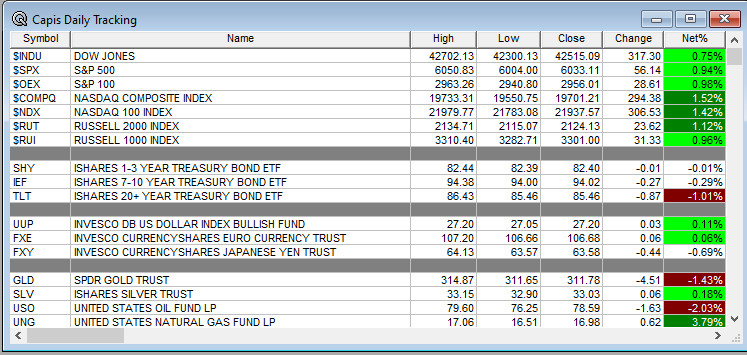

- The S&P 500 finished Monday higher by 0.90% at 6033.11 from Friday lower by -1.13% at 5976.97.

- Futures are lower this morning by -34.50 (-0.59%) at 6054 around 6:20 a.m. EDT.

- The cash range is now 100 points on the S&P 500 cash for the year, 6000 to 6100. Year to date the S&P 500 is up by 2.52% from 1.62% on Friday’s close.

Executive Summary:

- Last week, markets received weak inflation data. This week the FOMC meets and the $64,000 question is will they take that data and begin to cut rates? Markets are betting on no cuts but the language could change towards cutting down the road and that could surprise markets.

Quote of the Day:

- “I have not reached out to Iran for “Peace Talks” in any way, shape, or form. This is just more HIGHLY FABRICATED, FAKE NEWS! If they want to talk, they know how to reach me. They should have taken the deal that was on the table – Would have saved a lot of lives!!! ” President Trump on Truth Social

Breaking News: None of note.

Key Events of Note Today:

- Busy morning with Retail Sales, Industrial Production and NAHB Housing Data all out by 10:00 a.m. EDT.

- 5-Year TIPS Auction at 1:00 p.m. EDT.

- Fed Speak speakers in blackout until after next week’s meeting.

- President Trump is back from Canada and the G-7 Meeting for emergency meetings at the White House on Iran and Israel conflict.

Notable Earnings Out After The Close:

- Beats: None of note.

- Misses: LEN -0.13 of note.

- Flat: None of note.

- IPOs For The Week: CAI, SLDE of note.

- New IPOs/SPACs launched/News: None of note.

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced:

- RDW commences $200 million common stock offering.

- MMYT files for ordinary share offering

- BURU: Form S-1.. Up to 47,202,891 Shares of Common Stock

- Notes Priced:

- KIM – Pricing of $500 Million Aggregate Principal Amount of 5.300% Notes due 2036

- Notes Files: None of note.

- Convertibles Filed: None of note.

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Private Placements: None of note.

- Selling Shareholders of note:

- CTRI commences public offering of 9.5 million shares of common stock by Southwest Gas Holdings (SWX) who is a shareholder.

- LTM files prospectus supplement, selling shareholders offering a total of 10 million ADSs.

- Mixed Shelf Offerings:

- KAVL: Form S-3.. $100,000,000 Mixed Shelf

News After The Close:

- The Real Real (REAL) pays the remaining $26,749,000 in aggregate principal amount of its 3% Convertible Senior Notes due 2025.

- Cushman & Wakefield (CWK) midyear release sees, “… property markets are expected to be resilient before gaining more momentum in 2026 as a stronger growth backdrop emerges.”

- Microsoft (MSFT) drifts modestly lower as tensions with OpenAI reach boiling point with OpenAI discussing marking antitrust complaints to regulators.

- Senate Republicans to omit Medicare Advantage cuts, but proposes more aggressive Medicaid cuts. (Bloomberg)

- UnitedHealth (UNH) ticks slightly lower as company cuts commissions for brokers on some Medicare Advantage Plans. (Bloomberg)

- U.S. clears potential $2 billion sale of fighter jet parts to Australia, with Boeing (BA) as lead contractor.

- President Trump confirms implementation of UK/US trade deal.

Exchange/Listing/Company Reorg and Personnel News:

- DADA completes going private transaction, ceases being a publicly traded company.

- FSLY appoints Kim Compton as CEO, effective immediately.

- VMEO announces that Gillian Munson will step down as CFO, effective August 8; co retains an external search firm to identify candidates for the CFO role.

- BLDP CEO Randy MacEwen to step down, with Marty Neese assuming the position, effective July 7.

- FVR terminates CFO Randall Starr for cause, effective immediately.

Buybacks:

- FITB approves a new share repurchase authorization of up to 100 million shares

Dividends Announcements or News

- Stocks Ex Div Today of note: APH PLD ECL HBAN PHM AEG TTC GEFB GEF JJSF WKC UPBD ELME

- Stocks Ex Div Wednesday of note: None of note.

- Millrose (MRP) first full quarterly dividend declared following its spin-off from Lennar.

Stocks Moving Up & Down After The Close:

- Gap Up: APPS +10.6%, LEN +3.5% of note.

- Gap Down: RUN -27.5%, SEDG -23%, ENPH -15.5%, FSLR -10%; MMYT -10.8%, RDW -9.5%, TCOM -5.4%, CTRI -4.6%, BLDP -2.8% of note.

What’s Happening This Morning: (as of 7:42 a.m. EDT)

- Futures S&P 500 , NASDAQ 100 , Dow Jones . Europe is lower while Asia is lower ex Japan. Bonds are at 4.42% on the 10-Year unchanged for a second day. Crude Oil and Brent Crude are higher with Natural Gas higher as well. Gold is lower while Silver is higher and Copper lower. The U.S. Dollar is lower versus the Euro, higher against the Pound and lower against the Yen. Bitcoin is at $105.924 from $106,890 lower by $-2752 (-2.50%).

- Daily Positive Sectors: Technology, Communication Services, Consumer Cyclical, Financials and Industrials.

- Daily Negative Sectors: Energy, Utilities and Healthcare were notable for lower gains.

- One Month Winners: Healthcare, Energy, Basic Materials, and Communication Services of note.

- Three-Month Winners: Technology, Industrials, Communication Services of note.

- Six-Month Winners: Communication Services, Financials, Utilities of note.

- Twelve-Month Winners: Financials, Communication Services, Technology, Consumer Cyclical, Industrials and Utilities and of note.

- Year to Date Winners: Materials, Financials, Utilities, Industrials and Communication Services of note.

Bolded means the Sector is new to the period in which it falls.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Tuesday After the Close: LZB of note.

- Wednesday Before The Open: GMS KFY of note.

Notable Earnings of Note This Morning:

- Beats: WILY +0.10 of note.

- Misses: None of note.

- Still to Report: JBL of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative or Mixed Guidance: None of note.

Advance/Decline Daily Update: The A/D Line was improved on Monday.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: SATS +48.4%,APPS +10.2%, FFAI +2.7%, LEN +2.1%, of note.

- Gap Down: RUN -26.8%, SEDG -21%, ENPH -16.8%, RDW -12.1%, FSLR -10.8%, MMYT -7.5%, AMBC -4.3%, CTRI -2.7%, LTM -2.5%, of note.

Insider Action: No stock sees Insider Buying with dumb short selling. No stock sees Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Bloomberg Lead Story: Trump Plays Down a Cease Fire Between Iran and Israel in Favor of A “Real End”. (Bloomberg)

- Markets Wrap: Stock Futures fall as Mid East risks rise. (Bloomberg).

- Trump Smart Phone to be made in China for $499. You cannot make this up. (CNBC)

- Solar stocks getting killed this morning, under pressure after hours on report Senate tax committee proposed a full phase-out of solar and wind energy tax credits by 2028.

- Big Take: Iran’s Leaders face a reckoning as Israel strikes intensify. (Podcast)

Bolded on story link means behind a Pay Wall.

Economic & Geopolitical:

- Federal Reserve Speakers none of note today as they are in a blackout until this week’s meeting is over.

- Economic Releases:

- May Retail Sales are due out at 8:30 a.m. EDT and are expected to fall to -0.60% from 0.10%

- May Industrial Production is due out at 9:15 a.m. EDT and expected to improve to 0.0% from 0.1% last month.

- June NAHB Housing Market Index is due out at 10:00 a.m. EDT and expected to rise to 36 from 34.

- Weekly API Petroleum Data is due out at 10:30 a.m. EDT.

- President Trump’s Daily Schedule.

- President Trump participates in Bilateral Meetings today with the Presidents of Mexico and Ukraine with no pre-announced time.

- President Trump is in Canada for the G-7 and a separate meeting with the President of Canada.

M&A Activity:

- Eli Lilly (LLY) to be Verve (VERV) for $1.3 billion.

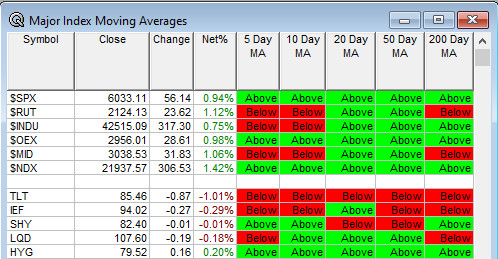

Moving Average Table: Moves to 74% from 43% for Equities. Bonds imploded.

Meeting & Conferences of Note:

- Sellside Conferences:

- Citi European Healthcare Conference

- Citizens Medical Devices and Healthcare Services Forum

- Goldman Sachs Global Copper Week

- Jefferies Consumer Conference

- Stephens Investor Conference

- Stifel Summer Solstice Conference

- Truist Securities MedTech Conference

- Wolfe’s Materials of the Future Conference

- Shareholder Meetings: ARI, CROX, DADA, HCI, GES, NXDT, TJX, TLRY, TWLO

- Top Analyst, Investor Meetings: AGEN, BKKT, BRN, CLS, GE, MET, MRVL, PENN, PSEC, SLM, VUZI, ZTO

- Fireside Chat: None of note.

- FDA Presentation: None of note.

- R&D Day: None of note.

- Meetings:

- BIO International Convention

- IEEE Optical Interconnects and Packaging Conference

- NYSE European Investor Conference

- Paris Air Show

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Upgrades: COO ALKS ROKU of note.

Downgrades: RIG HCAT SAGE of note.