Overnight Summary & Early Morning Trading:

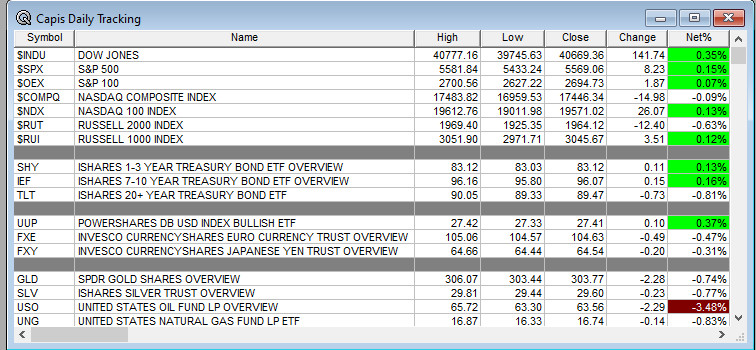

- The S&P 500 finished Wednesday higher by 0.15% at 5569.06. Tuesday higher by 0.58% at 5560.83. Futures are higher this morning by +74 (+1.33%) at 5661 around 6:25 a.m. EDT. The range is now 600 points on the S&P 500 cash for the year, 5500 to 6100. Year to date the S&P 500 is down -5.31% from -5.45% Tuesday’s close.

Executive Summary:

- Stocks are beginning to trade with less volatility as the VIX is down to 23.25 from 23.50 yesterday morning.

Quote of the Day: None ofnote.

Key Events of Note Today:

- 4-Week T-Bill Auction at 11:30 a.m. EDT.

Notable Earnings Out After The Close:

- Beats: BKNG +7.47, NBR +5.10, HURN +0.52, QRVO +0.42, UMBF +0.39, LFUS +0.38, FICO +0.36, ACGL +0.22, EIX +0.16, STX +0.16, FLS +0.12, MDLZ +0.10, PPG +0.10 and V +0.08 of note. (Greater than $0.08)

- Misses: FSLR -0.54, CZR-0.34, WERN -0.24, UNM -0.15, SBUX -0.08, WPC -0.03 and LC -0.01 of note.

- Flat: None of note.

- IPOs For The Week: ALEH, EGG, OMSE, YB

- New IPOs/SPACs launched/News: None of note.

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced:

- BCDA: Form S-3.. 813,636 Shares of Common Stock

- CREG: FORM S-1 – 8,029,851 Shares of Common Stock

- SGBX: Form S-1.. 989,795,760 Shares of Common Stock

- YOSH: Form S-1.. 3,005,600 Shares of Common Stock:

- Notes Priced: None of note.

- Notes Files: None of note.

- Convertibles Filed: None of note.

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Private Placements: None of note.

- Selling Shareholders of note:

- KREF files for 13,079,454 share common stock offering by selling shareholders

- Mixed Shelf Offerings:

- KREF files for $750 million mixed securities shelf offering.

- VICI files mixed securities shelf offering.

- ASPI files for $100 million mixed securities shelf offering.

News After The Close:

- 10K or Qs Filings/Delays – (Filed), NNDM ESEA(Delayed) None of note.

- Microsoft (MSFT) beats

- Meta (META) beats as well

- Qualcomm (QCOM) lower on guidance that was mixed.

- Jacobs Solutions (J) announces that its Board of Directors approved a special dividend of 7,299,065 shares of common stock of Amentum Holdings (AMTM) distributable to Jacobs’ shareholders of record as of the close of business on May 16, 2025.

- GD awarded $12 billion contract modification for Virginia-Class Submarines.

- BAH awarded a $743 mln US Air Force task order.

- Olol (OLO) +12% higher after hours on report it is exploring a potential sale. (Bloomberg)

Exchange/Listing/Company Reorg and Personnel News:

- EBAY announces that Chief Financial Officer Steve Priest will be leaving the Company.

- BLKB announces the promotion of Chad Anderson to executive vice president and chief financial officer.

- COO announces that its Board of Directors has appointed Barbara Carbone as an independent director, effective May 1, 2025.

Buybacks:

- POOL and authorizes an increase in the company’s share repurchase program to $600.0 mln

- ACT authorizes a new share repurchase program under which the company may purchase up to $350 mln of its common stock.

- MET has approved a new $3 billion authorization for the company to repurchase its common stock.

- MGM authorized $2 billion buyback.

Dividends Announcements or News:

- Stocks Ex Div Today: AON O NRG CASY PAGP PAA ALLY ATR AES AVAL VSEC WSR

- Stocks Ex Div Tomorrow of note: COST SCCO CARR NSC DHI ETR WES SBS EWBC BKRIY PNFP LW HXL HOPE CDRE AGRO

- POOL increases quarterly cash dividend 4% to $1.25/share from $1.20/share.

- ACT increases quarterly dividend 14% to $0.21/share from $0.185/share.

- NBHC increases quarterly cash dividend 3.4% to $0.30/share from $0.29/share.

- AKTR increases quarterly cash dividend to $0.33/share from $0.32/share.

Stocks Moving Up & Down Yesterday:

- Gap Up: TTMI +12.9%, ALGN +11%, MAX +10.3%, NTGR +9.9%, RSI +9.3%, TNDM +8.4%, MSFT +7.8%, DLX +7.7%, MGY +7.4%, FORM +6.6%, CNMD +5.6%, WEX +5.5%, CHRW +5.3%, AEIS +5%, META +5%, WAY +4.9%, GH +4.8%, SPOK +4.6%, VAL +4.1%, ALKT +4%, MGM +3.9%, MCW +3.4%, MYRG +3%, NYMT +2.9%, CACC +2.6%, TS +2.5%, CGNX +2.2%, EQIX +2/1of note.

- Gap Down: CFLT -10%, PPC -8.2%, AGI -6.9%, GKOS -6.7%, TFSL -6%, QCOM -5.8%, ICLR -4.9%, CTOS -4.6%, AVB -4.1%, GL -4%, CDNA -3.7%, COKE -3.5%, AMCR -3.3%, SNBR -3.2%, OPK -2.9%, CWEN -2.8% (also increases dividend), MKL -2.8%, FTAI -2.4%, MDXG -2.3%, RYN -2.2%, MET -2%of note.

What’s Happening This Morning: (as of 7:40 a.m. EDT)

Futures S&P 500 +53, NASDAQ +316, Dow Jones +252 , Russell 2000 +0.08. Europe is higher ex FTSE and Asia higher ex China. Bonds are at 4.14% from 4.168% yesterday on the 10-Year. Crude Oil and Brent Crude are lower with Natural Gas higher. Gold and Silver lower with Copper higher. The U.S. Dollar is lower versus the Euro, lower against the Pound and higher against the Yen. Bitcoin is at $96,034 from $94,923 higher by $2019 at +2.15%.

- Daily Positive Sectors: Healthcare, Consumer Defensive, Industrials and Real Estate of note.

- Daily Negative Sectors: Energy, Consumer Cyclical, Utilties and Financials of note.

- One Month Winners: Consumer Defensive of note.

- Three Month Winners: Consumer Defensive of note.

- Six Month Winners: Consumer Defensive and Financials of note.

- Twelve Month Winners: Utilities, Financials, Consumer Defensive, Real Estate, Communication Services, Consumer Cyclical and Technology of note.

- Year to Date Winners: Consumer Defensive, Utilities and Materials of note.

Bolded means the Sector is new to the period in which it falls.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Thursday After the Close:

- Friday Before The Open:

Notable Earnings of Note This Morning:

- Flat: LXP +0.00, FTV +0.00 of note

- Beats: ARVN +2.10, HII +0.87, MRNA +0.60, GVA +0.60, CVS +0.55, BPMC +0.50, MDGL +0.43, AGCO +0.37, EL +0.34, W +0.31, HOG +0.29, STNG +0.28, FTDR +0.26, TRP +0.25, PBF +0.21, CAH +0.18, DINO +0.16, APTV +0.16, AIT +0.16, HSY +0.15, BAX +0.14, BLDR +0.14, AAON +0.13, H +0.13, ATI +0.13, OGN +0.13, BIIB +0.12, BDC +0.11, IEX +0.11, PWR +0.11 of note.

- Misses:WD (0.53), APD (0.14), ALKS (0.12), WCC (0.11), SIRI (0.08), GPK (0.07), OCSL (0.06), TRN (0.03), XRX (0.03), SHAK (0.02), CCJ (0.02) of note.

- Still to Report: ALNY, APG, ARW, CWT, CFR, D, DNB, GWW, HGV, HUBB, NSIT, ICE, IDCC, ITRI, K, DRS, MA, MPW, NNN, OSIS, PH, PATK, PNW, RBLX, SNDR, SHC, THRY of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative or Mixed Guidance: None of note.

Advance/Decline Daily Update: The A/D crossed above its 30-day exponential moving average last week.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: ALGN +14.2%, NTGR +10.9%, TTMI +10.9%, TNDM +9.4%, MSFT +8.6%, WHD +8%, IRT +7.8%, GH +7.4%, RYI +6.9%, META +6.4%, MGM +5.9%, ALKT +5.8%, CWEN +5.6%, AAON +5.4%, OLO +4.8%, CNMD +4.7%, NVDA +4.3%, FOUR +4.2%, VTR +4.2%, BLKB +4%, WOLF +3.9%, ENVX +3.9%, ASH +3.9%, AMZN +3.8%, HOOD +3.7%, MCW +3.5%, RSI +3.5%, ACT +3.4%, EL +3.4%, MGY +3.3%, CSTL +3.2%, XPEV +2.9%, UDR +2.9%, BE +2.7%, ESEA +2.6%, TS +2.5%, MYRG +2.5%, WCC +2.5%, AXS +2.4%, EQIX +2.4%, WAY +2.4%, BVN +2.4%, CNXN +2.2%, MEOH +2.2%, CGNX +2.2%, AEIS +2.2%, KREF +2.1%, NIO +2%of note.

- Gap Down: DLX -10.9%, CFLT -10.7%, GKOS -9.8%, SNBR -9.5%, AGI -9.2%, TWI -7.8%, OTEX -5.9%, AU -5.7%, QCOM -5.4%, GRBK -5.4%, CTOS -5%, TPC -4.9%, PPC -4.9%, BHC -4.5%, SKT -4.5%, TFSL -4.2%, APD -4.1%, FTAI -3.9%, MKL -3.8%, GFL -3.8%, TSLX -3.5%, FOLD -3.3%, RDN -3.3%, CTGO -3.2%, ICLR -3%, HLF -2.9%, RGR -2.9%, SCI -2.6%, WEX -2.6%, TRGP-2.6%, CMPR -2.5%, AFL -2.5%, AX -2.5%, IVT -2.5%, LYG -2.5%, PSA -2.3%, MDXG -2.2%, TROX -2.2%, OCSL -2.2%, ANSS -2.1%, AIN -2% of note.

Insider Action: None of note sees Insider Buying with dumb short selling. None of note see Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Bloomberg: GM Lower Guidance on Tariffs Costs. Cost is up to $5 billion. (Bloomberg)

- Market Wrap:.. (Bloomberg)

- EU is planning to present new trade proposals to US this week. (Bloomberg)

- USTR Jamieson Greer in interview says he expects initial deals with various trading partners in weeks. (Reuters)

- Senate fails to pass resolution that would have revoked President Trump’s tariffs.

- Chinese state media says there would be “no harm” if trade talks started between U.S. and China. State media also claimed that US reached out to China. (FT)

- Eli Lilly (LLY) cuts guidance on research costs. (Bloomberg)

- 5 Things To Know Before The Market Opens. (CNBC)

- McDonald’s reports largest same store sales drop since 2020. (CNBC)

Bolded on story link means behind a Pay Wall.

Economic & Geopolitical:

- Economic Releases:

- Weekly Jobless Claims are due out at 8:30 a.m. EDT.

- Weekly Crude Oil Inventories are due out at 10:30 a.m. EDT.

- March Construction Spending is due out at 10:00 a.m. EDT and is expected to fall to 0.30% from 0.70%.

- April ISM Manufacturing Index is due out at 10:00 a.m. EDT as well and expected to fall to 47.90% from 49.0%.

- Weekly Jobless Claims are due out at 8:30 a.m. EDT.

- Federal Reserve Speakers of note today.

- Fed Speakers are back in Blackout period until next FOMC meeting is concluded.

- President Trump’s Daily Schedule.

- Press Briefing by the White House Press Secretary Karoline Leavitt and Deputy Chief of Staff Stephen Miller on Restoring Common Sense.

- President Trump participates in a National Day of Prayer Event at 10:00 a.m. EDT.

- President Trump receives his Intelligence Briefing at 11:00 a.m. EDT.

- President Trump participates in the swearing-in of the Ambassador to Italy at 2:00 p.m. EDT.

- President Trump delivers remarks at the University of Alabama Commencement at 8:00 p.m. EDT and then heads to Mar-A-Lago.

M&A Activity and News:

- None of note.

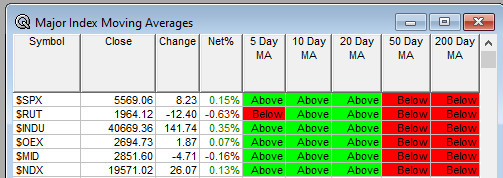

Moving Average Table: Moves from 60% to 57% on Equity Indexes.

Meeting & Conferences of Note:

- Sellside Conferences:

- RBC Capital Markets US Banks Fixed Income Investor Symposium

- Shareholder Meetings: BSX, DUK, EHC, EMN, GLW, KMB, PRGO

- Top Analyst, Investor Meetings: BERY, UIS

- Fireside Chat: None of note.

- R&D Day: None of note.

- FDA Presentation: None of note.

- Industry Meetings or Events:

- Advanced Clean Transportation Expo

- Ascend 2025

- RSA Conference

- TOKEN2049

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

- Upgrades: LANC NOW RVTY TRVG

- Downgrades: CTAS