Overnight Summary & Early Morning Trading:

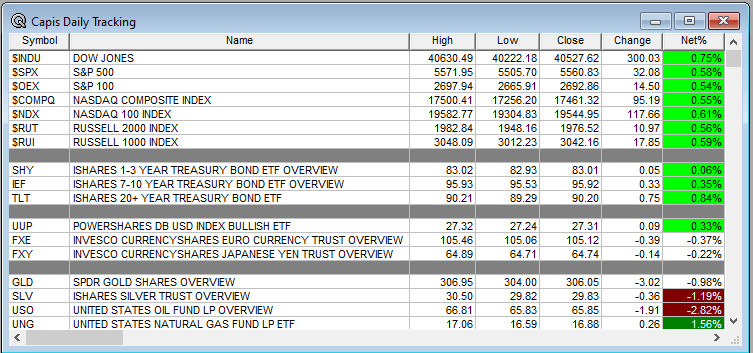

The S&P 500 finished Tuesday higher by 0.58% at 5560.83. Monday higher by 0.06% at 5528.75. Futures are lower this morning by -8 (-0.09%) at 5576 around 6:15 a.m. EDT. The range is now 600 points on the S&P 500 cash for the year, 5500 to 6100. Year to date the S&P 500 is down -5.45% from -6.00% Thursday’s close.

Executive Summary:

Stocks are beginning to trade with less volatility as the VIX is down to 23.50 this morning.

Quote of the Day:

- “At this time, cash is king”. Mark Mobius on cash in his funds which is at 95%.

Key Events of Note Today:

- Holy Cow!! 7 economic data points are due out on the last day of April. See Economic & Geopolitical Section below.

Notable Earnings Out After The Close:

- Beats: BKNG +7.47, NBR +5.10, HURN +0.52, QRVO +0.42, UMBF +0.39, LFUS +0.38, FICO +0.36, ACGL +0.22, EIX +0.16, STX +0.16, FLS +0.12, MDLZ +0.10, PPG +0.10 and V +0.08 of note. (Greater than $0.08)

- Misses: FSLR -0.54, CZR-0.34, WERN -0.24, UNM -0.15, SBUX -0.08, WPC -0.03 and LC -0.01 of note.

- Flat: None of note.

- IPOs For The Week: ALEH, EGG, OMSE, YB

- New IPOs/SPACs launched/News: None of note.

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced: None of note.

- Notes Priced: None of note.

- Notes Files: None of note.

- Convertibles Filed: None of note.

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Private Placements: None of note.

- Selling Shareholders of note:

- CCEC files for 15,142,440 share common stock offering by selling shareholders.

- Mixed Shelf Offerings:

- NRIM files for $150 million mixed securities shelf offering.

News After The Close:

- White House confirmed incentivizes for domestic automobile production.

- Canadian Prime Minister Mark Carney says that President Trump agreed to meet him in person in the near future.

- Super Micro Computer (SMCI) lowers Q3 EPS and revenue guidance below consensus.

- Blackstone (BX) ticking higher on report it’s exploring $3 billion sale of Sphera. (Reuters)

- Starbucks (SBUX) on earnings call: declines to provide Q3 (Jun) guidance but says it expects Q3 to follow normal seasonality.

- 10K or Qs Filings/Delays – (Filed), (Delayed) None of note.

Exchange/Listing/Company Reorg and Personnel News:

- CSL elected James D. Frias as Lead Independent Director succeeding Robin J. Adams, who previously held the position.

- ACEL announces that Mathew Ellis, Chief Financial Officer, has resigned, effective May 9, 2025, to pursue other business interests.

- OUST appointed Kenneth P. Gianella as Chief Financial Officer effective May 19, 2025.

Buybacks:

- V increases buyback by $30 billion.

Dividends Announcements or News:

- Stocks Ex Div Today: AON O NRG CASY PAGP PAA ALLY ATR AES AVAL VSEC WSR

- Stocks Ex Div Thursday of note:

Stocks Moving Up & Down Yesterday:

- Gap Up: ODD +20.9%, ORN +17.7%, JAKK +15.1%, RCKY +9.8%, FRSH +11.3%, QRVO +9%, STX +9%, LFUS +8.7%, ETWO +8.6%, BBIO +7.3%, TTI +6.9%, OI +6.6%, FLS +6.5%, NOG +6.3%, CLW +5.7%, NBR +5.2%, SIMO +4.1%, LRN +3.7%, TX +3%, ROG +2.9%, QUAD +2.9%, CWH +2.3%, MIR +2.2% of note.

- Gap Down: TENB -17.8%, SMCI -15.6%, SNAP -14.1%, HRZN -10%, VICR -9.5%, FSLR -9.1%, RBBN -8.8%, UNM -7.9%, HI -6.1%, SBUX -6.1%, WERN -4.9%, KAI -4.8%, FIBK -4.7%, BKNG -3%, FICO -2.9%, FYBR -2.8%, OKE -2.6% of note.

What’s Happening This Morning: (as of 7:40 a.m. EDT)

Futures S&P 500 -14, NASDAQ -94, Dow Jones +49, Russell 2000 -5.62. Europe is higher and Asia higher ex China. Bonds are at 4.168% from 4.235% yesterday on the 10-Year. Crude Oil and Brent Crude are lower with Natural Gas lower. Gold, Silver and Copper lower. The U.S. Dollar is higher versus the Euro, higher against the Pound and higher against the Yen. Bitcoin is at $94,923 from $95,146 lower by $426 at -0.45%.

- Daily Positive Sectors: Financials, Consumer Defensive, Healthcare and Utilities of note.

- Daily Negative Sectors: Energy of note.

- One Month Winners: Consumer Defensive of note.

- Three Month Winners: Consumer Defensive of note.

- Six Month Winners: Consumer Defensive and Financials of note.

- Twelve Month Winners: Utilities, Financials, Consumer Defensive, Real Estate, Communication Services, Consumer Cyclical and Technology of note.

- Year to Date Winners: Consumer Defensive, Utilities and Materials of note.

Bolded means the Sector is new to the period in which it falls.

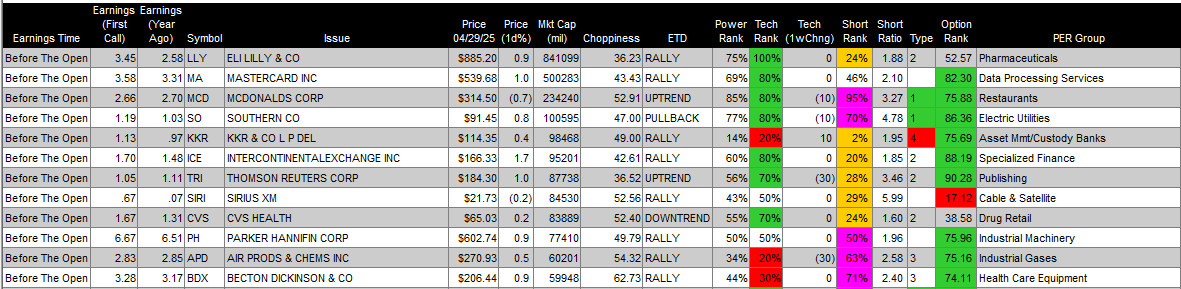

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Wednesday After the Close:

- Thursday Before The Open:

Notable Earnings of Note This Morning:

- Flat: REYN +0.00, BIP +0.00, TW +0.00, GIB +0.00 of note

- Beats: EVR +1.95, HUM +1.51, AER +0.93, EME +0.78, DFIN +0.54, PAG +0.38, GNRC +0.30, TT +0.25, VMC +0.23, WGS +0.21, IONS +0.17, CSTM +0.16, ROCK +0.14, COCO +0.11, of note. (Greater than $+0.10)

- Misses: ETSY (0.96), GSK (0.62), WNC (0.30), SITE (0.16), IP (0.15), PSN (0.14), OSK (0.13), SLGN (0.10), CAT (0.10), LANC (0.09), BLCO (0.09), LECO (0.09), UTHR (0.07), SR (0.07), OSW (0.06), GRMN (0.06), FDP (0.05), DAN (0.04), XPRO (0.02), YUMC (0.02), DTM (0.02), TKR (0.02), NCLH (0.02), PEG (0.01) of note.

- Still to Report: NMRK, SMP, HESM, AVT, FSS, WING, WDC, HES, ITW of note.

Company Earnings Guidance:

- Positive Guidance: DEA of note.

- Negative or Mixed Guidance: HLIT PII SANM SPOT UCTT of note.

Advance/Decline Daily Update: The A/D crossed above its 30-day exponential moving average last week.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: ODD +18.8%, JAKK +15%, ORN +14.5%, WSBC +13.6%, FFAI +13.5%, QRVO +11%, CWAN +10.8%, FRSH +10.7%, RCKY +10.3%, BBIO +9.6%, SVCO +9%, TTI +8.3%, STX +7.8%, ABVX +7.3%, MTAL +6.9%, PBYI +6.6%, CWH +6.5%, SNN +5.6%, QUAD +5.4%, HUM +5.1%, NOG +4.9%, HIW +4.9%, TX +4.8%, ETWO +4.8%, CLW +4.7%, CSTM +4.3%, LRN +4.2%, OI +4.2%, PPG +4%, ASX +3.4%, FLS +3.3%, LFUS +3.1%, EXLS +3%, GSK +2.8%, MIR +2.4% of note.

- Gap Down: TENB -18.6%, SMCI -15.4%, SNAP -13.9%, FSLR -13.1%, HRZN -11.6%, RBBN -7.7%, MRTN -7.5%, VICR -7.5%, JBGS -7.2%, SBUX -6.9%, LC -6.7%, UNM -6%, SAN -5.7%, MT -5.6%, WERN -4.8%, SON -3.7%, FIBK -3.6%, BKNG -3.6%, BXP -3.5%, KAI -3%, PUK -2.9%, IP-2.6%, XNCR-2.5%, EQR-2.5%, CHX-2.5%, MESO -2.5%, OKE -2.4%, NVCT -2.1%, FYBR -2.1%, YUMC -2.1%, EXPE -2%, KRG -2%, BCS -2%of note.

Insider Action: FLWS of note sees Insider Buying with dumb short selling. None of note see Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Bloomberg: Trump Bashes Powell and Touts Tariffs At Michigan Rally. (Bloomberg)

- Market Wrap:.Stock futures slip in buildup to big tech earnings. (Bloomberg)

- Ukraine ready to sign US Resources deal as early as today. (Bloomberg)

- Yum Brands (YUM) misses on Pizza Hut revenues. (CNBC)

- MBA Mortgage Applications fell -4.2% this morning in the weekly update.

- Sell in May? (CNBC)

- Bloomberg Odd Lots: Understanding the April Bond Yield Spike. (Podcast)

Bolded on story link means behind a Pay Wall.

Economic & Geopolitical:

- Economic Releases:

- April ADP Jobs Report is due out at 8:15 a.m. EDT and is expected to rise to 128,000 from 77,000.

- Q1 GDP (Advanced) is due out at 8:30 a.m. EDT and are expected to fall to 0.4% from 2.4%.

- March Personal Income is due out at the same time and expected to fall to 0.4% from 0.8%.

- March PCE Core is out at 8:30 a.m. EDT and expected to fall to 0.1% from 0.4%.

- Chicago PMI is out at 9:45 a.m. EDT and expected to fall to 46 from 47.60.

- March Pending Home Sales are due out at 10:00 a.m. EDT and are expected to fall to -0.20% from 2.0%.

- Weekly Crude Oil Inventories are due out at 10:30 a.m. EDT.

- Federal Reserve Speakers of note today.

- Fed Speakers are back in Blackout period until next FOMC meeting is concluded.

- President Trump’s Daily Schedule.

- President Trump heads a Cabinet Meeting at 11:00 a.m. EDT.

- President Trump participates in the swearing in of the Ambassador to the United Kingdom at 2:00 p.m. EDT.

- President Trump delivers remarks to Investing in America at 4:00 p.m. EDT.

- President Trump participates in a NewsNation Cuomo Townhall: The First 100 Days at 8:00 p.m. EDT.

M&A Activity and News:

- None of note.

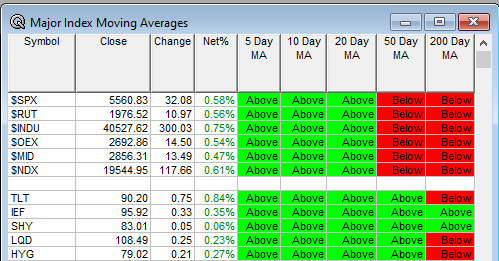

Moving Average Table: Remains at 60% on Equity Indexes. TLT improved more on Monday.

Meeting & Conferences of Note:

- Sellside Conferences:

- Morgan Stanley Brazil Healthcare Day

- Shareholder Meetings: DJT, HUN, KO, MOH, MPC, NEM, NYT, PHM, WYNN

- Top Analyst, Investor Meetings: CAT, JAGX, STLA, V

- Fireside Chat: None of note.

- R&D Day: None of note.

- FDA Presentation:

- ABEO: PDUFA Date for Pz-cel EB-101 (COL7A1)

- ACTU: Data Presentation on Elraglusib

- VCNX: Data Presentation for Pepinemab

- Industry Meetings or Events:

- AACR Annual Meeting

- GLP-1-Based Therapeutics Summit

- Innovation Zero World Congress

- NI Connec

- RSA Conference

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

- Upgrades: C

- Downgrades: L