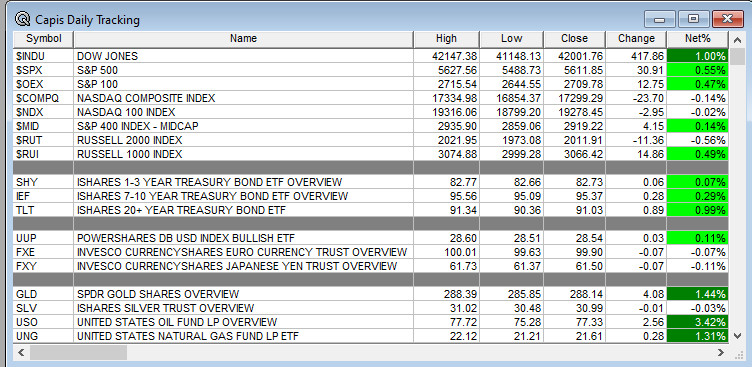

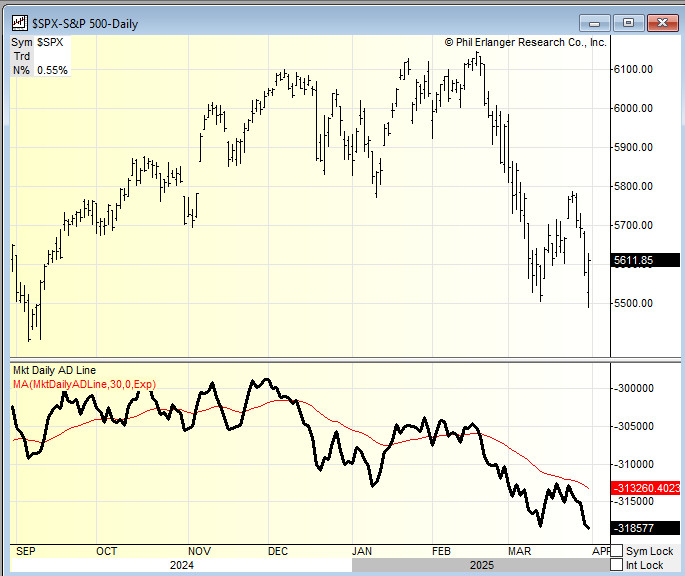

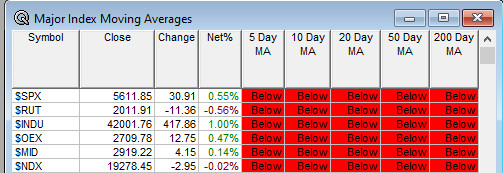

Overnight Summary & Early Morning Trading: The S&P 500 finished Monday higher by 0.55% at 5611.85. Friday lower by -1.97% at 5580.94. Futures are lower this morning by -21 (-0.37%) at 5633.50 around 6:50 a.m. EDT. The range is 500 points on the S&P 500 for the year, 5600 to 6100 a drop of 100 points. Thought for the upcoming week: Moving above 5600 on the cash is a big deal after moving above this level yesterday. Can it hold today?

Key Events of Note Today:

- Several economic data points due out see Economic section.

Notable Earnings Out After The Close

- Beats: PRGS +0.25, PVH +0.06 of note.

- Misses: LPRO -1.23 of note.

- IPOs For The Week: CRWV, FATN, LGPS, OMSE

- New IPOs/SPACs launched/News:

- IPOs Filed/Priced:

- Secondaries Filed or Priced:

- EE announces proposed public offering of $150 mln of Class A common stock.

- Notes Priced:

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Private Placements:

- Selling Shareholders of note:

- CWAN files common stock offering; also files for 3,833,333 shares of common stock offering by selling shareholder.

- Mixed Shelf Offerings:

- PRGS files mixed shelf securities offering.

- XRAY files mixed shelf securities offering.

- Convertible Offerings:

News After The Close:

- Fluor (FLR) will recognize the $671 million bid-build contract in the first quarter of 2025.

- Hillenbrand (HI) completes the Sale of Majority Stake in Milacron injection molding and extrusion business for $287 mln.

- CACI Intl (CACI) and the United States Military Academy enter cooperative research and development agreement to advance electronic warfare technologies. We note the United States Naval Academy is way ahead on this effort with its Cyber Warfare Hooper Center.

- Red Cat Holdings (RCAT) Reports Financial Results for the 2024 Transition Period (as of December 31, 2024 and the eight months then ended) and Provides Corporate Update.

- Estee Lauder (EL) to face a lawsuit over concealing overdependence on gray-market sales in China. (Reuters)

- Hyundai Motor (HYMTF) warns U.S. dealers it will evaluate pricing strategy, potentially hiking prices come 25% tariffs on imported vehicles and parts. (Reuters)

- Live Nation (LYV) and Vivid Seats (SEAT) ticking lower after President Trump plans to sign Executive Order targeting ticket scalping. (Reuters)

- Valaris (VAL) awarded two-year contract offshore West Africa for drillship VALARIS DS-10 valued at $352 mln.

- Freeport McMoran (FCX) realized Q1 prices for copper reflect higher prices on US sales.

- BA awarded $2.46 bln U.S. Air Force contract modification.

- LMT awarded $600 mln U.S. Air Force contract modification

- 10K or Qs Filings/Delays – (Filed), TSSI DBVT WINT (Delayed) of note.

Exchange/Listing/Company Reorg and Personnel News:

- JACK named Lance Tucker as its CEO; he had served as interim CEO since February 2025.

- LPRO appointed Board Chair Jessica Buss as CEO, effective immediately; Michelle Glasl named COO

- TKR CEO Tarak B. Mehta departing, effective immediately; Richard G. Kyle appointed interim president and CEO

- ARDT appoints Dave Caspers as COO

- BIGC CTO Brian Dhatt to depart, effective April 30; Marcus Groff, Senior Vice President of Engineering, will assume Mr. Dhatt’s engineering related duties and responsibilities

Buybacks

- PVH intends to enter into $500 million accelerated share repurchase agreements.

Dividends Announcements or News:

- Stocks Ex Div Today: APD O A CAH RJF STT EHC CUBE INGR FRT NYT CHH PEGA SFBS TNET FULT ANDE WWW.

- Stocks Ex Div Tomorrow: CMCSA RSG BBDO BBD ACM BRX ESE CVBF UPBD

Stocks Moving After The Close:

Gap Up: MVST +34.2%, PVH +15.8%, JACK +2.8% of note.

Gap Down: LPRO -12.3%, EE -6.5%, CELC -5.5%, VATE -5%, DBVT -2.5%, CWAN -2%

What’s Happening This Morning: (as of 8:25 a.m. EDT) Futures S&P 500 -22, NASDAQ -66, Dow Jones -219, Russell 2000 -4.80. Europe and Asia are higher ex China. Bonds are at 4.157% from 4.19% yesterday on the 10-Year. Crude Oil and Brent Crude are lower with Natural Gas lower as well. Gold, Silver and Copper higher. The U.S. Dollar is higher versus the Euro, higher against the Pound and lower against the Yen. Bitcoin is at $83,976 from $82,035 higher by $1190 at 1.435%.

- Daily Positive Sectors: Consumer Defensive, Utilities, Financials, Energy and Real Estate.

- Daily Negative Sectors: Consumer Cyclical and Technology led the way lower.

- One Month Winners: Energy and Utilities of note.

- Three Month Winners: Energy, Materials, Healthcare, Utilities and Financials of note.

- Six Month Winners: Financials, Energy, Consumer Defensive, Communication Services and Utilities of note.

- Twelve Month Winners: Utilities, Financials, Communication Services, Consumer Defensive, Real Estate and Technology of note.

- Year to Date Winners: Energy, Materials, Healthcare, Utilities, Financials, Consumer Defensive and Real Estate of note.

Bolded means the Sector is new to the period in which it falls.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Tuesday After the Close: NCNO

- Wednesday Before The Open: ANGO UNF

Notable Earnings of Note This Morning:

- Flat: None of note

- Beats: None of note.

- Misses: None of note.

- Still to Report:

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative or Mixed Guidance: PRGS PVH of note.

Advance/Decline Daily Update: The A/D continues to struggle and did not improve yesterday.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: MVST +26.5%, PVH +17.3%, PRGS +7.9%, TSSI +6.2%, WINT +4.8%, HI +4.7%, CELC +4.4%, XPEV +4%, CWAN +3.7%, XRAY +3.7%, BIGC +3.5%, NIO +2.6%, BMA +2% of note.

- Gap Down: LPRO -12.3%, EE -7.5%, TVTX -2.8%, DBVT -2.3%, DHC -2.1%, KLIC -2% of note.

Insider Action: No names see Insider Buying with dumb short selling. No names see Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Bloomberg: Trump Tariffs Set to Make History And Break A System MAGA Loathes. (Bloomberg)

- Market Wrap: US Futures drop as tariffs weigh on markets. (Bloomberg)

- Stocks Making The Biggest Moves: PVH JNJ NMAX SHAK. (CNBC)

- US Chip Grants in Limbo. (Bloomberg)

- White House to consider roughly 20% tariffs. (CNBC)

- Open AI closes $40 billion funding. (CNBC)

- 5 Things To Know Before The Market Opens. (CNBC)

- Bloomberg: Odd Lots – The growing risk to Fed independence. (Podcast)

Bolded Royal Blue means behind a Pay Wall.

Economic & Geopolitical:

- Economic Releases:

- March S&P Global US Manufacturing PMI came in at 49.80 in its last update.

- March ISM Manufacturing is due out at 10:00 a.m. EDT and is expected to fall to 49.8% from 50.3%.

- Last, February Construction Spending is due out at 10:00 a.m. EDT as well and is expected to rise to 0.40% from -0.20%.

- Weekly API Petroleum Institute is out with its latest inventory update at 4:30 p.m. EDT.

- Federal Reserve Speakers of note today.

- Federal Reserve Atlanta President Raphael Bostic speaks at 9:00 a.m. EDT.

- President Trump’s Daily Schedule.

- Press Briefing at 12:00 p.m. EDT.

- The president and vice president have lunch at 12:30 p.m. EDT.

- President Trump signs Executive Orders at 3:30 p.m. EDT.

M&A Activity and News:

Moving Average Table: Moves from 20% to 0% today.

Meeting & Conferences of Note: (Not updated today, back tomorrow)

-

- Sellside Conferences:

- Bank of America Nuclear Conference

- Citi Clinic at the Cleveland Clinic Conference

- Goldman Sachs Private Company Software and Internet Conference

- JP Morgan Napa Valley Biotech Forum

- JP Morgan Retail Round Up

- Piper Cardio Day with ACC Takeaways

- Sellside Conferences:

-

- Shareholder Meetings: CIGI, DGLY, RNXT, RSLS

- Top Analyst, Investor Meetings: MLYS, NXDT, SRAD

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation:

- Industry Meetings or Events:

- AD/PD 2025 Alzheimer’s & Parkinson’s Diseases Conference

- CinemaCon

- Intel Vision

- Int Conference on Alzheimer’s and Parkinson’s Diseases

- ISC West

- Optical Fiber Communications Conference and Exhibition

- Van Lanschot Kempen European Real Estate Seminar

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

-

- Upgrades: HMST ESAB

- Downgrades: MSTR

-

-