Quote of the Day: With less progress on inflation and businesses expected to add the cost of coming tariffs to their prices, “the appropriate path for policy is also going to be pushed back,” Federal Reserve Atlanta President Bostic said in an interview on Bloomberg today. That means only 1 cut now according to Bostic.

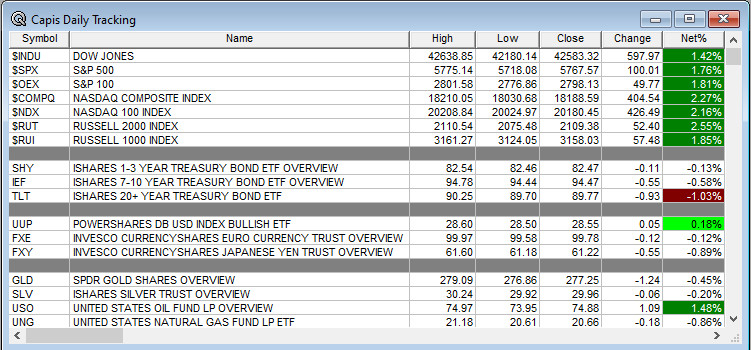

Overnight Summary & Early Morning Trading: The S&P 500 finished Monday higher by 5767.57 by 1.76%. Friday higher by 0.08% at 5667.56. Futures are higher this morning by 13.25 (+1.09%) at 5828.75 around 8:05 a.m. EDT. The range is 400 points on the S&P 500 for the year, 5700 to 6100, but could move to 300 points. Thought for the week: Moving above 5700 on the cash is a big deal after recapturing 5700 yesterday.

Chart of the Day: The Home Builders look ugly and KB Homes (KBH) is no exception after missing estimates by $0.07 this morning. The stock is now at $57.80 in the pre-market.

Key Events of Note Today:

- Consumer Confidence and New Home Sales are due out at 10:00 a.m. EDT.

- A 2-Year Note Auction is held at 1:00 p.m. EDT.

Notable Earnings Out After The Close

- Beats: None of note.

- Misses: OKLO -0.67, KBH -0.08 of note.

- IPOs For The Week: CRWV, FATN, LGPS, OMSE

- New IPOs/SPACs launched/News:

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced:

- PROP announces public offering of common stock of $35 mln

- AEP announces public offering of $2 bln of common stock with a forward component

- RCT Closing of $20 Million Initial Public Offering

- SUUN Closing of up to US$19 Million Equity Financing

- Notes Priced:

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Private Placements.

- Selling Shareholders of note:

- Mixed Shelf Offerings:

- NGNE files $300 mln mixed shelf securities offering.

- TLSA files $250 mln mixed shelf securities offering.

- CLNN: FORM S-3 – $160,000,000 Mixed Shelf Offering

Biggest Movers Up & Down Yesterday

- Movers Up: DJT +4.6%, SPIR +2.5%, FFAI +2.2% of note.

- Movers Down: PROP -19.6%, UNF -9.2%, KBH -7.7%, MRT -4.5%, OKLO -4% of note.

News After The Close:

- Cintas (CTAS) terminates discussions with UniFirst (UNF) regarding its previously announced proposal to acquire the UNF for $275.00/share.

- KB Home (KBH) says that the spring selling season was more muted than typical, misses on earnings.

- Black Hills (BKH) announces that its electric utility subsidiary in Colorado received approval from the Colorado Public Utilities Commission for new rates.

- Boeing (BA) looks to withdraw guilty plea agreement reached during final months of the Biden administration. (WSJ)

- Trump Media (DJT) announces Intention to Partner with Crypto.com to Launch ETFs.

- eToro Group files for NASDAQ IPO under the ticker “ETOR”. (SEC Filing)

- 10K or Qs Filings/Delays – (Filed), (Delayed) of note.

Exchange/Listing/Company Reorg and Personnel News:

- OKLO has appointed Daniel Poneman and Michael Thompson to its Board of Directors.

- SPIR appoints Alison Engel as its new CFO, effective April 1.

- OMCL names Perry Genova, PhD as new CTO, effective March 31

- KBH appoints Robert Dillard as CFO, effective March 31

- CCI terminates Steven Moskowitz as CEO, CFO named as interim CEO; Reaffirms all recently announced financial guidance and capital allocation policies.

- EG announces that Joseph Taranto, current Board Chair, will retire from that role when his term expires in May.

Buybacks

- PSN increases the company’s stock repurchase authorization to $250 million

Dividends Announcements or News:

- Stocks Ex Div Today: TTE MO E STM BBY VIV ADO

- Stocks Ex Div Tomorrow: ERIC INVH CW TRNO MTN KFY PSEC GTY OLP

What’s Happening This Morning: (as of 8:05 a.m. EDT) Futures S&P 500 +12, NASDAQ +34, Dow Jones +54, Russell 2000 -3.58. Europe is higher with Asia higher as well. Bonds are at 4.36% from 4.296% yesterday on the 10-Year. Crude Oil and Brent Crude are higher with Natural Gas higher. Gold, Silver and Copper higher. The U.S. Dollar is lower versus the Euro, lower against the Pound and lower against the Yen. Bitcoin is at $87,351 from $87,496 lower by $-875 at -1.01%.

- Daily Positive Sectors: All higher. led by Consumer Cyclical, Industrial, Technology, Communication Services and Financials.

- Daily Negative Sectors: No losers.

- One Month Winners: Healthcare and Energy of note.

- Three Month Winners: Healthcare, Energy and Utilities of note.

- Six Month Winners: Utilities, Financials, Communication Services and Consumer Cyclicals of note.

- Twelve Month Winners: Utilities, Financials, Communication Services, Consumer Defensive and Technology of note.

- Year to Date Winners: Materials, Financials, Healthcare, Consumer Defensive, and Real Estate of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Tuesday After the Close:

- Wednesday Before The Open:

Notable Earnings of Note This Morning:

- Flat: None of note

- Beats: CSIQ +0.59 of note.

- Misses: CNM -0.04, MKC -0.04 of note.

- Still to Report: CRMD of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative or Mixed Guidance: CSIQ KBH of note.

Advance/Decline Daily Update: The A/D fell to major support making new lows.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: FFAI +18.8%, ALMS +13.4%, MBLY +10.1%, PSIX +9.8%, DJT +9.4%, SFD +3.6% of note.

- Gap Down: MURA -27.7%, PROP -22%, UNF -10.2%, KBH -8%, OKLO -6.7%, PONY -4.5%, MKC -4.2%, EPAC -3%, MRT -2.5%, OMCL -2.3% of note.

Insider Action: None of note see Insider Buying with dumb short selling. None of Note sees Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Bloomberg: Trump’s Threats of Secondary Tariffs Invents New Trade Weapon. (Bloomberg)

- Market Wrap: Stocks stall on new Trump trade salvo. (Bloomberg)

- Stocks Making The Biggest Moves: CVNA KBH NET AEP. (CNBC)

- Treasury Secretary Scott Bessent meets with Republican leaders on tax bill today. (Politico)

- February European Tesla (TSLA) sales fell 40% yr/yr.

- 5 Things To Know Before The Market Opens. (CNBC)

- Bloomberg The Big Take – Trumps CEA Head talks tariffs. (Podcast)

Bolded Royal Blue means behind a Pay Wall.

Economic & Geopolitical:

- March Consumer Confidence is due out at 10:00 a.m. EDT and is expected to fall to 94.20 from 98.30.

- February New Home Sales are due out at the same time and expected to rise to 680,000 from 657,000.

- Weekly API Inventory Levels due out at 4:30 p.m. EDT.

- President Trump’s Daily Schedule.

- President Trump and the vice president have lunch at 12:30 p.m. EDT.

- President Trump signs Executive Orders at 2:00 p.m. EDT.

- Federal Reserve Speakers of note.

- Federal Reserve Governor Adriana Kulger at 8:40 a.m. EDT.

- Federal Reserve New York President John Williams speaks at 9:05 a.m. EDT.

M&A Activity and News:

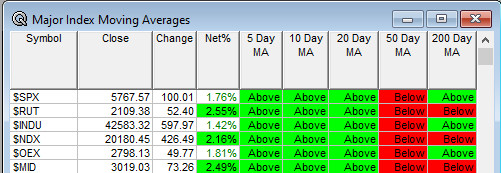

Moving Average Table: Move from 23% to 71% today.

Meeting & Conferences of Note: (Not updated today, back tomorrow)

-

- Sellside Conferences:

- BMO Obesity Summit

- BNP Paribas Exane European Healthcare Conference

- HSBC Global Investment Summit

- iAccess Alpha Virtual Best Ideas Spring Conference

- Immuno-Oncology 360 Conference

- ISG Xperience Summit

- JP Morgan Public Finance Transportation & Utility Investor Forum

- Kepler Aerospace & Defense Conference

- Leerink Partners Foundations of Discovery, Drugs & Dx

- Leerink Mountain Meeting

- TD Securities Industrials & Infrastructure Services Conf

- Sellside Conferences:

-

- Shareholder Meetings: TRVI, WIMI

- Top Analyst, Investor Meetings: ACRV, ATNM, CTSH, HURN, IP, KALV, KFS, PAVM

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation:

- Industry Meetings or Events:

- Agentic AI Summit

- Compound Semiconductor Asia Conference

- NABCEP CE

- National Bank of Canada’s Financial Services Conference

- STN East Conference

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

- Upgrades: HQY NET CRWD COF ALC

- Downgrades: OPT ALLY

-