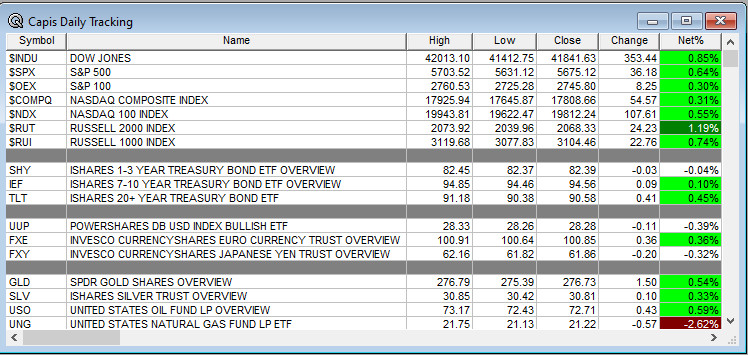

Overnight Summary & Early Morning Trading: The S&P 500 finished Monday higher by 0.64% at 5675.12. Friday was higher by 2.13% at 5639.94. A two day rally impressive! Futures are lower this morning by -14 (-0.24%) on the S&P 500 at 7:00 a.m. EDT. Current level is 5718.25 on the Futures of the S&P 500.

Executive Summary: Back and forth we go. The S&P 500 is back above 5600. The range is 500 from 600 points on the S&P 500 for the year, 5600 to 6100. Futures are lower this morning and 5600 is now support. Moving above 5700 would be a big deal after recapturing 5600. We are only 25 points away from this level.

Breaking:

Chart of the Day: Steel Dynamics (STLD) guided lower after the close and has very few shorts, 10%, with a poor tech rank. It should move to a Type 4 Long Squeeze.

Key Events of Note Today:

- Several monthly economic data points due out. (see Economic section)

- 52 Week Bill Auction at 11:30 a.m. EDT.

- 20-Year Bond Auction at 1:00 p.m. EDT.

Notable Earnings Out After The Close

- Beats: GETY +0.01 of note.

- Misses: None of note.

- IPOs For The Week: APUS, FATN, KMTS. OMGE, SAGT,

WGRX - New IPOs/SPACs launched/News:

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced:

- ETR public offering of common stock with a forward component

- VCIG: Form 424B5.. 5,100,000 Ordinary Shares

- Notes Priced:

- AA Announces Closing of Debt Offering

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Private Placements.

- QXO Raises $830 Million in Private Placement

- Selling Shareholders of note:

- Mixed Shelf Offerings:

- VRPX: FORM S-1 – Mixed Shelf Offering

- Convertible Offerings & Notes Filed:

Biggest Movers Up & Down Last Week: Well none posted as last week was too volatile for an update. If that does not mark the bottom, then I do not know what does.

- Movers Up: HROW +16.9%, KODK +12.2%, NBTX +6.2%, SOC +6.1%, TTEC +3.4%, VERI +3.2%, MRP +2.2% of note.

- Movers Down: BKKT -29.1%, HNRG -11.1%, QXO -4%, ELAN -3.6%, ETR -3.5%, SGMO -3% of note.

News After The Close:

- Alphabet (GOOGL) in advanced talks to purchase Wiz, a cybersecurity startup, for around $30 bln. (WSJ)

- Bank of America (BAC) and Webull Pay both not renewing commercial agreement with Bakkt (BKKT).

- Steel Dynamics (STLD) guides Q1 EPS below consensus.

- LMT awarded $213 mln U.S. Army contract modification.

- 10K or Qs Filings/Delays – (Filed), BKKT VERI INSE MSBI FRST DDD HROW BLNK (Delayed) of note.

Exchange/Listing/Company Reorg and Personnel News:

- BBIO appoints Thomas Trimarchi as President and CFO.

- EXPI names Jesse Hill as interim CFO, effective April 1.

- OSW announces CFO and COO Stephen Lazarus appointed President; Chief Commercial Officer Susan Bonner to step down.

- CPAY appoints Alissa Vickery to serve as interim CFO, effective immediately.

Buybacks:

- MBC authorizes share repurchase program for up to $50 mln of common stock.

Dividends Announcements or News:

- Stocks Ex Div Today: TSM PLD APH ECL ROST VRT PHM HBAN TXRH FTI CCK AAON BPOP AL AVNT CON KRP JJSF HUBG PLOW BWMX UNTC CHMG CZNL PRG.

- Stocks Ex Div Tomorrow: NXPI STX BSY FSK CSGS ELME QCRH.

- SCVL approves 11.1% increase in quarterly cash dividend to $0.15/share

- MRP announces first dividend at $0.38.

What’s Happening This Morning: (as of 8:15 a.m. EDT) Futures S&P 500 -16, NASDAQ -93, Dow Jones -88, Russell 2000 -11.40. Europe is higher with Asia higher as well. Bonds are at 4.306% from 4.281% yesterday on the 10-Year. Crude Oil and Brent Crude are higher with Natural Gas lower. Gold, Silver and Copper higher. The U.S. Dollar is lower versus the Euro, higher against the Pound and higher against the Yen. Bitcoin is at $82,700 from $83,211 lower by $1816 at -2.14%.

- Daily Positive Sectors: All were higher for a second day. Wow!! An infrequent observation to say the least.

- Daily Negative Sectors: None were lower.

- One Month Winners: Real Estate, Consumer Defensive, Utilities and Healthcare of note.

- Three Month Winners: Communication Services, Consumer Defensive, Financials and Healthcare of note.

- Six Month Winners: Communication Services, Financials, Consumer Cyclical and Utilities of note.

- Twelve Month Winners: Financials, Utilities, Communication Services, Technology and Consumer Defensive of note.

- Year to Date Winners: Financials, Healthcare, Consumer Defensive, Materials and Real Estate of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Tuesday After the Close: ZTO of note.

- Wednesday Before The Open:

Notable Earnings of Note This Morning:

- Flat: None of note

- Beats: TME+0.25 of note.

- Misses: BEKE -0.66, HUYA -0.32 of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative or Mixed Guidance: None of note.

Advance/Decline Daily Update: The A/D fell to major support making new lows, before a rebound the last two days.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: HROW +21.9%, FINV +12.7%, INSE +10%, KODK +5.4%, NBTX +4.8%, ESLT +4.5%, MBC +3.4%, TBRG +3.2%, TIGR +2.8%, TTEC +2.6%, ZYXI +2.4%, OSW +2.3%, VNET +2.3%, CMPS +2.3%, TME +2.2%, ERJ +2.1%, STAA +2.1%, SOC +2.1% of note.

- Gap Down: BKKT -29.5%, HUYA -10.6%, BEKE -6.9%, BBAI -6.6%, HNRG -6.5%, SGMO -4.9%, VERI -3.2%, MRP -3.1% of note.

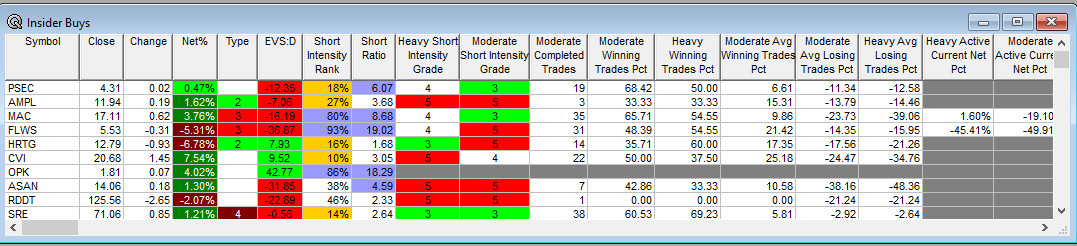

Insider Action: MAC FLWS see Insider Buying with dumb short selling. None see Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Market Wrap: US Stocks to Resume Slide as Growth Concern Weigh. (Bloomberg)

- Bloomberg: JP Morgan Stock Traders Reel in Windfall as Trump Whipsaws Market. (Bloomberg)

- Stocks Making The Biggest Moves: RL BIDU DUOL (CNBC)

- Israel launches large-scale attack on Gaza. (NYT)

- Corportate Insiders are buying the dip on their stocks. (Bloomberg)

- Frontier Airlines (ULCC) to offer free checked bags through August. (CNBC)

- Russian President Putin will demand suspension of all weapons deliveries to Ukraine in exchange for ceasefire during today’s call with President Trump. (Bloomberg)

- President Trump says Chinese President Xi will come to visit him in the near future. (Bloomberg)

- President Trump will speak with Russian President Putin tomorrow to discuss ending Ukraine war.

- President Trump’s advisors are considering a simplified structure for reciprocal tariffs on April 2. (WSJ)

- Apple (AAPL) lost appeal in German antitrust case. (Reuters)

- 5 Things To Know Before The Market Opens Tuesday. (CNBC)

- Bloomberg The Big Take – How Wall Street thinks about Crypto’s future. (Podcast)

Bolded Royal Blue means behind a Pay Wall.

Economic:

- February Housing Starts are due out at 8:30 a.m. EDT and are expected to grow 1,385,000 from 1,366,000.

- February Industrial Production is due out at 9:15 a.m. EDT and expected to fall to 0.2 from 0.5.

- Weekly API Petroleum is due out at 4:30 p.m. EDT.

- President Trump’s Daily Schedule.

- President Trump signs Executive Orders starting at 3:00 p.m. EDT.

- At some point, President Trump holds a telephone call with Russian President Putin.

- Federal Reserve Speakers are in blackout now until March 20th when the latest meeting has concluded.

M&A Activity and News:

- .

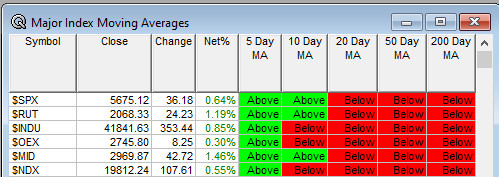

Moving Average Table: Move from 20% to 30% today.

Meeting & Conferences of Note: (Not updated today, back tomorrow)

-

- Sellside Conferences:

- Bank of America Electronic Payments Symposium

- Bank of America Global Industrials Conference

- KeyBanc Healthcare Forum

- Morgan Stanley European Financials Conference

- Oppenheimer Healthcare Conference

- Piper Sandler Energy Conference

- Piper Sandler Tech Leadership Ski Summit

- Roth Conference

- Stifel CNS Forum

- TD Cowen Life Sciences Winter Meeting & Ski Trip

- William Blair Industrials Summit

- Wolfe Autos Summit

- World Petrochemical Conference

- Sellside Conferences:

-

- Shareholder Meetings: DTIL, QCOM, VRPX

- Top Analyst, Investor Meetings: ADBE, AFRM, BOX, ETON, GLW, MOS

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation:

- Industry Meetings or Events:

- Adobe Summit

- Coldwell Banker Commercial Global Conference

- LSI USA ’25 Conference

- MDA Clinical and Scientific Conference

- NVIDIA GTC AI Conference

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

- Upgrades: WTW RL GDS PCAR

- Downgrades: TPIC

-