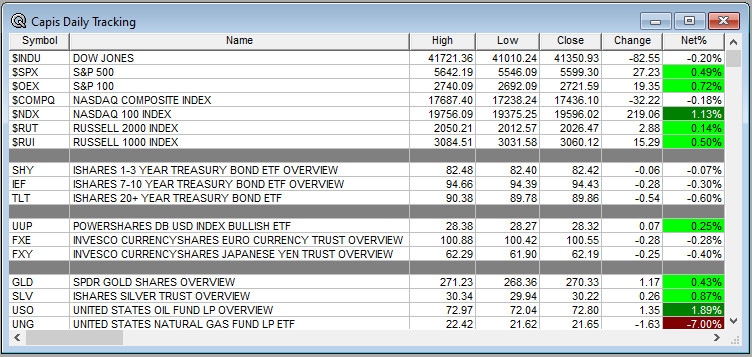

Overnight Summary & Early Morning Trading: The S&P 500 finished Wednesday higher by 0.49% at 5599.30. Tuesday lower by -0.76% at 5572.07. It was the worst trading day of the year on Monday. Futures are lower this morning by -7.50 (-0.13%) on the S&P 500 at 7:10 a.m. EDT. Current level is 5597.50 on the Futures of the S&P 500.

Executive Summary: Back and forth we go. The S&P 500 is now right below 5600. The range moved from 500 to 600 points on the S&P 500 for the year, 5500 to 6100. Futures are higher this morning and 5500 is now support. Moving above 5600 would be a big deal. Baby steps.

And so it begins, three consumer companies (PEP CAG SJM) call for no tariffs on ingredients not available in the U.S. Capital Chronyism at its worst. As long as companies can lobby, the swamp has not been drained. That said, this exemption does make sense as if there is no ingredient in the U.S., why tax it? The Trump Administration has it backwards. Get the Income Tax extension through. Encourage growth. Then deal with Tariffs, one by one.

Breaking: PPI Up 0.0%. That is crazy good!!

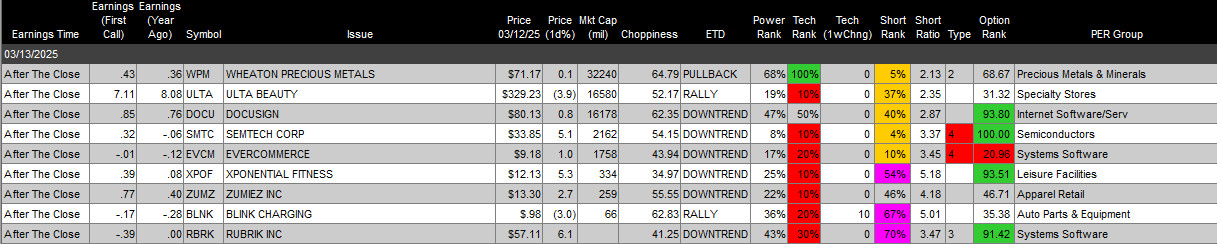

Chart of the Day: Adobe (ADBE) reported earnings and gave guidance. However, the chart is weak and it is lower. Not a surprise to us.

Key Events of Note Today:

- PPI is due out at 8:30 a.m. EDT and will drive today’s action.

- Weekly Jobless Claims are due out at 8:30 a.m. EDT.

- Weekly Natural Gas Inventories are due out at 10:30 a.m. EDT.

- 30-Year Note Auction at 1:00 p.m. EDT.

Notable Earnings Out After The Close

- Beats: ABDE +0.11, PHR +0.07, BRY +0.06, PATH +0.06, AEO +0.04, CVGW +0.04, S +0.03 of note.

- Misses: None of note.

- IPOs For The Week: APUS, FATN, KMTS. OMGE, SAGT,

WGRX - New IPOs/SPACs launched/News:

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced:

- TARS announces proposed $100 million public offering

- Notes Priced:

- ESGR Pricing of $350 Million of 7.500% Fixed-Rate Reset Junior Subordinated Notes Due 2045

- FDUS Prices Public Offering of $100 Million of 6.750% Notes Due 2030

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders of note:

- Mixed Shelf Offerings:

- MRVL files mixed securities shelf offering

- LODE FORM S-3 – $50,000,000 Mixed Shelf Offering

- Convertible Offerings & Notes Filed:

- ATEN announces proposed offering of $200 million of convertible senior notes

- NN $190 Million of 5% Redeemable Senior Secured, Convertible Transaction

- ITGR Announces Launch of Convertible Notes Offering

Biggest Movers Up & Down Yesterday:

- Movers Up: RAIL +13.8%, INTC +10.8%, BRY +7.4%, CVGW +5.6%, ASTL +0.4% of note.

- Movers Down: PATH -16.6%, S -13.4%, BTMD -8.6%, NN -7.6%, AEO -5.4%, ADBE -3.7% of note.

News After The Close:

- Intel (INTC) names new CEO Lip-Bu Tan.

- Rocket Lab (RKLB) announces InterMission and MAX Constellation, two next-generation software suites that build on successful missions to the Moon and beyond to deliver advanced autonomy, security, and scalability for complex space missions and constellation operations.

- Senate Minority Leader Schumer indicates continuing resolution passed by House won’t have votes to get through Senate.

- Spirit Airlines exits chapter 11 significantly deleveraged and with new financing to support return to profitability.

- PepsiCo (PEP), Conagra (CAG) and J M Smucker (SJM) request that Trump exempt ingredients not available from US sources. (Reuters)

- 10K or Qs Filings/Delays – (Filed), (Delayed) of note.

Exchange/Listing/Company Reorg and Personnel News:

- TTD appoints Vivek Kundra as COO, effective March 31

Buybacks

- NABL approves a share repurchase program for up to $75.0 mln shares of common stock.

- CHDN approves a new $500 mln share repurchase program.

- MCB announces $50 million stock repurchase program.

Dividends Announcements or News:

- Stocks Ex Div Today: HD LIN PSA BR SBAC CTRA LKQ DRS ADT AMKR BDC NSP MDU CCOI MCY TUYA VSH LMAT AMBP CASH ARIS PRG.

- Stocks Ex Div Tomorrow: META KO TMO GILD ADP CB WM MSI WMB CRH DLR NWG CCI NDAQ AME GRMN VRSK XEL EXR EBAY TKO GPN DVN

- BBW increases quarterly cash dividend 10% to $0.22/share from $0.20/share.

- AHH decreases quarterly cash dividend to $0.14/share from $0.205/share.

What’s Happening This Morning: (as of 8:15 a.m. EDT) Futures S&P 500 -21, NASDAQ -62 Dow Jones -57. Europe is lower with Asia lower as well. Bonds are at 4.337% from 4.31% Wednesday on the 10-Year. Crude Oil and Brent Crude are lower with Natural Gas lower. Gold higher with Silver and Copper lower. The U.S. Dollar is higher versus the Euro, higher against the Pound andlower against the Yen. Bitcoin is at $82,697 from $83,034 lower by $104 by -0.12%.

- Daily Positive Sectors: Technology, Communication Services, Consumer Cyclicals, Energy and Financials were higher.

- Daily Negative Sectors: Consumer Defensive, Healthcare, Real Estate and Materials were lower.

- One Month Winners: Real Estate, Consumer Defensive, Utilities and Healthcare of note.

- Three Month Winners: Communication Services, Consumer Defensive, Financials and Healthcare of note.

- Six Month Winners: Communication Services, Financials, Consumer Cyclical and Utilities of note.

- Twelve Month Winners: Financials, Utilities, Communication Services, Technology and Consumer Defensive of note.

- Year to Date Winners: Financials, Healthcare, Consumer Defensive, Materials and Real Estate of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Thursday After the Close:

- Friday Before The Open:

Notable Earnings of Note This Morning:

- Flat: None of note

- Beats: GIII +0.30, WB +0.01 of note.

- Misses: DG -0.64 of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: of note.

- Negative or Mixed Guidance: AEO S PATH DG GIII of note.

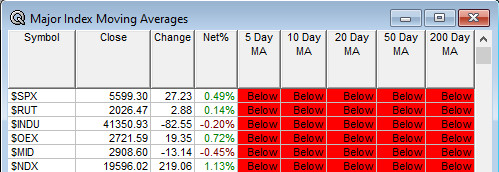

Advance/Decline Daily Update: the A/D fell to major support making new lows, before a rebound and continues to make new lows.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: RAIL +12.5%, INTC +11.2%, ASTL +9.8%, NVX +7.1%, CVGW +5.4%, FUTU +5.1%, CANG +4.8%, ACNT +4.7%, NABL +2.8%, WB +2.8%, RNA +2.7%, ARMN +2.5%, CSV +2.4% of note.

- Gap Down: PATH -18.3%, S -13.9%, AEO -8.6%, ATEN -8.4%, VNET -8.3%, NN -7.4%, LOGC -5%, BTMD -4.9%, ADBE -4.7%, TARS -3.4% of note.

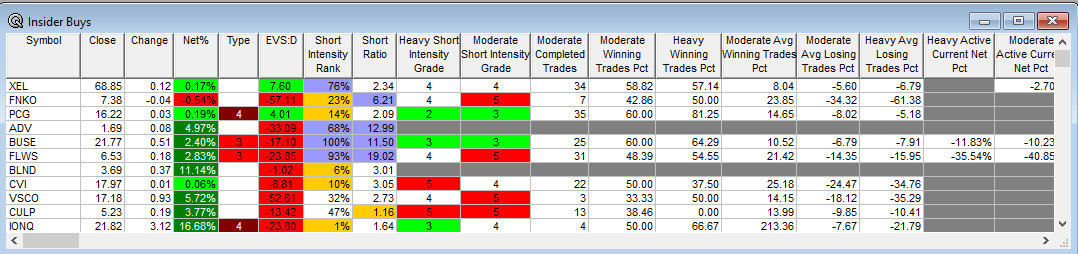

Insider Action: XEL BUSE sees Insider Buying with dumb short selling. FLWS sees Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Market Wrap: Stock Futures slip ahead of inflation data. (Bloomberg)

- Bloomberg: Trump Vows 200% Tax on EU Wines Unless European Taxes Lowered On U.S. Whiskey. (Bloomberg)

- Stocks Making The Biggest Moves: Not out yet. (CNBC)

- Convenience store sales down in February. (WSJ)

- FTC to take Amazon (AMZN) to trial. (CNBC)

- Bloomberg Odd Lots – Is there an affordable fix to affordable housing? (Podcast)

Bolded Royal Blue means behind a Pay Wall.

Economic:

- February PPI is due out at 8:30 a.m. EDT and is expected to drop to 0.3% from 0.4%.

- Weekly Jobless Claims and Natural Gas Inventories are due out at 8:30 a.m. EDT and 10:30 a.m. EDT.

Geopolitical: (Watch our Twitter feed, Bullet86, for any impromptu appearances)

- President Trump’s Daily Schedule.

- President Trump meets with the Secretary General of NATO at 12:20 p.m. EDT and then has a working lunch.

- Federal Reserve Speakers are in blackout now until March 20th when the latest meeting has concluded.

M&A Activity and News:

Moving Average Table: Remains at 0% today. Third day in a row at 0. Ouch!!

Meeting & Conferences of Note: (Not updated today, back tomorrow)

-

- Sellside Conferences:

- Barclays Global Healthcare Conference

- Jefferies MedTech Doctor Day

- JP Morgan Gaming, Lodging, Restaurant & Leisure Management Conference

- JP Morgan Industrials Conference

- Mizuho US Consumer Industrials & TMT Summit

- UBS Consumer and Retail Conference

- Sellside Conferences:

-

- Shareholder Meetings: A, ACET, ADUR, FFIV, HURC, NB

- Top Analyst, Investor Meetings: ALT, BECN, CHEF, COCP, FAST, LWLG, NABL, NCMI, NVMI

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation:

- Industry Meetings or Events:

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

- Upgrades: SCCO NVO MSFT MRCY CTRE CRVO

- Downgrades: SEAT PATH MC AEO

-