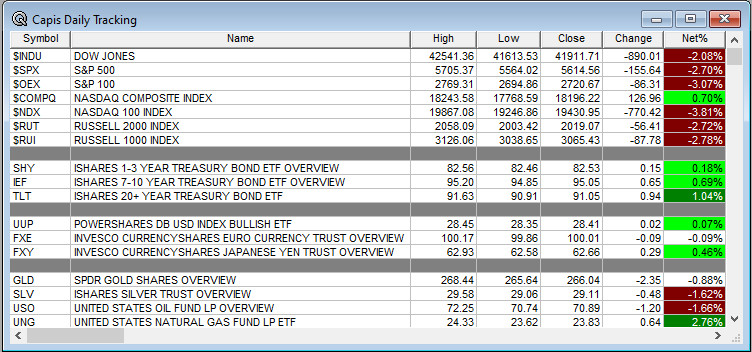

Overnight Summary & Early Morning Trading: The S&P 500 finished Monday lower by -2.70% at 5614.56. It was the worst trading day of the year. Friday was higher by 0.55% at 5770.20. Futures are higher this morning by +10.25 on the S&P 500 at 7:15 a.m. EDT. Current level is 5647 on the Futures of the S&P 500.

Executive Summary: Back and forth we go. The S&P 500 is now below 5700. The range moved from 400 to 500 points on the S&P 500 for the year, 5600 to 6100. Futures are higher this morning and 5600 is now support.

Breaking:

Chart of the Day: Delta lowered guidance after the close. Were we ahead on this downward move? Yes.

Key Events of Note Today:

- February NFIB Small Business Optimism is out and came in at 100.70 against 102.80 in January.

- The latest JOLTS data is due at 10:00 a.m. EDT.

- API Petroleum Report is due out at 4:30 p.m. EDT.

Notable Earnings Out After The Close

- Beats: LMB +0.036, MTN +0.27, AVO +0.07, METC +0.05, PAY +0.02. ASAM +0.01 of note.

- Misses: SARO -0.17, HPK -0.09, ORCL -0.02 of note.

- IPOs For The Week: APUS, FATN, KMTS. OMGE, SAGT,

WGRX - New IPOs/SPACs launched/News:

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced:

- MBOT: Form S-3.. 12,542,268 Shares of Common Stock

- MLYS Proposed Public Offering of Common Stock – $250.0 million of shares

- Notes Priced:

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders of note:

- Mixed Shelf Offerings:

- AISP: FORM S-3 – $50,000,000 Mixed Shelf Offering

- Convertible Offerings & Notes Filed:

- HTGC Closes Offering of $287.5 Million of Convertible Unsecured Notes

Biggest Movers Up & Down Last Week:

- Movers Up: SUPV +7.4%, METC +7.1%, PAY +6%, SARO +4.5%, MTN +4.2%, FTK +4.2%, ILMN +3.5%, ORCL +2.2%, of note.

- Movers Down: ASAN -26%,RDW -17.6%, DAL -13.3%, MYPS -12%, AVO -8.1% of note.

News After The Close:

- ILMN ticks +3% higher after aiming to cut $100 mln in costs, lowers FY25 adjusted EPS guidance.

- CNS reports preliminary assets under management (AUM) of $88.6 bln as of February 28, 2025, up $2.1 bln from January 31, 2025.

- DAL lowers its Q1 guidance due to recent reductions in consumer and corporate confidence caused by increased macro uncertainty.

- 10K or Qs Filings/Delays – (Filed), (Delayed) of note..

Exchange/Listing/Company Reorg and Personnel News:

- ASAN Co-Founder, CEO and Chair, Dustin Moskovitz, informs company of his intention to transition to role of Chair when a new CEO begins.

- DPZ promotes Joseph Jordan to COO and President of Domino’s U.S.

- NVGT appoints David Li as President and CEO, effective April 7.

- LUNR – Completion of Redemption of its Outstanding Warrants

- SEZL declares a six-for-one stock split.

Buybacks

- SEZL announces a $50.0 mln stock repurchase program.

- AMAL announces new $40.0 mln stock repurchase program, replacing previous share repurchase authorization.

Dividends Announcements or News:

- Stocks Ex Div Today: FIS AEE LPLA EXE OMC BWXT G CHRD JXN NJR INGM SR JWN IGT GLNG GOGL SEI NRP.

- Stocks Ex Div Tomorrow: NVDA LUV HPQ NVS SFL PFG POOL AER ORA ICL NWSA REG CRGY NSSC NWS PHI OSW EE.

- KFY increases quarterly cash dividend 30% to $0.48/share from $0.37/share.

What’s Happening This Morning: (as of 8:15 a.m. EDT) Futures S&P 500 +26.50, NASDAQ +105.50, Dow Jones +164 Russell 2000 +17.50. Europe is lower ex Germany with Asia lower ex China. Bonds are at 4.236% from 4.24% Monday on the 10-Year. Crude Oil and Brent Crude are higher with Natural Gas higher. Gold, Silver and Copper higher. The U.S. Dollar is lower versus the Euro, lower against the Pound and higher against the Yen. Bitcoin is at $81,559 from $82,235 higher by $2751 by +3.50%.

- Daily Positive Sectors: Utilities and Energy were higher.

- Daily Negative Sectors: Technology, Consumer Cyclical, Communication Services, Financials and Materials were lower.

- One Month Winners: Real Estate, Consumer Defensive, Utilities and Healthcare of note.

- Three Month Winners: Communication Services, Consumer Defensive, Financials and Healthcare of note.

- Six Month Winners: Communication Services, Financials, Consumer Cyclical and Utilities of note.

- Twelve Month Winners: Financials, Utilities, Communication Services, Technology and Consumer Defensive of note.

- Year to Date Winners: Financials, Healthcare, Consumer Defensive, Materials and Real Estate of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Tuesday After the Close:

- Wednesday Before The Open:

Notable Earnings of Note This Morning:

- Flat: FWRG of note

- Beats: LEGN +0.33, CIEN +0.23, KSS +0.23, HLLY +0.10, VIK +0.09, DKS +0.07, KFY +0.06, UNFI +0.04 of note.

- Misses: FERG -0.06 of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: FWRG of note.

- Negative or Mixed Guidance: KSS HLLY of note.

Advance/Decline Daily Update: the A/D fell to major support making new lows, before a rebound and just made a new low.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: TSVT +76.8%, FTK +9.7%, PAY +8.4%, FISI +7.9%, HPK +5.8%, MTN +5.4%, MGIC +5.1%, ALKT +4.5%, NGVT +3.8%, FVRR +3.8%, SNCY +3.2%, ASML +3%, RYN +2.6%, METC +2.5%, IOT +2.4%, EWCZ +2.3%, IONQ +2.2%, WNS +2.1%, SARO +2.1%, SEZL +2% of note.

- Gap Down: ASAN -27.4%, RDW -15.6%, DAL -11%, UAL -7.5%, AVO -6.9%, AAL -6.3%, CTRE -6.2%, MYPS -5.3%, KOD -4%, CHRS -3.8%, JBLU -3.4%, LUV -2.4% of note.

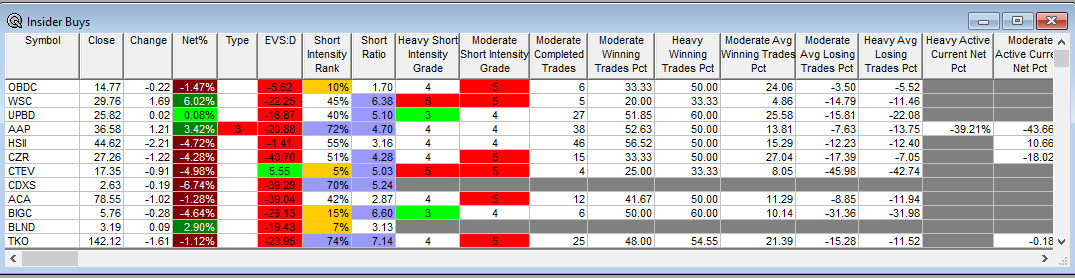

Insider Action: AAP sees Insider Buying with dumb short selling. TKO sees Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Market Wrap: US Stock Futures higher as Trump to meet with CEOs. (Bloomberg)

- Bloomberg: Traders Search For Havens as US Stocks Selloff Rattles Nerves. (Bloomberg)

- Stocks Making The Biggest Moves: . (CNBC)

- Southwest (LUV) ends free checked bags. (Bloomberg)

- Kohls (KSS) plunges 15% on outlook. (CNBC)

- 5 Things To Know Before the Market Opens. (CNBC)

- Bloomberg Odd Lots – Cathie Wood on what’s next in AI and Big Tech. (Podcast)

Economic:

-

Due this week: NFIB Small Business Optimism, CPI, Treasury Budget, PPI, University of Michigan Consumer Sentiment.

Geopolitical: (Watch our Twitter feed, Bullet86, for any impromptu appearances)

- President Trump’s Daily Schedule.

- President Trump and the vice president have lunch at 12:30 p.m. EDT.

- There is a Press Briefing at 1:00 p.m. EDT by the Press Secretary.

- President Trump delivers remarks to the Business Roundtable at 5:00 p.m. EDT.

- President Trump attends the swearing in of the new head of the Secret Services at 5:00 p.m. EDT.

- Federal Reserve Speakers are in blackout now until March 20th when the latest meeting has concluded.

M&A Activity and News:

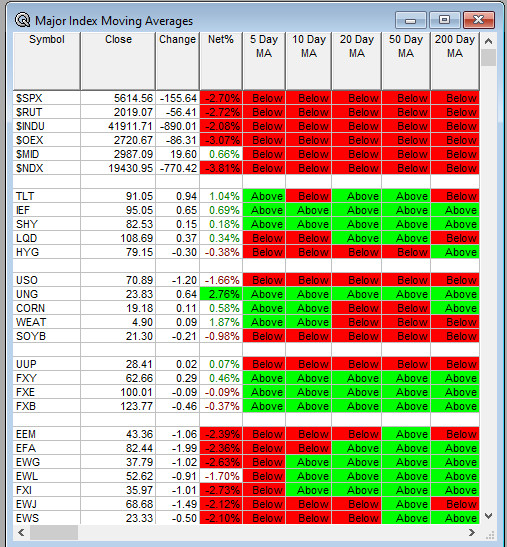

Moving Average Table: Moves from 9% to 0% today.

Meeting & Conferences of Note: (Not updated today, back tomorrow)

-

- Sellside Conferences:

- Bank of America Consumer and Retail Conference

- Barclays Global Healthcare Conference

- BNP Paribas Ingredients Conference

- Cantor Global Technology Conference

- Citi TMT Conference

- Deutsche Bank Media, Internet & Telecom Conference

- Evercore Private Markets Forum

- JPM Industrial Conference

- Jefferies Biotech on the Bay Summit

- Leerink Healthcare Conference

- Loop Markets Investor Conference

- Mizuho US Consumer Industrials & TMT Summit

- Piper Western Bank Forum

- Stifel Technology One-on-One Conference

- Wolfe Research FinTech Forum

- Sellside Conferences:

-

- Shareholder Meetings: ADUR, DERM, EFSH, IRFX, MMS, TOL

- Top Analyst, Investor Meetings: ACVA, BIGC, ETN, GLBE, RRD, SLAB, TER

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation:

- Industry Meetings or Events:

- Women in Data Science Conference

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

- Upgrades: U ONON GEHC

- Downgrades: AFYA

-