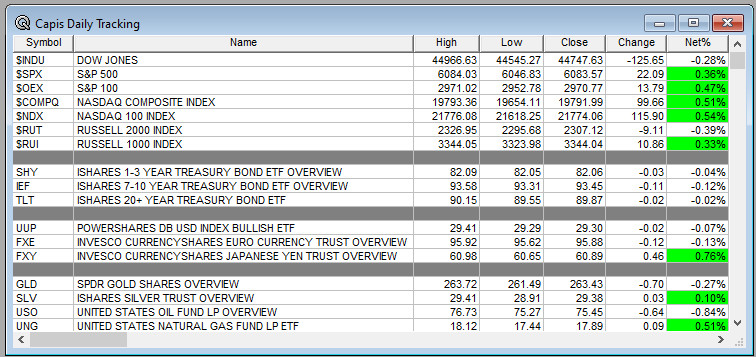

Overnight Summary & Early Morning Trading: The S&P 500 finished Thursday higher by 0.36% at 6083.57. Wednesday higher by 0.39% at 6061.48. The overnight high was hit at 6109.50 at 6:50 a.m. EDT and the low was hit at 6094 at 1:35 a.m. EDT. The overnight range is 15 points. The current price is higher at 7:10 a.m by +0.01% at 6106.75 up +0.75 points.

Executive Summary: Stocks are stabilizing from recent weakness into today’s Jobs Report.

Articles of Note: “Sovereign Wealth For Presidents” by WSJ Editorial Board.

*Note that certain articles highlighted may require a subscription. We highlight noted sources like the WSJ or Bloomberg that have wide audiences.

Key Events of Note Today:

-

- Monthly Jobs Report Report and University of Michigan Consumer Sentiment are due out at 8:30 a.m. EDT and 10:00 a.m. EDT along with Baker Hughes Rig Count at 1:00 p.m. EDT.

- 4-Week Bill Auction at 11:30 a.m. EDT.

Daily Chart Request: Want to see an Erlanger Chart in The Morning Note? Simply send an email to us at [email protected] and we will more than likely show it.

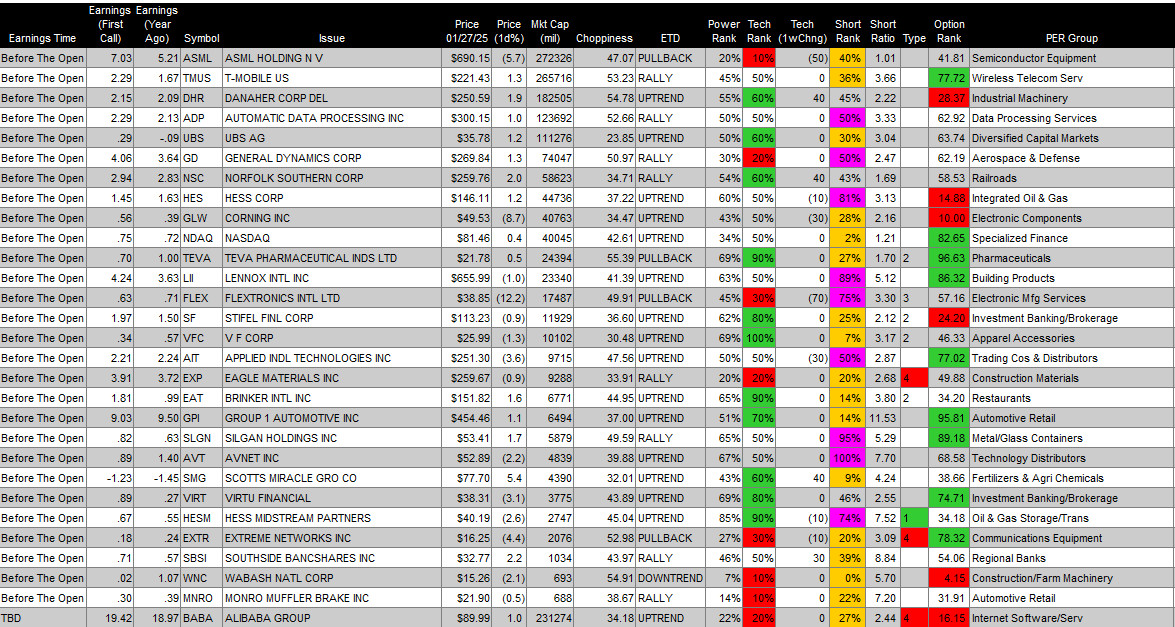

Amazon (AMZN) beat estimates by $0.37 and had impressive quarterly sales. The stock is lower by -3.07% this morning.

Notable Earnings Out After The Close

- Beats: VST +0.93, CLSK +0.91, MTD +0.69, AFRM +0.39, AMZN +0.37, EXPE +0.30, ATR+0.26, POWL +0.25, SSNC +0.25, TTWO +0.24. QLYS +0.23, POST+0.21, LGFA +0.19, BYD +0.17, FTNT +0.13, CNO +0.11, DOCS +0.11, MPWR +0.11, NBIX +0.11, MHK +0.10 of note. (>+0.10)

- Flat: None of note.

- Misses: RGA -0.29, WERN -0.13, MTX -0.11, SKX -0.10, PINS -0.08, MCHP -0.08, FBIN -0.07, NMIH -0.05, ELF -0.02, STEP -0.01, LESL-0.01 of note.

- IPOs For The Week: FBGL, TTAM

- New IPOs/SPACs launched/News:

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced:

- STIM announces launch of underwritten public offering of common stock.

- Notes Priced:

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders of note:

- Mixed Shelf Offerings:

- FDS files mixed shelf securities offering.

- PIPE:

- Convertible Offerings & Notes Filed:

- MUX announces proposed offering of $85 million of convertible senior notes.

Biggest Movers Up & Down Yesterday:

- Movers Up: DOCS +21.8%, PINS +19%, NET +14%, LEU +11.8%, AFRM +11.7%, MPWR +11% of note.

- Movers Down: BILL -30%, ELF -25.8%, SKX -12.5%, MCHP -6.8%, AMZN -5.4% of note.

News After The Close:

- Amazon (AMZN) put up strong numbers with mixed Q1 guidance not good enough for investors as the stock is off -5.0% in after hours.

- Pinterest (PINS) shares surge 20% after Q4 beat. (CNBC)

- 10K or Qs Delays – none of note.

Exchange/Listing/Company Reorg and Personnel News:

- POWI CEO Balu Balakrishnan to retire, he intends to serve as executive chairman of the company’s board for as long as is needed to ensure a smooth transition to his successor.

- PROV CFO TamHao B. Nguyen has resigned effective February 21, 2025 in order to pursue another opportunity.

- ESCA appoints Armin Boehm as CEO, effective April 1; to succeed Walter P. Glazer, Jr., who previously announced plans to retire.

Buybacks:

- MPWR has approved a new stock repurchase program that authorizes MPS to repurchase up to $500 mln in the aggregate of its common stock, which will expire on February 4, 2028.

- PIPR has authorized the repurchase of up to $150 mln of the company’s outstanding common stock.

Dividends Announcements or News:

- Stocks Ex Div Today: AAPL IBM BX AEP AMP GWW ETR LVS CQP OHI ARMK WBS WTRG X LAZ MWA FIBK NOMD CWT GLP SJW RES PZZA NMM GABC FBMS MATW.

- Stocks Ex Div Tomorrow:

- EXPO increases quarterly cash dividend to $0.30/share from $0.28/share

- ALLE increases quarterly cash dividend by 6% to $0.51/share from $0.48/share

What’s Happening This Morning: (as of 8:15 a.m. EDT) Futures S&P 500 -1.25, NASDAQ -7, Dow Jones +11 and Russell 2000 -1.02. Europe is lower ex Germany with Asia is lower. Bonds are at 4.44% unchanged from yesterday on the 10-Year. Crude Oil and Brent Crude are higher with Natural Gas higher as well. Gold, Silver and Copper higher. The U.S. Dollar is higher versus the Euro, lower against the Pound and higher against the Yen. Bitcoin is at $97,889 from $98,433 higher by $1206 up by +1.25%. Additional Comments: The S&P 500 has now broken back above 6000 and now it has become support in a back and forth with the 6000 level.

- Daily Positive Sectors: Financials, Materials, Consumer Defensive, Technology and Communication Services were higher.

- Daily Negative Sectors: Energy and Helathcare were lower.

- One Month Winners: All except for Technology of note.

- Three Month Winners: Communication Services, Consumer Cyclical, Financials and Technology of note.

- Six Month Winners: Consumer Cyclical, Financials, Communication Services, Utilities and Industrials of note.

- Twelve Month Winners: Technology, Communication Services, Financials, Consumer Cyclical and Utilities note.

- Year to Date Winners: Energy, Healthcare, Communication Services, Materials, Utilities, Industrials and Technology of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Friday After the Close: None of note.

- Monday Before The Open:

Notable Earnings of Note This Morning:

- Beats: ROAD +0.10, PRLB +0.06, PWP +0.05, FLO +0.02, NWL +0.02, AVTR +0.01, PAA +0.01 of note. (>+0.10)

- Flat: KIM of note.

- Misses: GPRE -0.51, of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: of note.

- Negative or Mixed Guidance: of note.

Advance/Decline Daily Update: The A/D fell to major support, bounced, made new lows and now is bouncing.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: DOCS +23.7%, PINS +21.9%, AFRM +16.6%, LEU +14%, DC +12%, EXPE +10.2%, NET +9.5%, FTNT +8.4%, BYD +7.9%, MPWR +7.4%, SYNA +6.9%, CLSK +6.4%, TTWO +6%, IBEX +5.5%, POWI +5%, KRMD +4.9%, STEP +4.6%, TBN +4.1%, SSNC +3.9%, NGVC +3.8%, SLRN +3.7%, PRLB +3.6%, EHC +3.5%, CDLR +3.3%, QNST +3.3%, G +3.3%, SARO +3.1%, ESCA +3.1%, LGF.A +3%, PCTY +2.9%, MTD +2.8%, NVO +2.6%, PRO +2.3%, MHK +2.1% of note.

- Gap Down: BILL -27.9%, ELF -26.9%, STIM -22.5%, WBTN -18.5%, ALMS -16.5%, GPRO -15.8%, NBIX -13.6%, LTRX -12.9%, SKX -12.1%, LESL -11.2%, CLFD -10.8%, MTX -10%, MUX -8.7%, MCHP -6.4%, ONTO -6%, CDP -5.7%, AVTR -5.5%, ILMN -4.7%, RGA -4.6%, ACB -4%, GRPN -3.7%, AMZN -3.2%, POWL -3.2%, CNO -2.8%, OTEX -2.6%, CUZ -2.4%, NMIH -2.4%, VCTR -2.3%, VSAT -2.2%, MATW -2.2% of note.

Insider Action: Non of note see Insider Buying with dumb short selling. None of note see Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Lead Story on Bloomberg: Trump Takes Aim at The Carry Trade in Private Equity. (Bloomberg)

- Market Wrap: Stocks and Bonds steady with all eyes on payrolls. (Bloomberg)

- Stocks Making The Biggest Moves: . (CNBC)

- Five Things To Know Before The Market Opens. (CNBC)

- India’s Central Bank cuts rates for the first time in 5 years. (CNBC)

- Telsa (TSLA) car sales in China fall -11.50%. (CNBC)

- Bloomberg Odd Lots: Palantir’s vision for U.S. Defense spending. (Podcast)

- Bloomberg Big Take: How Economists think about the future of AI. (Podcast)

Economic:

- January Nonfarm Payrolls is due out at 8:30 a.m. EDT and is expected to fall to 155,000 from 256,000. The unemployment rate is expected to stay at 4.10%.

- January University of Michigan Consumer Sentiment is due out at 10:00 a.m. EDT and expected to rise to 71.30% from 71.10%.

- Weekly Baker Hughes Rig Count is due out at 1:00 p.m. EDT.

Geopolitical: (Watch our Twitter feed, Bullet86, for any impromptu appearances)

- President Trump’s Daily Schedule.

- President Trump greets the Prime Minister of Japan at 11:30 a.m. EDT and is with him until 2:00 p.m. EDT.

- President Trump makes a Faith Office Announcement at 2:00 p.m. EDT and signs Executive Orders.

- President Trump heads to Mar-A-Largo at 3:00 p.m. EDT for the weekend.

- Federal Reserve Governor Michelle Bowman speaks at 9:25 a.m. EDT.

- Federal Reserve Governor Adriana Kugler speaks at 12:00 p.m. EDT.

M&A Activity and News:

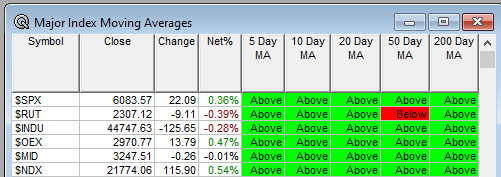

Moving Average Table: Rises to 97% from 70%.

Meeting & Conferences of Note:

-

- Sellside Conferences:

- Piper Sandler & Co TSLP Day

- Sellside Conferences:

-

- Shareholder Meetings: BLBX, IDAI

- Top Analyst, Investor Meetings: OWL, QNCX, ZKIN

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation:

- Industry Meetings or Events:

- Chicago Auto Show

- Small Cap Growth Investor Conf

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

- Upgrades: G PINS HON DECK APTV

- Downgrades: MDLZ RBLX

-