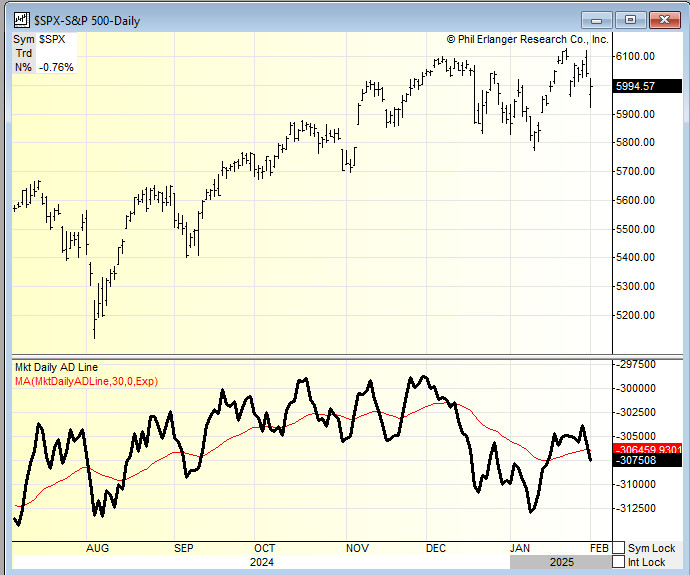

Overnight Summary & Early Morning Trading: The S&P 500 finished Tuesday higher by 0.72% at 6037.88. Monday lower by -0.76% at 5994.57. The overnight high was hit at 6057.75 at 4:05 p.m. EDT and the low was hit at 6020.25 at 5:00 a.m. EDT. The overnight range is 31 points. The current price is lower at 7:10 a.m by -0.44% at 6036.50 down -26.50 points.

Executive Summary: The S&P 500 fell by -1% or more on three days in January. So we clustered with multiple -1% losses during last month. Key will be if February can break the clustering pattern. Monday the S&P 500 had its first down day of more than -1% at the open but finished with a loss of less than -1%. Each day has seen weak futures overnight that yesterday turned around by the open. Can we do that two days in a row?

ADP Payroll comes in at 183,000 just announced at 8:15 a.m. EDT.

Articles of Note:

*Note that certain articles highlighted may require a subscription. We highlight noted sources like the WSJ or Bloomberg that have wide audiences.

Key Events of Note Today:

-

- ADP Payroll and ISM Services are due out at 8:15 a.m. EDT and 10:00 a.m. EDT.

- Weekly Crude Oil Inventories out at 10:30 p.m. EDT.

Daily Chart Request: Want to see an Erlanger Chart in The Morning Note? Simply send an email to us at [email protected] and we will more than likely show it.

Walt Disney (DIS) missed estimates by $0.05 but reaffirmed guidance. The stock is higher by 0.61% right now and it is on our Weekly Types Long List.

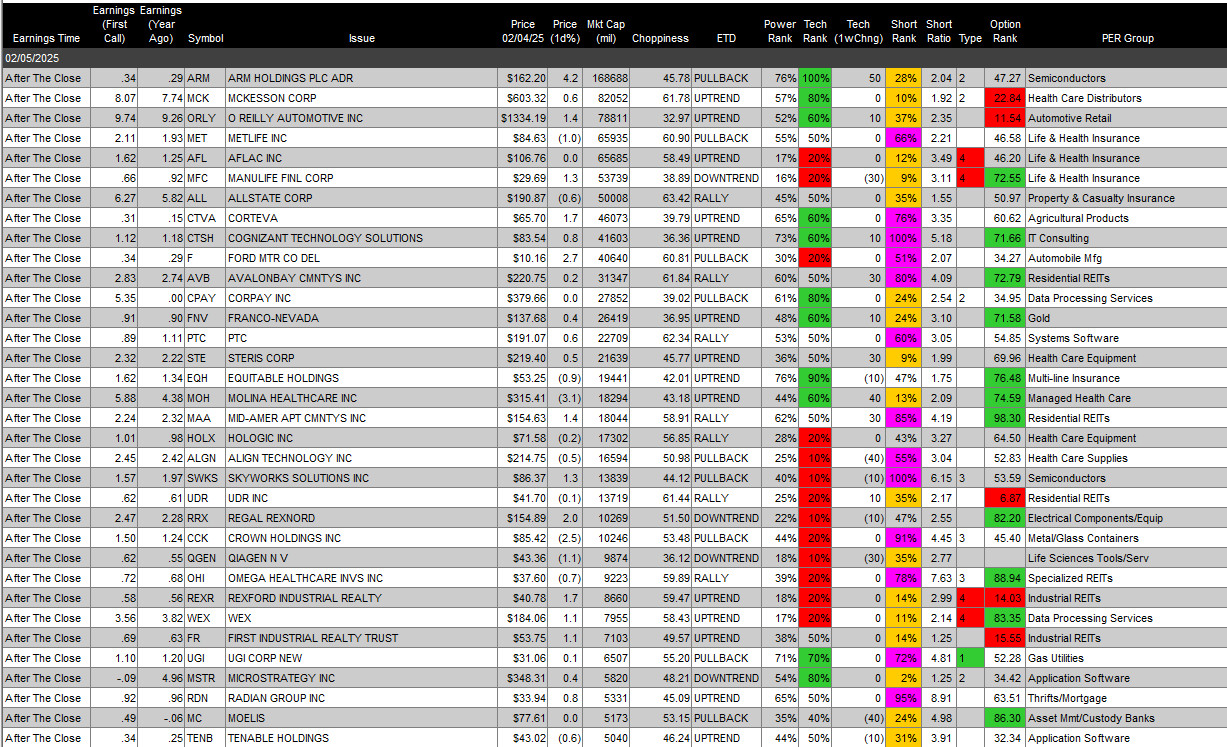

Notable Earnings Out After The Close

- Beats: VOYA +0.68, CRUS +0.47, SPG +0.26, AMGN +0.23, ENPH +0.21, FMC +0.19, MAT +0.15, LUMN +0.14, MRCY +0.12 of note. (>+0.10)

- Flat: None of note.

- Misses: FICO -0.30, PRU +0.28, UNM -0.11, HRB -0.08, WU -0.02, MDLZ -0.01 of note.

- IPOs For The Week: FBGL, TTAM

- New IPOs/SPACs launched/News:

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced:

- SDA announces follow-on public offering of up to $50 mln of Class A ordinary shares.

- GHRS – Pricing of $150 Million Public Offering.

- MBOT: FORM S-1 – 15,966,530 Shares of Common Stock.

- SHOT: FORM S-1 – 23,985,404 Shares of Common Stock

- Notes Priced:

- BVN Buenaventura Issues 144A/Reg S Offering of US$650 million Senior Unsecured Notes Due

2032.

- BVN Buenaventura Issues 144A/Reg S Offering of US$650 million Senior Unsecured Notes Due

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders of note:

- Mixed Shelf Offerings:

- CYCN: Form S-3.. $25,000,000 Mixed Shelf.

- PIPE:

- Convertible Offerings & Notes Filed:

Biggest Movers Up & Down Last Week:

- Movers Up: MRCY +14.2%, AVNW +13.6%, CRUS +7%, ENPH +6.8%, SNAP +6.4% of note.

- Movers Down: GOOG -7.7%, MTCH -9%, AMD -8.6%, CMG -4.8 of note.

News After The Close:

- China looking at Apple’s APP store fees. (Reuters)

- Goodyear Tire (GT) details agreement with the United Steelworkers.

- ARK Investments announced update 13F.

- 10K or Qs Delays – none of note.

Exchange/Listing/Company Reorg and Personnel News:

- CRUS announces the appointment of Jeff Woolard as chief financial officer, effective February 24, 2025

- MTCH appoints Spencer Rascoff as CEO, effective immediately; succeeds Bernard Kim, who is stepping down.

Buybacks:

Dividends Announcements or News:

- Stocks Ex Div Today: SLB BRO ATR IDA LPG UVSP

- Stocks Ex Div Tomorrow: HESM WTFC KBH MATX FELE FUL HOPE CCEC HFWA HTBK

- ACT announces quarterly dividend.

- MMM increases quarterly cash dividend to $0.73/share from $0.70/share.

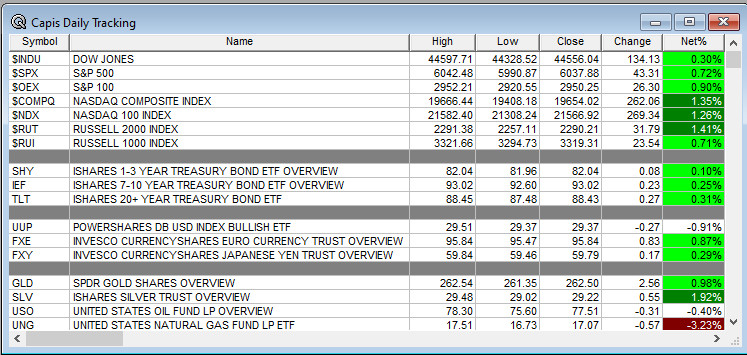

What’s Happening This Morning: (as of 8:15 a.m. EDT) Futures S&P 500 -26.50, NASDAQ -172, Dow Jones -85 and Russell 2000 +6 . Europe is lower ex the FTSE with Asia higher except for China. Bonds are at 4.458% from 4.588% on the 10-Year. Crude Oil and Brent lower with Natural Gas lower as well. Gold higher with Silver lower and Copper higher. The U.S. Dollar is lower versus the Euro, lower against the Pound and lower against the Yen. Bitcoin is at $99,461 from $95,466 lower by $-2,170 down -2.14%. Additional Comments: The S&P 500 has now broken back above 6000 and now it has become support in a back and forth with the 6000 level.

- Daily Positive Sectors: Energy, Technology, Consumer Cyclical and Communication Services were higher.

- Daily Negative Sectors: Consumer Defensive, Utilities, Industrials and Financials were lower.

- One Month Winners: All except for Technology of note.

- Three Month Winners: Communication Services, Consumer Cyclical, Financials and Technology of note.

- Six Month Winners: Consumer Cyclical, Financials, Communication Services, Utilities and Industrials of note.

- Twelve Month Winners: Technology, Communication Services, Financials, Consumer Cyclical and Utilities note.

- Year to Date Winners: Energy, Healthcare, Communication Services, Materials, Utilities, Industrials and Technology of note.

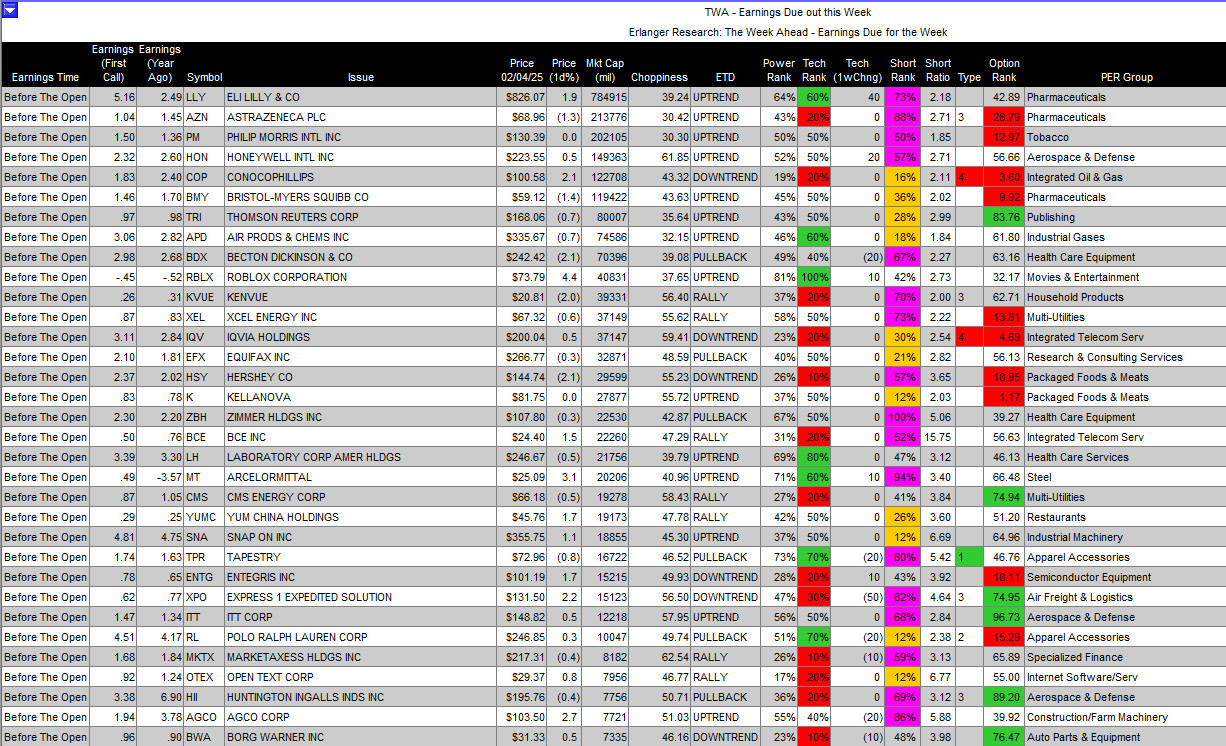

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Wednesday After the Close: (Above $5 Billion Market Cap)

- Thursday Before The Open: (Above $7 Billion Market Cap)

Notable Earnings of Note This Morning:

- Beats: UBER +2.71, EVR +0.59, CRTO +0.40, COR +0.23, SWK +0.22, GFF +0.20, TKR +0.17, CDW +0.16, DAY +0.15, EMR +0.10, ODFL +0.07, ATS +0.07, JCI +0.05, NYT +0.05, BSX +0.04, TECH +0.03, FI +0.03, AZTA +0.02, RXO +0.01 of note.

- Flat: REYN of note.

- Misses: ARES (0.75), HOG (0.28), GSK (0.26), CPRI (0.21), BG (0.11), VSH (0.08), SR (0.08), PFGC (0.07), TROW (0.07), DIS (0.05), FSV (0.04), ARCC (0.03), KMT (0.01) of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: PFGC JCI ENPH INTA MAT MWA UNM of note.

- Negative or Mixed Guidance: TKR ITW KMT BG CPRI REYN COLM FMC KLIC MDLZ of note.

Advance/Decline Daily Update: The A/D fell to major support, bounced, made new lows and now is FALLING AGAIN.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: MRCY +22.3%, AVNW +14.6%, MAT +13.4%, VEEA +13.2%, LUMN +9.7%, SAN +7.8%, VALN +7%, ENPH +6.2%, CRUS +6.1%, AMTM +5.9%, GSK +5.9%, APAM +5.3%, DOX +4.8%, LAES +4.5%, MOD +3.7%, MWA +3.6%, AZEK +3.5%, NVO +3.5%, WDAY +3.5%, TM +3%, ATS +2.7%, EA +2.4%, RILY +2.1%, ACT +2.1%, NMR +2% of note.

- Gap Down: FMC -21.2%, OSCR -11.2%, DXC -11%, CVRX -10.5%, NVCT -9.7%, SDA -8.9%, MTCH -8.4%, AMD -8.4%, INTA -7.6%, GOOG -6.8%, ATEN -6.4%, FICO -6.1%, CMG -6.1%, COLM -5.7%, MDLZ -4.3%, EQNR -4.3%, BG -4.2%, KLIC -4%, OI -3.6%, ARES -3.3%, UNM -3.2%, CSL -2.4%, HRB -2.2%, PRU -2.1%, IEX -2.1%, ARCC -2.1% of note.

Insider Action: FLWS sees Insider Buying with dumb short selling. TTSH sees Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Lead Story on Bloomberg: Trump Says US Should Take Ove Gaza. (Bloomberg)

- Market Wrap: US Futures fall on Google and AMD earnings. (Bloomberg)

- Stocks Making The Biggest Moves: Check back later. (CNBC)

- MBA Mortgage Applications rose 2.2%.

- Novo Nordisk beats on Q4. (CNBC)

- Bloomberg Odd Lots: US Payments System that Musk has access to now. (Podcast)

Economic:

- The Latest ADP Payroll Report is due out at 8:15 a.m. EDT and is expected to rise to 155,000 from 122,000.

- At 10:00 a.m. EDT, January ISM Services is due out and expected to fall to 53.90% from 54.10%.

- Weekly Crude Oil Inventories are due out at 10:30 a.m. EDT.

Geopolitical: (Watch our Twitter feed, Bullet86, for any impromptu appearances)

- President Trump’s Daily Schedule.

- At 1:00 p.m. there is a press briefing by the White House Press Secretary.

- President Trump meets with the Governor of Texas at 2:30 p.m. EDT.

- President Trump signs the No Men In Women’s Sports Executive Order at 3:00 p.m. EDT.

- President Trump meets with California Governor Gavin Newsom at 4:00 p.m. EDT.

- Federal Reserve Richmond President Thomas Barkin speaks at 91:00 a.m. EDT.

- Federal Reserve Chicago President Austan Goolsbee speaks at 1:00 p.m. EDT.

- Federal Reserve Governor Michelle Bowman speaks at 3:00 p.m. EDT.

- Federal Reserve Vice Chairman Phillip Jefferson speaks at 7:30 p.m. EDT.

M&A Activity and News:

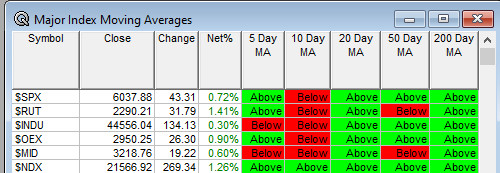

Moving Average Table: Rises to 70% from 37%.

Meeting & Conferences of Note:

-

- Sellside Conferences:

- Evercore ISI Travel & Transport Conf

- Guggenheim Biotech Conference

- Oppenheimer Healthcare Winter CEO & Investor Summit

- Sellside Conferences:

-

- Shareholder Meetings: BCTX, BERY, TWST

- Top Analyst, Investor Meetings: CLDI, DERM, DT, IPHA

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation:

- Industry Meetings or Events:

- AACR-JCA Joint Conference

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

- Upgrades: SLAB HAYW ENPH MAT CAH CMG

- Downgrades: WRBY FHI

-