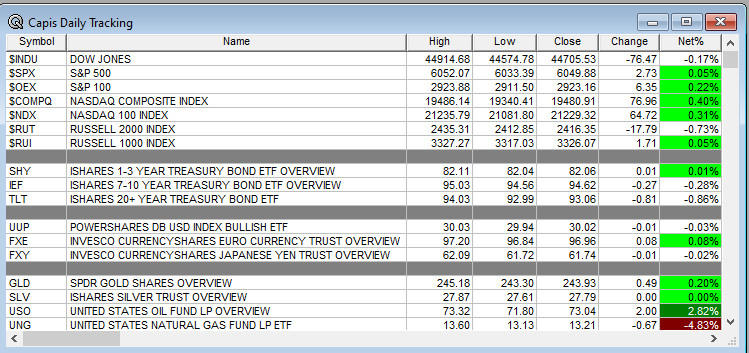

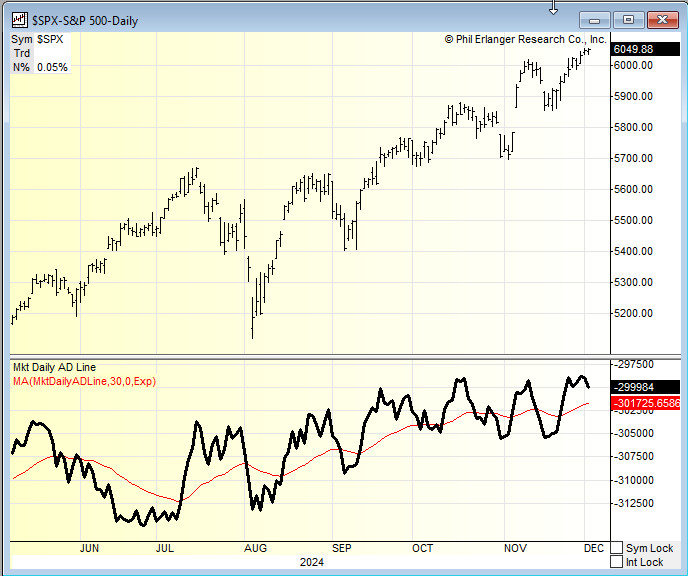

Overnight Summary & Early Morning Trading: The S&P 500 closed Tuesday higher by 0.05% at 6049.88 from Monday up 0.24% at 6047.15 at 6032.38. The overnight high was hit at 6081.75 at 6:35 a.m. EDT and the low was hit at 6063 at 6:00 p.m. EDT. The overnight range is 18 points. The current price is 6081 at 6:45 a.m.

Executive Summary: ADP Payrolls just came out at 146,00 a bit lighter than expected but still a decent number. Government Payroll number is due out on Friday. Fed Chairman Powell speaks at 1:45 p.m. and any time he talks of late stocks drop so expect a drop later afternoon.

Article of Note: “The Fed’s Next Big Policy Rethink Needs Rethinking” by Bill Dudley. (VettaFi)

Key Events of Note Today:

- Economic releases of note include ADP Payrolls, ISM Non-Manufacturing Index and Weekly Crude Oil Inventories.

Daily Chart Request: Want to see an Erlanger Chart? Simply email us at [email protected].

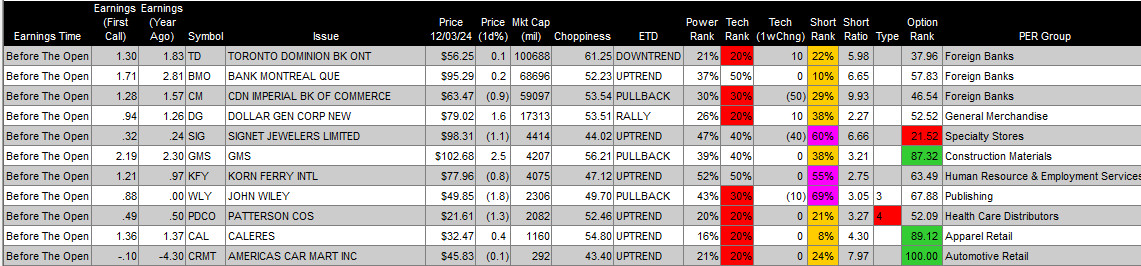

Next up is Foot Locker (FL). The stock is weak technically with a rank of 20% and has not been strong technically since August. Short Intensity is low at 35% with the Short Ratio at 2.72. This morning the stock is at $20.07 and is lower by $-4.09 on weaker earnings. The work nailed it. What to Do: We would sell as a Long Squeeze. To Short or Not To Short: We are not okay with being short or shorting this name that has worked as a short dropping from $33.94 making it a nice gainer on the short side since August.

Notable Earnings Out After The Close

- Beats: OKTA +0.09, PSTG +0.09, BOX +0.03, BASE +0.03, MRVL +0.02, DSGX +0.01 of note.

- Flat: None of note.

- Misses: CURV -0.04, CRM -0.03 of note.

- IPOs For The Week: ALEH, CJMB, DGX, FCHL, FTRK, HIT, JUNS,

LSE, NAMI, NTCL, YSXT, ZSPC - New IPOs/SPACs launched/News:

- IPOs Filed/Priced:

- Secondaries Filed or Priced:

- JANX announces proposed public offering of $300 mln of its common shares.

- LUNR announces launch of $65 mln of public offering of its Class A common stock and concurrent private placement.

- CRGY announces public offering of 18 mln shares of Class A common stock.

- ED announces public offering of 7.0 mln shares of common stock.

- ALCE: FORM S-1 – 4,993,341 shares of common stock

- Notes Priced: RC: Pricing of Public Offering of Senior Notes Due 2029

- Direct Offering:

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders of note:

- Mixed Shelf Offerings:

- PIPE:

- Convertible Offerings & Notes Filed:

- IREN announces $300 mln proposed convertible notes offering due 2030

- LYV – Pricing Of Convertible Senior Notes Offering

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down After The Close:

- Movers Up: HRTX +92.4%, (PSTG) +23.8%, OKTA +14.5%, MRVL +9.6%, CRM +6.9%, JANX +3.2% of note.

- Movers Down: CURV -23.8%, TRVI -23.7%, LUNR -13.7%, GXO -10.1%, BASE -10%, CRGY -3.6%, CPB -3.3% of note.

News After The Close:

- CRGY signs definitive agreement to acquire Eagle Ford assets from Ridgemar Energy for upfront consideration of $905 mln plus future oil price contingent consideration.

- CUK reports record-breaking bookings in 2024.

- HRTX announces that the U.S. District Court for the District of Delaware ruled in Heron’s favor in the Company’s patent litigation against Fresenius Kabi USA, LLC with respect to CINVANTI (aprepitant) injectable emulsion.

- Wells Fargo (WFC) essentially unchanged in after-hours trading as the company is set to sell its San Francisco headquarters as part of the bank’s broader shift to the east coast.

- ODFL reports LTL operating metrics for November. Revenue per day decreased 8.2% yr/yr due to an 8.0% decrease in LTL tons per day and a slight decrease in LTL revenue per hundredweight.

- RTX awarded $1.31 bln U.S. Navy contract modification.

- OPEC + likely prolonging oil cuts for Q1. (Reuters)

- 10-K “Delays -CLSK of note.

Buybacks or Repurchases:

- RJF authorizes common stock repurchase for up to $1.5 bln.

- CBT authorizes the repurchase of up to 10.0 mln additional shares of company’s common stock, increasing the current amount of shares available for repurchase to approximately 11.0 mln.

- RUSHA approves a new stock repurchase program for up to $150.0 mln of common stock.

- TRMK announces a new $100 mln stock repurchase program.

Exchange/Listing/Company Reorg and Personnel News:

- CPB elects Mick Beekhuizen to succeed Mark Clouse as President and CEO, effective Feb. 1, 2025.

- PRU appoints Andrew Sullivan as its next CEO, effective March 31.

- GXO announces that CEO Malcom Wilson plans to retire in 2025; He will continue to lead the company during the executive search process for his successor.

Dividends Announcements or News:

- Stocks Ex Div Today: CI SLB ODFL HAL AVY PJT AMKR FSK ICL AVT NPO PWP BBDC

- Stocks Ex Div Tomorrow: QCOM BLK ELV SRE NXPI KIM MOS HRB JXN ONB SLM DNB LANC HWC AMBP SBLK LZB AAT ARIS LB RYI

- TXNM increases quarterly cash dividend 5.2% to $0.4075/share from $0.3875/share.

- RJF increases quarterly cash dividend 11.1% to $0.50/share from $0.45/share.

- DTE increases quarterly cash dividend to $1.09/share from $1.02/share.

What’s Happening This Morning: Futures S&P 500 +18 , NASDAQ +148, Dow Jones +163 and Russell 2000 +4.75. Europe is higher ex the FTSE. Asia is higher ex Australia. Bonds are at 4.261% from 4.205% for the 10-Year. Crude Oil and Brent are higher with Natural Gas lower for a third day in a row. Gold, Silver and Copper are lower for a second day in a row. The U.S. Dollar is higher versus the Euro, higher versus the Pound and higher against the Yen. Bitcoin is at $95,905 from $95,669 yesterday morning higher by $333 with futures +0.38% this morning.

- Daily Positive Sectors: Communication Services, Technology, Energy and Materials of note.

- Daily Negative Sectors: Utilities, Real Estate, Financials and Industrials of note.

- One Month Winners: Consumer Cyclicals, Financials, Industrials, Energy and Utilities of note.

- Three Month Winners: Consumer Cyclicals, Financials, Communication Services, Industrials, Utilities, Consumer Defensive and Technology of note.

- Six Month Winners: Financials, Real Estate, Utilities, Consumer Cyclical and Technology of note.

- Twelve Month WinnerMOmONTs: Financials, Technology, Industrials, Utilities and Communication Services note.

- Year to Date Winners: Technology, Financials, Utilities, Communication Services and Industrials of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

Wednesday After the Close:

Thursday Before The Open:

Notable Earnings of Note This Morning:

- Beats: RY +0.92, CHWY +0.14, DLTR +0.05 of note.

- Flat: HRL

- Misses: THI -0.74, FL -0.07 of note.

- Still to Report:

Company Earnings Guidance:

- Positive Guidance: CRM, CHWY, MRVL, OKTA, PSTG of note.

- Negative or Mixed Guidance: FL, CURV of note.

Advance/Decline Daily Update: The A/D Line has been improving for the last two weeks.

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: HRTX +83.9%, PSTG +23%, OKTA +15.1%, MRVL +14.1%, CRM +12.5%, DLTR +6%, PBI +4.5%, NVAX +3.7%, RY +3.6%, SGML +3.3%, RLGT +3.1%, HIMX +3.1%, WULF +2.8%, DSGX +2.8%, GENI +2.6%, GSAT +2.4%, LLY +2.3%

- Gap Down: CURV -20.5%, LUNR -15.3%, TRVI -14%, BASE -8.7%, FL -7.5%, GXO -5.5%, TIPT -5.5%, CRGY -5.2%, THO -4.3%, HRL -3.7%, BOX -2.5%, RVMD -2.2%, GRFS -2.1%

Insider Action: None see Insider buying with dumb short selling. TTSH sees Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Lead Story on Bloomberg: South Korean parties seek to impeach President Yoon. (Bloomberg)

- 5 Things To Know Before The Market Opens. (CNBC)

- Stocks Making The Biggest Moves: . (CNBC)

- Market Wrap: US Futures see Tech lead gains ahead of Fed Chairman Powell at 1:45 p.m. EDT. (Bloomberg)

- Weekly Mortgage Applications are out and

- Foot Locker (FL) tumbles on weak guidance and sees Nike “softness”. (CNBC)

- GM sees a $5 billion hit to restructure China. (Bloomberg).

- Eli Lilly (LLY) beats Novo’s Wegovy in head to head trial. (Bloomberg)

- Bloomberg: The Big Take – The quiet rise of highly regulated home insurance. (Podcast)

Economic:

- November ADP Payroll is due out at 8:15 a.m. EDT and expected to fall to 177,000 from 233,000.

- November ISM Non-Manufacturing is due out at 10:00 a.m. EDT and expected to fall at 55.50% from 56%.

- Weekly Crude Oil Inventory update is out at 10:30 a.m. EDT.

Geopolitical:

- Federal Reserve St, Louis President Alberto Musalem speaks at 8:45 a.m. EDT.

- Federal Reserve Chairman Powell speaks at 1:45 p.m..

- The Latest Beige Book is due out at 2:00 p.m. EDT.

- President Biden is in Angola and Cape Verde before returning to the U.S. at 4:55 p.m. EDT

- Watch our Twitter feed, Bullet86, for an impromptu appearances.

M&A Activity and News:

- None of note.

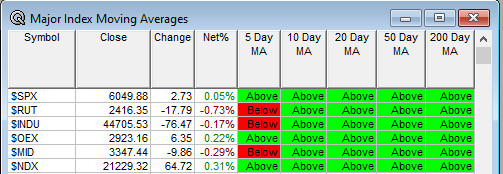

Moving Averages On Major Equity Indexes: Moves from 93% to 90%.

Meeting & Conferences of Note:

-

- Sellside Conferences:

- Bank of America Leveraged Finance Conference

- B. Riley Securities Energy Convergence Conference

- Barclays Eat Sleep Play Shop Conference

- Citi Basic Materials Conference

- Citi Global Healthcare Conference

- Goldman Sachs Industrials and Materials Conference

- Goldman Sachs Energy Clean Tech & Utilities Conference

- Jefferies Renewables & Clean Energy Conference

- Morgan Stanley Global Consumer & Retail Conference

- Needham Growth Conference

- Noble Markets Emerging Growth Equity Conference

- Piper Sandler Healthcare Conference

- Sidoti & Co. Small Cap Conference

- UBS Global Technology & AI Conference

- Wells Fargo MT Summit

- Wolfe Research Small and Mid-Cap Conference

- Sellside Conferences:

-

- Fireside Chat: None of note.

- Top Analyst, Investor Meetings: ACIC, AVNT, CBT, COUR, EW, GP, HOOD, UNH, ZTS

- Shareholder Meetings: EARN, HOLX, HYPR, QTI, SYBX

- Update: None of note.

- R&D Day: None of note.

- FDA Presentation:

- TARA: Data Presentation for TARA-002

- Company Event: None of note.

- Industry Meetings or Events:

- AMZN re:Invent Conference

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Upgrades: MRK

Downgrades: ALEC