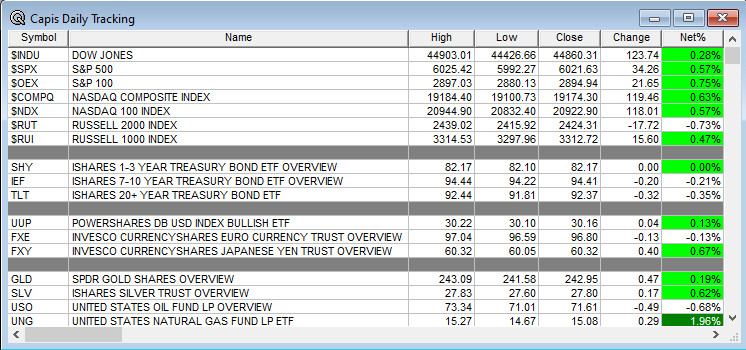

Overnight Summary: The S&P 500 closed Tuesday higher by 0.57% at 6021.63 from Monday higher by 0.30% at 5987.37. The overnight high was hit at 6046.50 at 9:45 p.m. EDT and the low was hit at 6024.25 at 6:25 a.m. EDT. The overnight range is 22 points. The current price is 6030.50 at 7:05 a.m. The S&P 500 is lower by -7.75 higher by -0.13% this morning.

Executive Summary: Enjoy your Turkey, stuffing and all the other food as well as second helpings and Turkey sandwiches on Friday and over the weekend!!

Article of Note: “Scott Bessent Has $6.7 Trillion Mountain of Worry Waiting at Treasury” by Robert Burgess (Bloomberg Opinion)

Key Events of Note Today:

- Economic releases of note are plentiful today as everything is getting push into today that would be reported tomorrow. As such, we have 8 releases between 8:30 and 12:00 p.m. EDT.

- 5-Year Bond Auction at 1:00 p.m. EDT.

Daily Chart Request: Want to see an Erlanger Chart? Simply email us at [email protected].

Next up is Uber Technologies (UBER). The stock is weak technically with a rank of 10%. Short Intensity has risen to 63% with the Short Ratio at 2.74. This morning the stock is at $71.56 and got an upgrade from Mark Mahaney of Evercore ISI who called it his favorite pick. What to Do: We would nibble here as an aggressive long idea moving to a short squeeze over time. If long, then we would add to the position. To Short or Not To Short: We are not okay with being short or shorting this name that has worked as a short dropping from $87 making it a nice gainer on the short side.

Notable Earnings Out After The Close

- Beats: URBN +0.24, WDAY +0.13, CRWD +0.12, JWN +0.11, NTNX +0.10, DELL +0.09, AMBA +0.08, PD +0.08 and ADSK +0.05 of note.

- Flat: HPQ of note.

- Misses: ARWR -4.03 and GES -0.03 of note.

- IPOs For The Week: BRIA, CGTL, JUNS, MTRS, PONY, VENU,

WYHG, YAAS - New IPOs/SPACs launched/News:

- IPOs Filed/Priced:

- Secondaries Filed or Priced:

- POET to complete $25 mln direct offering.

- BTM: Form 424B5 – Up to $13,000,000 Class A Common Stock

- DXYZ: Form 424B3 — Maximum Offering of 1,082,065 Shares

- Notes Priced:

- Direct Offering:

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders of note:

- LSAK files for 14,678,393 shares of common stock by selling shareholders

- STBX: FORM F-3 – 20,845,316 Class A Ordinary Shares Offered by Selling Shareholders

- Mixed Shelf Offerings:

- FISI files $200 mln mixed shelf securities offering

- COR files mixed shelf securities offering

- YORW files $60 mln mixed shelf securities offering

- PIPE: SCNX – Private Placement of $3 Million of 10% Secured Convertible Debentures as Initial Tranche of

$12 Million Offering and Entry into $50 Million Equity Line of Credit Agreement - Convertible Offerings & Notes Filed:

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down After The Close:

- Movers Up: AMBA +18.2%, VLN +7.8%, IREN +7.1%, URBN +6.5%, EVLV +6.4%, NTNX +2.3%, YXT +2.2% of note.

- Movers Down: DDD -11.5%, DELL -10.9%, WDAY -10.8%, GES -10.1%, ADSK -9.1%, HPQ -7.9%, LSAK -4.8%, POET -4%, CRWD -3.7% of note.

News After The Close:,

- Akamai Tech (AKAM) announces that the U.S. Bankruptcy Court for the District of Delaware has approved its bid to acquire select assets from Edgio. Will be accretive.

- Super Micro Computer (SMCI) prepaid in full and terminated obligations under loan agreements with Bank of America.

- RYCEY awarded $695 mln U.S. Navy contract.

- RTX awarded $591 mln U.S. Navy contract.

- GD to compete for each order of a $499 mln U.S. Army contract for mortar propelling charges.

- B. Riley Financial (RILY) expects to return to a normal filing cadence in 2025.

- 10-K “Delays – None of note.

Buybacks or Repurchases:

- ICFI approves increase to its repurchase program, authorizing up to $300 mln for buybacks

Exchange/Listing/Company Reorg and Personnel News:

- MSEX names Gregory Sorensen as its COO, effective December 16.

- YXT announces that Teng Zu has resigned from his position as the CEO due to personal reasons, effective today; he will remain with the Company as a director and the vice chairman of the Board.

- ADSK appoints Janesh Moorjani as its CFO, effective December 16; replaces Elizabeth Rafael who had been serving as interim CFO since May 31.

Dividends Announcements or News:

- Stocks Ex Div Today: HD TMUS NEM EA L EG TTEK CHRD BRFS PVH CATY CCS ENR FLNG ADEA PAHC

- Stocks Ex Div Tomorrow:

- NOG declares $0.42 quarterly cash dividend and anticipates increasing the next quarterly dividend to $0.45/share

What’s Happening This Morning: Futures S&P 500 -4.25, NASDAQ -37.50, Dow Jones +24 and Russell 2000 +19.59. Europe is lower. Asia is higher ex Japan. Bonds are at 4.262% from 4.359% for the 10-Year. Crude Oil and Brent are higher with Natural Gas lower. Gold, Silver and Copper are higher. The U.S. Dollar is lower versus the Euro, lower versus the Pound and lower against the Yen. Bitcoin is at $93,558 from $98,140 yesterday morning higher by +$2322 with futures up +2.54% this morning.

- Daily Positive Sectors: Utilities, Communication Services, Consumer Defensive, Healthcare and Technology of note.

- Daily Negative Sectors: Energy, Technology and Utilities of note.

- One Month Winners: Financials, Consumer Cyclicals, Energy, Industrials and Communication Services and of note.

- Three Month Winners: Consumer Cyclicals, Financials, Industrials, Utilities, Technology and Communication Services of note.

- Six Month Winners: Financials, Real Estate, Utilities, Consumer Cyclical and Technology of note.

- Twelve Month Winners: Financials, Technology, Industrials, Utilities and Communication Services note.

- Year to Date Winners: Technology, Financials, Utilities, Communication Services and Industrials of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Wednesday After the Close: None of note

- Friday Before The Open: None of note

Notable Earnings of Note This Morning:

- Beats: None of note.

- Misses: FRO -0.04 of note.

- Still to Report:

Company Earnings Guidance:

- Positive Guidance: AMBA of note.

- Negative or Mixed Guidance: DELL GES of note.

Advance/Decline Daily Update: The A/D Line hit a wall last Tuesday and rolled over having broken its monthly moving average but has now broken out to new highs.

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: AMBA +25%, URBN +11.3%, VLN +8.9%, IREN +6.8%, NTNX +6.5%, BGNE +5%, ARWR +4%, EVLV +3.2%, MMS +2.6%, BTSG +2.1%

- Gap Down: DDD -13.8%, DELL -12.3%, GES -11.9%, WDAY -10.1%, HPQ -8.8%, ADSK -7.5%, FRO -6.6%, POET -6.5%, CRWD -6.3%, FISI -5.7%, MSEX -3.2%, EXEL -2

Insider Action: No names see Insider buying with dumb short selling. No names see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Lead Story on Bloomberg: Trump Picks Key Economic, Trade Posts. (Bloomberg)

- 5 Things To Know Before The Market Opens. (CNBC)

- Stocks Making The Biggest Moves: DELL MSTR URBN. (CNBC)

- Market Wrap: Stocks slip with Trump picks and upcoming data due this morning. (Bloomberg)

- Mortgage Applications increased by 6.3% this week when they were released at 7:00 a.m. EDT.

- Bloomberg: The Big Take – Adani bribery charges are rocking India. (Podcast)

Economic:

- October Personal Income is due out at 8:30 a.m. EDT and expected to remain at 0.03%.

- October PCE Core is due out at 8:30 a.m. EDT and expected to stay at 0.03%.

- October Durable Orders are due out at the same time and expected to rise to 0.4% from -0.08%.

- Q3 GDP is also due out at 8:30 a.m. EDT and is expected to stay at 2.80%.

- Weekly Jobless Claims are due out at 8:30 a.m. EDT.

- October Pending Home Sales are due out at 10:00 a.m. EDT and expected to fall to -1.50% from 7.40%.

- Weekly Crude Oil Inventories are due out at 10:30 a.m. EDT.

- Weekly Natural Gas Inventories are due out at 12:00 p.m. EDT.

Geopolitical:

- No Federal Reserve speakers of note today.

- FOMC Minutes are due out at 2:00 p.m. EDT.

- President Biden and the First Lady are in Nantucket for Thanksgiving hanging at the home of David Rubenstein, founder of Carlyle Group.

- Watch our Twitter feed, Bullet86, for an impromptu appearances.

M&A Activity and News:

- None of note.

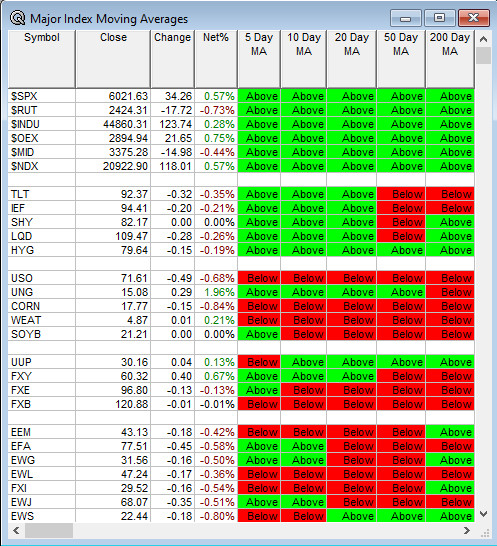

Moving Averages On Major Equity Indexes: Remains 100%. Bonds have improved this week.

Meeting & Conferences of Note:

-

- Sellside Conferences:

- Bernstein’s The Premium Review Conference

- Goldman Sachs Energy Clean Tech & Utilities Conference

- Goldman Sachs India Corporate Conference

- Needham Growth Conference

- Sellside Conferences:

-

- Fireside Chat: None of note.

- Top Analyst, Investor Meetings: None of note.

- Shareholder Meetings: ATNM, BNGO

- Update: None of note.

- R&D Day: None of note.

- FDA Presentation:

- Company Event: None of note.

- Industry Meetings or Events:

- LA Auto Show

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Upgrades: URBN EMBC DKS

Downgrades: