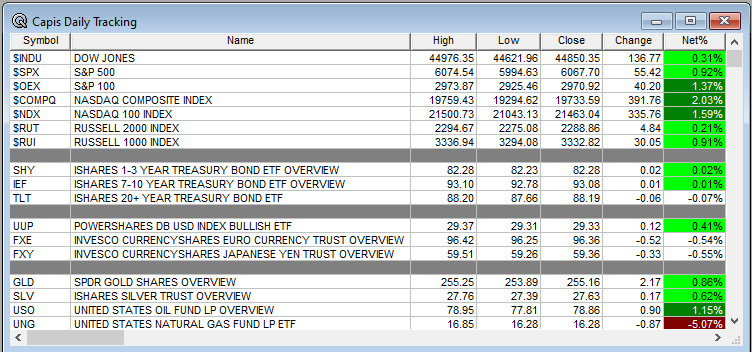

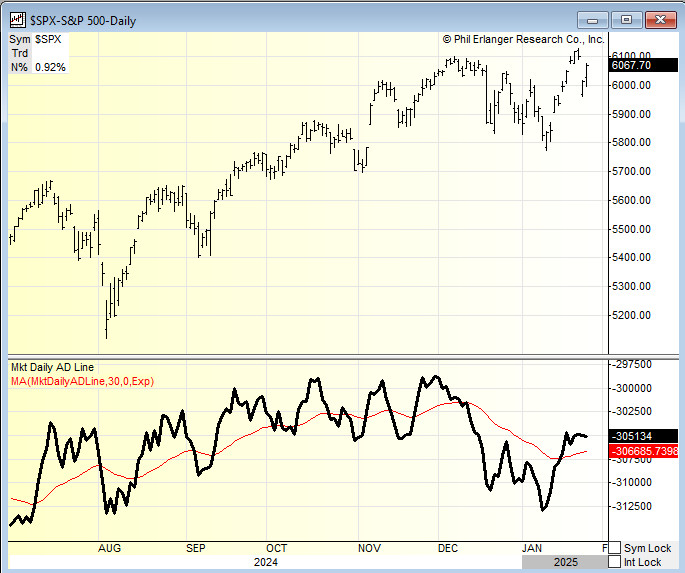

Overnight Summary & Early Morning Trading: The S&P 500 finished Tuesday higher by 0.92% at 6067.70. Monday lower by -1.46% at -88.96. The overnight high was hit at 6111.50 at 1:00 a.m. EDT and the low was hit at 6086.50 at 6:55 p.m. EDT. The overnight range is 25 points. The current price is higher at 7:05 a.m by +0.10% at 6103 up +6 points.

Executive Summary: The S&P 500 has now fallen by -1% or more on three days this month with Monday being the third down day of more than -1%. So we are clustering with multiple -1% losses. With three trading days left in the month and a Federal Reserve Open Market Committee Meeting conclusion today, expect the unexpected.

Articles of Note: Must read on who is behind Deepseek. “Deepseek Chief’s Journey From Math Geek To Global Disruptor.” (WSJ)

*Note that certain articles highlighted may require a subscription. We highlight noted sources like the WSJ or Bloomberg that have wide audiences.

Key Events of Note Today:

-

- Several economic indicators out today

- 7 Year Note Auction at 1:00 p.m. EDT and there is a 2 Yr FRN Note Auction at 11:30 a.m. EDT.

Daily Chart Request: Want to see an Erlanger Chart in The Morning Note? Simply send an email to us at [email protected] and we will more than likely show it.

Hilton Grand Vacations (HGV) is a new Type 1 Short Squeeze. Other hotel stocks are also heavily shorted including H, MAR and WH.

Notable Earnings Out After The Close

- Beats: RNR +1.01, CB +0.58, FFIV +0.48, NXT +0.45, QRVO +0.40, UMBF +0.23, SYK +0.14, ASH +0.11, MANH +0.11, TRMK +0.09, SBUX +0.02 of note.

- Flat: TRNS, ELS and ARE of note.

- Misses: PFS -0.13, VBTX -0.10, PKG -0.06, LFUS -0.02, LC -0.01, BXP -0.01 of note.

- IPOs For The Week: BBNX, FBGL, INR, RCT

- New IPOs/SPACs launched/News:

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced:

- TGL: FORM S-3 – Up to 90,000,000 Shares of Common Stock

- Notes Priced:

- CCL Pricing of $2.0 Billion 6.125% Senior Unsecured Notes Offering for Refinancing and Interest

Expense Reduction

- CCL Pricing of $2.0 Billion 6.125% Senior Unsecured Notes Offering for Refinancing and Interest

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders of note:

- VRME: FORM S-3 – 1,461,896 Shares of Common Stock Offered by the Selling Stockholder

- Mixed Shelf Offerings:

- GM files mixed shelf securities offering.

- PIPE:

- Convertible Offerings & Notes Filed:

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down Yesterday:

- Movers Up: FFIV +14.4%, NXT +13.6%, UMBF +3.6%, LRN +3.4%, RNST +3.3%, of note.

- Movers Down: MANH -23.6%, LC -21.1%, QRVO -4.8%, PKG -4.5%, BXP -3.6%, LFUS -3.1% of note.

News After The Close:

- Commerce Secretary nominee Howard Lutnick will testify to Senate tomorrow at 10:30 ET.

- VALE reports FY24 Iron ore production reached 328 Mt, the highest since 2019, surpassing the original guidance of 310-320 Mt.

- Point72 Asset Management’s founder Steven Cohen believes the outlook for artificial intelligence is more favorable after DeepSeek. (Reuters)

- KSS ticking higher after cutting 10% of its corporate workforce. (WSJ)

- 10K or Qs Delays – none of note.

Exchange/Listing/Company Reorg and Personnel News:

- LCID appoints Taoufiq Boussaid as Chief Financial Officer, planned to become effective February 25, 2025.

- FND appoints Bradley Paulsen as President, effective April 28.

- SYK announces that Glenn S. Boehnlein will retire from his role as Vice President, Chief Financial Officer.

- SMPL announces retirement of CFO Shaun Mara, effective July 3, Christopher Bealer who will join on April 1 to replace Mara as CFO.

- CLX CFO Kevin Jacobsen to retire effective April 1, Luc Bellet to succeed Kevin and they will work together on an orderly transition.

- NTAP names Wissam Jabre as CFO, effective March 10, 2025.

Buybacks:

- BDX authorizes up to 10 mln in additional share repurchases.

Dividends Announcements or News:

- Stocks Ex Div Today: LEN CLX ENTG QGEN AM CALM GBX PSEC MCBS

- Stocks Ex Div Tomorrow: MMC VLO AZZ

- SPGI increases quarterly cash dividend 5.5% to $0.96/share from $0.91/share.

- HAFC increases quarterly cash dividend 8% to $0.27/share from $0.25/share.

- NOG increases quarterly cash dividend to $0.45/share from $0.42/share.

- SF increases quarterly cash dividend 10% to $0.46/share from $0.42/share.

What’s Happening This Morning: (as of 8:15 a.m. EDT) Futures S&P 500 -14, NASDAQ -4, Dow Jones -50 and Russell 2000 -1. Europe is higher with Asia higher as well. Bonds are at 4.522% from 4.569% on the 10-Year. Crude Oil and Brent are lower with Natural Gas lower. Gold higher with Silver and Copper lower. The U.S. Dollar is higher versus the Euro, higher against the Pound and lower against the Yen. Bitcoin is at $102,185 from $102, 811 higher by $+474 up 0.44%. Additional Comments: The S&P 500 has now reversed the breakthrough its December high one trading day later and and is now below 6100. Can 6000 hold?

- Daily Positive Sectors: Technology, Communication Services and Consumer Cyclicals were higher.

- Daily Negative Sectors: Consumer Defensive, Real Estate, Utilities, Materials and Industrials and were lower.

- One Month Winners: None of note.

- Three Month Winners: Communication Services, Consumer Cyclical, Financials and Technology of note.

- Six Month Winners: Consumer Cyclical, Financials, Communication Services, Utilities and Industrials of note.

- Twelve Month Winners: Technology, Communication Services, Financials, Consumer Cyclical and Utilities note.

- Year to Date Winners: Energy, Healthcare, Communication Services, Materials, Utilities, Industrials and Technology of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Wednesday After the Close:

- Thursday Before The Open:

Notable Earnings of Note This Morning:

- Beats: LII +1.34, EAT +0.94, GPI+0.91, SMG +0.34, TMUS +0.28, SF +0.26, VIRT +0.25, MSCI +0.22, AIT +0.18, HES +0.14, GD +0.08, ADP +0.06, EXTR +0.03, PB +0.03, GLW +.01, NDAQ +0.01 of note.

- Flat: None of note.

- Misses: NAVI -0.46, EXP -0.32, ASML -0.16, MHO -0.12, MNRO -0.10, DHR -0.02 of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: EAT LOGI NXT of note.

- Negative or Mixed Guidance: BXP MANH SBUX of note.

Advance/Decline Daily Update: The A/D fell to major support, bounced, made new lows and now is starting to stabilize.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: NXT +22.8%, FFIV +14.7%, AZUL +9.7%, FNA +8.8%, CGEM +8.1%, ASML +6.9%, ASH +5.4%, LOGI +4.4%, SYNA +4%, AHH +3.7%, ASPN +3.5%, LRN +2.8%, HAFC +2.7%, TRMK +2.7%, CLMT +2.6%, SEDG +2.3%, SONY +2.2%, FSLR +2% of note.

- Gap Down: LC -22.7%, MANH -22.4%, VBTX -6.1%, CLBK -5.8%, QRVO -5%, PKG -4.7%, DHX -3.1%, AXL -2.6%, MRVI -2.5%, ZBH -2.5%, DHR -2.4%, OTIS -2.3%, SMPL -2.1%, BXP -2% of note.

Insider Action: None see Insider buying with dumb short selling. None see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Lead Story on Bloomberg: Microsoft Probing To See If DeepSeek Related Group Improperly Obtained OpenAI Data. (Bloomberg)

- Market Wrap: NASDAQ Futures rise as Tech rebounds ahead of Fed. (Bloomberg)

- Stocks Making The Biggest Moves: yet to post, check back. (CNBC)

- ASML seeks low price AI models driving chip demand. (CNBC)

- Trump offers buyouts to get rid of Federal employees. (Bloomberg)

- Frontier proposes merging with Spirit again. (CNBC)

- Weekly Mortgage Applications fell -2.0%.

- Bloomberg Big Take: Freeland’s Vision for Canada. (Podcast)

Economic:

- Weekly Crude Oil Inventories are out at 10:30 a.m. EDT.

Geopolitical: (Watch our Twitter feed, Bullet86, for any impromptu appearances)

- President Trump’s Daily Schedule. Nothing up yet and Trump is back at the White House.

- Federal Reserve speakers are in the blackout period through today’s close.

- The Latest FOMC Rate Decision is due out at 2:00 p.m. EDT followed by a press conference at 2:30 p.m. EDT.

M&A Activity and News:

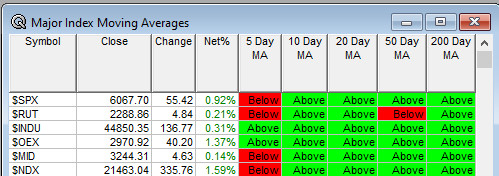

Moving Average Table: Drops from 70% to 83%.

Meeting & Conferences of Note:

-

- Sellside Conferences:

-

- Shareholder Meetings: CFFN, J, VVV

- Top Analyst, Investor Meetings: KLYG, PALI, PHIO, ZNTL

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation:

- AZN: Data Presentation on Datopotamab deruxtecan

- CGTX: Data Presentation on CT1812 Jan 29-31

- ZNTL: Data Presentation on Azenosertib

- PFE: Data Presentation on ZNc3-006

- Industry Meetings or Events:

- DealFlow’s Atlantic City Microcap Conf

- International Production & Processing Expo

- Microcap Conference

- Society of Thoracic Surgeons

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

- Upgrades: WNEB LPRO VZ T

- Downgrades: TS

-