Overnight Summary & Early Morning Trading: The S&P 500 finished Monday higher by 0.16% at 5836.22. Friday was lower by -1.54% at 5827.04. The overnight high was hit at 5913.50 at 3:45 a.m. EDT and the low was hit at 5875.50 at 4:05 p.m. EDT. The overnight range is 38 points. The current price is higher at 8:20 a.m by 0.17% up by +10 at 5913.

Executive Summary: Stocks got hit hard into the open on Monday but recovered by the end of the day. Could the low be in for now? It appears that way as futures are higher this morning and the “Wolf Moon” was full last night. Kind of a joke but the reality is there is a loose connection to corrective action and full moons. A great read!! See articles of note.

Articles of Note: “Are Investors Moonstruck? Lunar Phases and Stock Returns” by Kathy Yuan, Lu Zheng and Qiaoqiao Zhu (University of Michigan)

*Note that certain articles highlighted may require a subscription. We highlight noted sources like the WSJ or Bloomberg that have wide audiences.

Key Events of Note Today:

-

- is out at 3:00 p.m. EDT. Details in Economic Section.

- There is a 3 & 6 Month Bill Auction at 11:30 a.m. EDT.

Daily Chart Request: Want to see an Erlanger Chart in The Morning Note? Simply send an email to us at [email protected] and we will more than likely show it.

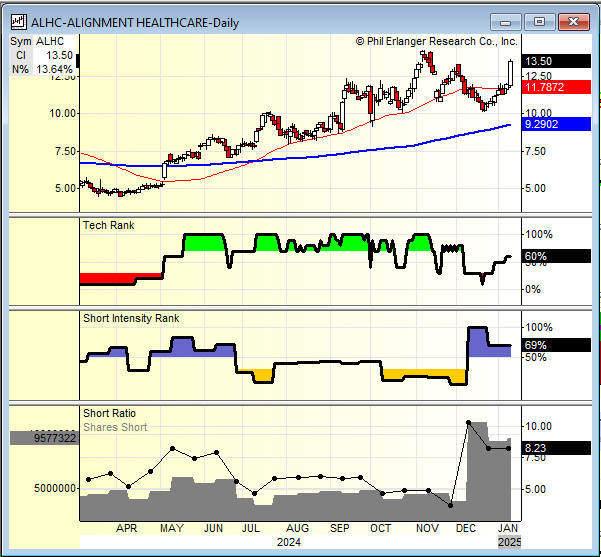

Alignment Healthcare (ALHC) is a Short Squeeze as it rose 13.60% yesterday. The shorts have been increasing their bet the last two months. Note the Technical Rank has improved to 60% and the Erlanger Short Intensity is 69% with an Erlanger Short Ratio of 8.23. Yesterday the company announced strong membership growth. (GlobeNewswire)

Notable Earnings Out After The Close

- Beats: KBH +0.08 of note.

- Flat: None of note.

- Misses: None of note.

- IPOs For The Week: ALEH, CRGT, DGNX, DXST, FBGL, SKBL,

SLGB, ZYBT - New IPOs/SPACs launched/News: None of note.

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced:

- CNTM: FORM S-1 – Up to 51,666,622 Shares of Common Stock

- CTNT: FORM S-3 – 469,484 Shares of Class A Common Stock

- LMFA: Form S-3.. Up to 3,472,740 Shares of Common Stock

- Notes Priced: CCL Repricing of Senior Secured First Lien Term Loan B Facilities as Part of Ongoing Interest

Expense Reduction - Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders of note:

- CCCS files for 26,035,603 shares of common stock offering by selling shareholders.

- Mixed Shelf Offerings:

- ADBE files mixed shelf securities offering.

- PIPE:

- Convertible Offerings & Notes Filed:

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down After The Close:

- Movers Up: ANGI +14.1%, INGN +11.3%, KBH +8.1%, ZENV +5.4%, INSG +4.6%, DRS +4.3%, AB +3.2%, AMRC +2% of note.

- Movers Down: AEHR -11.8%, CCCS -4.8%, DOV -2.8%, SANW -2.1% of note.

News After The Close:

- AB announces that preliminary assets under management decreased to $792 billion during December 2024 from $813 billion at the end of November.

- IVZ reports month-end assets under management (AUM) of $1,846.0 billion, a decrease of 0.6% versus previous month-end.

- DHR issues Q4 revenue guidance; expects low-single digit percent growth yr/yr.

- IAC (IAC) approves plan to spin off full stake in Angi (ANGI) in a tax-free transaction.

- ICFI awarded a new $40 mln contract by The U.S. Department of Homeland Security Center for Countering Human Trafficking.

- Robinhood (HOOD) to pay $45 mln for violating over 10 securities law provisions. (SEC Release)

- AMRC awarded $183 mln project to modernize U.S. General Services Administration’s campus infrastructure with cost-saving measures.

- Porttillo’s (PTLO) provides guidance in slides; sees 2025 revenue growth of 11-12%, same restaurant sales of flat to +2%, adjusted EIBTDA growth of 6-8%.

- Barrick (GOLD) suspends operations in Mali after $245 million in gold is seized. (Reuters)

- Copa Holdings’ (CPA) capacity (ASMs) increased by 6.5%, while system-wide passenger traffic (RPMs) increased by 6.8%, compared to 2024.

- Donald Trump’s incoming economic team discussing gradual 2-5% a month tariff hikes. (Bloomberg)

- AAPL revamped app developer fees trigger scrutiny from EU antitrust regulators. (Bloomberg)

- 10K or Qs Delays – NEOG (Q)

Exchange/Listing/Company Reorg and Personnel News:

- YUM promotes Scott Mezvinsky to KFC Division Chief Executive Officer, effective March 1.

- SLDP COO Derek Johnson to resign, effective February 1.

- BXC announces resignation of CFO Andrew Wamser, effective Jan 24; Kimberly DeBrock to serve as interim CFO as Co commences a search for successor.

- BurTech Acquisition Corp. and BurTech Acquisition Corp. announce closing of business combination; combined co to trading on Nasdaq under the ticker symbols “BZAI” and “BZAIW” on January 14 .

Buybacks:

Dividends Announcements or News:

- Stocks Ex Div Today: GEHC DGX AFG OZK HTLF VTMX AIV

- Stocks Ex Div Tuesday: ABBV ABT PNC FCX MAA PECO ACA MSM TRN BKE GTX CHCO WGO ARR

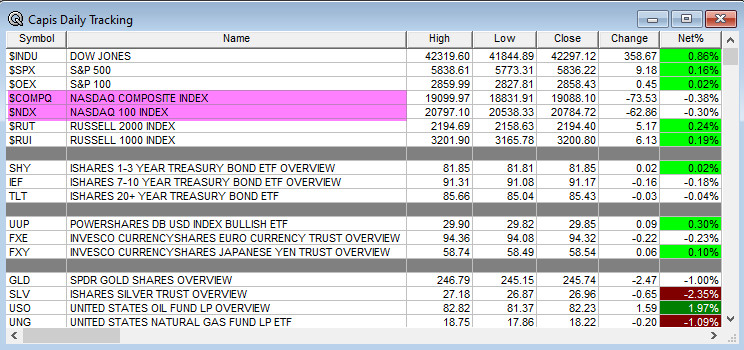

What’s Happening This Morning: (as of 8:10 a.m. EDT) Futures S&P 500 +17 , NASDAQ +73 , Dow Jones +123 and Russell 2000 +8.30 . Europe is higher ex FTSE with Asia higher ex Japan. Bonds are at 4.792% from 4.766% on the 10-Year. Crude Oil and Brent are lower with Natural Gas lower as well. Gold, Silver and Copper higher. The U.S. Dollar is lower versus the Euro, higher against the Pound and higher against the Yen. Bitcoin is at $96,035 from $90,752 higher by $3146 up 3.39%. Additional Comments: NASDAQ Indexes did not participate (highlighted in Magenta).

- Daily Positive Sectors: Materials, Energy, Real Estate, Industrials and Healthcare was higher on Friday.

- Daily Negative Sectors: Technology, Utilities, Communication Services and Consumer Defensive were lower.

- One Month Winners: None of note.

- Three Month Winners: Communication Services, Consumer Cyclical, Financials and Technology of note.

- Six Month Winners: Consumer Cyclical, Financials, Communication Services, Utilities and Industrials of note.

- Twelve Month Winners: Technology, Communication Services, Financials, Consumer Cyclical and Utilities note.

- Year to Date Winners: Energy, Healthcare, Communication Services, Materials, Utilities, Industrials and Technology of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Tuesday After the Close:

- Wednesday Before The Open:

Notable Earnings of Note This Morning:

- Beats: None of note.

- Flat: None of note.

- Misses: None of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative or Mixed Guidance: None of note.

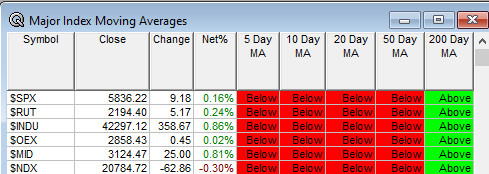

Advance/Decline Daily Update: The A/D fell to major support, bounced and is now making new lows. Not the direction we want this to go if long stocks.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: RGNX +16.7%, RILY +16.2%, ANGI +10.3%, KIDS +10%, INGN +9.9%, KBH +9.8%, ZENV +9.2%, TDOC +8.2%, IVZ +5.1%, AMRC +4.4%, SLDP +3.5%, AB +3.4%, HCM +3.4%, HHH +2.6%, SANW +2.4%, MMSI +2.2%of note.

- Gap Down: AEHR -18.8%, BTG -5.6%, DRS -3%, TTAN -3%, INSG -2.3% of note.

Insider Action: None see Insider buying with dumb short selling. None see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Lead Story on Bloomberg: Trump Team Studies Gradual Tariff Increases. (Bloomberg)

- Market Wrap: Wall Street set for higher open on tariff modifications. (Bloomberg)

- Stocks Making The Biggest Moves: KBH TDOC SIG APLD. (CNBC)

- Los Angeles braces for more winds today. (Bloomberg)

- Southwest Airlines (LUV) pauses corporate hiring and summer internships. (CNBC)

- Barron’s + on GOOGL QCOM MU and – GEO

- Bloomberg Big Take: Time runs short for TikTok. (Podcast)

Economic:

- December NFIB Small Business Optimism is due out at 6:00 a.m. EDT and came in at 105.10 from 101.70.

- December PPI is due out at 8:30 a.m. EDT and is expected to come in at 0.3% from 0.40% in November.

- Weekly API Crude Oil is out at 4:30 p.m. EDT.

Geopolitical: (Watch our Twitter feed, Bullet86, for any impromptu appearances)

- President Biden receives the President’s Daily Brief at 10:00 a.m. EDT.

- President Biden delivers remarks about conservation at 5:30 p.m. EDT.

- Federal Reserve Kansas City President Jeffrey Schmid speaks at 10:00 a.m. EDT.

- Federal Reserve New York President John Williams speaks at 3:00 p.m. EDT.

M&A Activity and News:

- .

Moving Average Table: Remains at 20%.

Meeting & Conferences of Note:

-

- Sellside Conferences:

- CJS ‘New Ideas for the New Year’ Investor Conference

- Goldman Sachs Financial Technology Conference

- JP Morgan Healthcare Conference

- Jefferies CCS Conference

- Needham Growth Conference

- TD Securities Annual Global Mining Conference

- UBS Winter Infrastructure & Energy/Utilities Conference

- Top Analyst, Investor Meetings: BRCC, VRNT

- Sellside Conferences:

-

- Shareholder Meetings: CRKN, GATO, LEXX, UNF

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation:

- Company Event: None of note.

- Industry Meetings or Events:

- Biotech Showcase

- ICR Conference

- LifeSci Partners Corporate Access Event

- Lytham Partners Investor Healthcare Summit

- North American International Auto Show in Detroit

- SIC Biotech Symposium

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

- Upgrades: V PCAR OLN MCRI HSAI FI EMN DVN CE CART

- Downgrades: SHO ORGN CHH CHGG BTG BCE ADM

-