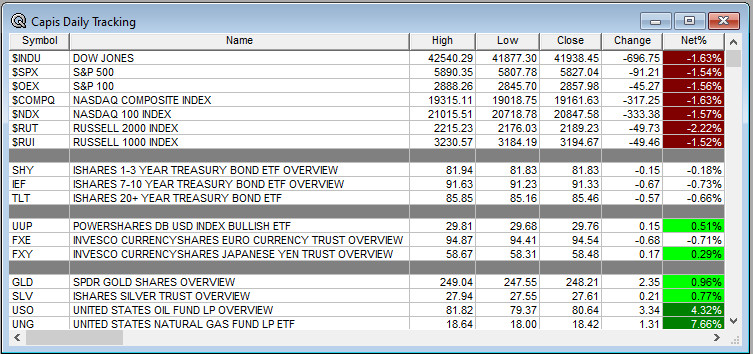

Overnight Summary & Early Morning Trading: The S&P 500 Friday lower by -1.54% at 5827.04. Wednesday higher by 0.16% at 5918.25. The overnight high was hit at 58675.75 at 6:30 p.m. EDT and the low was hit at 5809 at 4:00 a.m. EDT. The overnight range is 59 points. The current price is lower at 7:10 a.m by -0.86% down by -50.50 at 5815.75.

Executive Summary: ADP Payrolls came in at 256,000 against estimates of 155,000 jobs last Friday. That was not what the Federal Reserve wanted to getting inflation lower. Now instead rates climbed to 4.77%. The latest Short Interest is out and NYSE rose 01.9% while NASDAQ rose 2.67%. Stocks are getting hit hard again into the open today.

Articles of Note: “Doubting America Can Cost You A Lot of Money.” by John Authers (Bloomberg)

*Note that certain articles highlighted may require a subscription. We highlight noted sources like the WSJ or Bloomberg that have wide audiences.

Key Events of Note Today:

-

- Monthly Treasury Budget is out at 3:00 p.m. EDT. Details in Economic Section.

- There is a 3 & 6 Month Bill Auction at 11:30 a.m. EDT.

Daily Chart Request: Want to see an Erlanger Chart in The Morning Note? Simply send an email to us at [email protected] and we will more than likely show it.

Academy Sports And Outdoors (ASO) is a Short Squeeze with our updated short interest data over the weekend. The shorts have been increasing their bet the last two months. Note the Technical Rank has improved to 100% and the Erlanger Short Intensity is 88% with an Erlanger Short Ratio of 6.07.

Notable Earnings Out After The Close

- Beats: WDFC +0.11 of note.

- Flat: None of note.

- Misses: None of note.

- IPOs For The Week: ALEH, CRGT, DGNX, DXST, FBGL, SKBL,

SLGB, ZYBT - New IPOs/SPACs launched/News: None of note.

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced:

- Notes Priced:

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders of note:

- Mixed Shelf Offerings:

- BNED files $100 mln mixed shelf securities offering.

- SMG files mixed shelf securities offering.

- DKL files $50 mln mixed shelf securities offering.

- BLKB files mixed shelf securities offering.

- FTEL files $150 mln mixed shelf securities offering.

- PIPE:

- Convertible Offerings & Notes Filed:

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down Last Week:

- Movers Up: ANGO (12.28 +35.24%), ITCI (94.55 +12.93%), FTAI (174.60 +15.34%), DAL (66.80 +13.22%), UAL (107.01 +11.85%), CPRI (23.74 +17.06%), SNX (133.82 +13.47%), ADTN (10.13 +12%), SUPV (19.09 +11.77%), FRO (17.28 +21.23%), DHT (10.72 +14.6%), CRK (19.94 +12.78%), STNG (54.64 +11.83%) of note.

- Movers Down: RDUS (10.97 -25.22%), QURE (13.93 -22.35%), OMER (8.85 -21.05%), APLS (27.51 -17.8%), KURA (7.21 -17.47%), APOG (51.04 -29.01%), MCY (47.35 -27.97%), STZ (182.85 -17.61%), EIX (65.24 -18.25%) of note.

News After The Close:

- Franklin Resources (BEN) reports preliminary month-end assets under management (AUM) of $1.58 trillion at December 31, 2024, compared to $1.65 trillion at November 30, 2024.

- JWN reports holiday season comp growth of +5.8%; raises FY25 sales and comp growth outlook, reiterates profitability guidance.

- Kohl’s (KSS) will close its San Bernardino E-commerce Fulfillment Center (EFC) when the lease on that facility expires in May 2025, as well as 27 underperforming stores by April 2025.

- DAL cancels approximately 700 Delta and Delta Connection flights for Jan. 10 due to weather conditions across the Southeast.

- GCO reports same store sales increased 6% on quarter-to-date basis, and comparable e-Commerce sales grew 20%.

- OXY provides summary of earnings considerations that could impact results for Q4. (SEC Filing)

- U.S. proposes a 4.3% increase to Medicare Advantage plan payments, $21 bln boost to insurers for Medicare payments. (Bloomberg)

- BOOT guides Q3 earnings and revs above consensus, sees comps of approximately +8.6%.

- 10K or Qs Delays – NEOG (Q)

Exchange/Listing/Company Reorg and Personnel News:

- HSY announces that Chairman, President, and CEO Michele Buck will retire in June 30, 2026; The Board has appointed a special committee to direct the search for the Company’s next CEO.

- ATKR appoints John Pregenzer as COO; retains Role as president-electrical.

- PLAB appointed George Macricostas to the position of Executive Chairman, effective January 6, 2025.

Buybacks:

Dividends Announcements or News:

- Stocks Ex Div Today: ING HRL GNL UVV SCVL

- Stocks Ex Div Tuesday: GEHC DGX AFG OZK HTLF VTMX AIV

What’s Happening This Morning: (as of 8:10 a.m. EDT) Futures S&P 500 -39, NASDAQ -196, Dow Jones -66 and Russell 2000 -25.23 . Europe is lower with Asia lower as well. Bonds are at 4.766% from 4.698% on the 10-Year. Crude Oil and Brent are higher with Natural Gas higher as well. Gold, Silver and Copper lower. The U.S. Dollar is higher versus the Euro, higher against the Pound and lower against the Yen. Bitcoin is at $90,752 from $94, 841 lower by $-4025 down -4.33%.

- Daily Positive Sectors: Energy was higher on Friday.

- Daily Negative Sectors: Financials, Real Estate, Technology and Consumer Defensive were lower.

- One Month Winners: None of note.

- Three Month Winners: Communication Services, Consumer Cyclical, Financials and Technology of note.

- Six Month Winners: Consumer Cyclical, Financials, Communication Services, Utilities and Industrials of note.

- Twelve Month Winners: Technology, Communication Services, Financials, Consumer Cyclical and Utilities note.

- Year to Date Winners: Energy, Healthcare, Communication Services, Materials, Utilities, Industrials and Technology of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Monday After the Close:

- Tuesday Before The Open:

Notable Earnings of Note This Morning:

- Beats: None of note.

- Flat: None of note.

- Misses: None of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative or Mixed Guidance: None of note.

Advance/Decline Daily Update: The A/D fell to major support, bounced and is now making new lows. Not the direction we want this to go if long stocks.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: SAGE +38.4%, ITCI +35.6%, MOLN +24%, ENFN +13.2%, CLRB +9.1%, ARQT +6.1%, TXG +5.9%, LULU +5.8%, WDFC +5.3%, FOLD +5.3%, HUM +5.2%, BOOT +3.8%, CRBU +3.7%, CVS +3.5%, FTEL +3.2%, UNH +2.9%, BPMC +2.9%, NTRA +2.6%, RARE +2.5%, EXAS +2.2%, MD +2.1%, AKA +2.1%, CSTL +2% of note.

- Gap Down: EWCZ -17%, MREO -9.9%, RXST -5.8%, NEOG -4.8%, ASND -3.6%, GCO -2.7%, SWTX -2.3% of note.

Insider Action: LFCR and FBK see Insider buying with dumb short selling. None see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Lead Story on Bloomberg: Los Angles Fires Rage As High Winds Set To Return This Week. (Bloomberg)

- Market Wrap: Stock traders jolted by fresh rise of Treasury yields. (Bloomberg)

- Stocks Making The Biggest Moves: Not reported yet, check back. (CNBC)

- Moderna (MRNA) lower on drop of revenue guidance. (Reuters)

- Pershing Square offers to take over Howard Hughes for $85 a share in a move to be the next Berkshire Hathaway. (CNBC)

- AWS (AMZN) and General Catalyst partner to speed up development of healthcare AI tools. (CNBC)

- Barron’s + on FSLR CRWD ASIX UNTY UCTT SSNC VST with +/- STZ BUD TAP BFB

- Bloomberg Big Take: Global Bond Tantrum Is Wrenching and Worrisome Start To The Year. (Podcast)

Economic:

- December Treasury Budget is due out at 2:00 p.m. EDT and came in last month at $-367 billion.

- Due out this week besides weekly data – Treasury Budget, NFIB Small Business Optimism Index, PPI, CPI, Empire State Manufacturing Index, Retail Sales, Philadelphia Fed Index, Import/Export Prices, NAHB Housing Index, Housing Starts and Industrial Production.

Geopolitical: (Watch our Twitter feed, Bullet86, for any impromptu appearances)

- Press Briefing at 1:30 p.m. EDT with Press Secretary Karine Jean-Pierre.

- President Biden delivers a foreign policy address at the State Department at 2:00 p.m. EDT.

- President Biden meets with Senior White House and Administration officials to discuss the Californian wildfires at 5:15 p.m. EDT.

- No Federal Reserve speakers of note.

M&A Activity and News:

- JNJ to buy Intra-Cellular (ITCI) for $14.6 billion. (CNBC)

Moving Average Table: Moves from 36% positive to 20%.

Meeting & Conferences of Note:

-

- Sellside Conferences:

- Seaport Research Partners Second Annual Steel & Metals Conference

- Benchmark Event at ICR

- Goldman Sachs Financial Technology Conference

- ICR Conference

- JP Morgan Healthcare Conference

- Needham Growth Conference

- UBS Winter Infrastructure & Energy Conference

- Top Analyst, Investor Meetings: OCUL

- Sellside Conferences:

-

- Shareholder Meetings: LFWD, NVVE, VTAK

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation: AVXL: Data Presentation on ANAVEX 2-73

- Company Event: None of note.

- Industry Meetings or Events:

- Biotech Showcase

- Lytham Partners Investor Healthcare Summit

- North American International Auto Show in Detroit

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

- Upgrades: KTOS RRC OVY KLAC ITUB GPOR CART BBD AEP

- Downgrades: DH

-