Overnight Summary and Early Morning Trading:

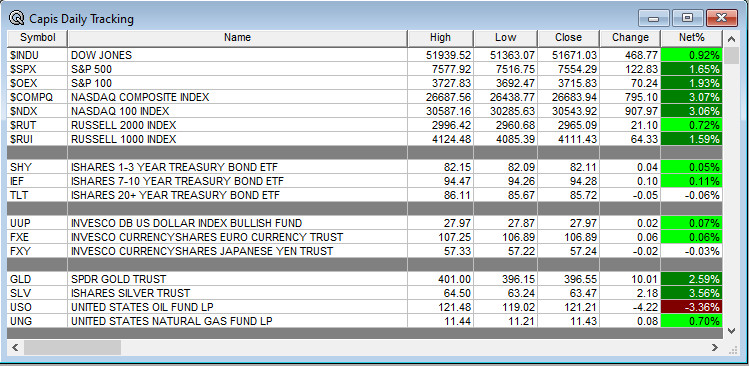

- The S&P 500 finished Monday higher by 1.65% at 7554.29 from Friday higher by 0.50% at 7431.46.

- The S&P 500 sees support now at 7500 from 7400. Resistance is now at 7600 from 7500. In the last two months, support has moved from 6300 to 7500

- S&P 500 hit its 25th All-Time Closing High of 2026 on Tuesday, 6/2.

- Futures are flat this morning at 0.00 (+0.00%) at 7626.75 on the SP 500 at 6:50 a.m. EDT.

- Bond Market is higher today on price with the 10-Year Yield at 4.439% from 4.441%.

Executive Summary:

- Stocks started a new week winning streak, with the S&P 500 gaining 0.65% in the last week. We are now up 6.50% since the peak in January on the S&P 500 as of last Friday’s close.

- U.S. moves into Week 17 of its attack on Iran. Is the ceasefire and a conclusion to the war going to really happen this week or just another week of kicking the can down the road?

Key Geopolitical Events of Note:

- Economic news of note.

- Weekly – API Petroleum Institute Report of note.

- Monthly – Housing Starts, ADP Employment Report and Import/Export Prices of note.

- Fed Speakers of Note today: Blackout period.

- 20-Year Bond Auction at 1:00 p.m. EDT.

- President Trump’s schedule:

- Executive Time at 2:00 a.m. EDT. (8:00 a.m. Local Time)

- Participates in a working session with G-7 leaders at 3:00 a.m. (9:00 a.m. Local Time)

- Participates in a Bilateral Meeting with the Emir of the State of Qatar at 4:30 a.m. (10:30 a.m. Local Time)

- Participates in a Bilateral Meeting with the President of the UAE at 5:15 a.m. (11:16 a.m. Local Time)

- Participates in a Working Lunch with the G-7 Leaders and the Middle East at 6:00 a.m. (12:00 p.m. Local Time)

- Participates in a Bilateral Meeting with the G-7 Leaders and the Development Countries at 9:00 a.m. (3:00 p.m. Local Time)

- Participates in a Cultural Performance and Concert at 1:15 p.m. (7:15 p.m. Local Time)

- Participates in a G7 Leaders’ Social Dinner 2:15 p.m. (8:15 p.m. Local Time)

Notable Earnings Out After The Close:

- Beats: None

- Misses: PLAY -0.38 of note.

- Flat: None of note: None.

Capital Raises of Note/Pricings:

- IPO Filings: None of note.

- Secondaries Filed Or Priced:

- CVBF authorizes the repurchase of up to 15.0 mln shares of company’s common stock

- HRDN files for 28,719,000 share common stock offering.

- Notes Filed Or Priced: None of note.

- Convertible Offerings Filed or Priced:

- NN announces redemption of 5.00% senior secured convertible notes.

- ADPT announces proposed convertible senior notes offering.

- NEO announces it has commenced a private offering of $275 mln aggregate principal amount of convertible senior notes due 2032.

- Private Placement:

- Direct Offering: None of note

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders:

- NTHI files for 555,554 share common stock offering by selling stockholder

- HRDN also files for 57,432,395 share common stock offering by selling securityholders

- Mixed Shelf Offerings:

- SU files mixed securities shelf offering

After The Close:

- Hewlett Packard Enterprise (HPE) is collaborating with leading companies — Intel (INTC), IQM, Qblox, Quantinuum (QNT), QuEra Computing, Quantum Machines, Rigetti (RGTI), and Riverlane — across a diverse set of architectural approaches with the goal of building out a full-stack hybrid quantum supercomputing platform. These collaborations will support the development of integrated testbeds for hybrid algorithm co-design, software interoperability, and system-level performance benchmarking across HPC and AI environments.

- Applied Materials (AMAT) unveils deposition and selective etch systems to advance 3D chip scaling.

- Qualcomm (QCOM) in discussions to expand AI chip capabilities with potential Tenstorrent acquisition.

- DELL awarded $1.4 bln Air Force call order for the Microsoft Enterprise License Agreement renewal.

Monday After the Close Winners:

- HITI +18.2%,

Monday After The Close Losers:

- PLAY -9.5%, ADPT -7.2%, NEO -5.4%, MAC -4%, SFIX -3.5%,

Executive, Corporate Changes:

- SFIX appoints Sree Sreedhararaj as Chief Product and Technology Officer.

- KSS announces that Elliott Rodgers has been named Chief Operating Officer; He will assume the role on September 9, 2026.

- IPI names Jason Tremblay as CFO.

- MDLZ announces appointment of Amit Banati as Executive Vice President and Chief Financial Officer, effective July 1, 2026.

- LOVE announces it has appointed Andrew Farag as the Company’s Executive Vice President, Chief Financial Officer and Treasurer, effective immediately.

- NEM Brian Tabolt has been appointed Chief Financial Officer, Mark Rodgers has been appointed Chief Operating Officer, and David Thornton has been appointed Chief Technical Officer.

Dividend Calendar:

- Top Names Ex-Dividend Tuesday: of note.

- Top Names Ex-Dividend Wednesday: None of note.

- SSRM reinstates of regular quarterly dividend; Anticipates declaring the first quarterly cash dividend of $0.03/share in conjunction with 2Q26 results.

Buybacks:

- ENSG announces that its Board of Directors has approved a $60 mln increase to the Company’s previously approved $40 mln stock repurchase program.

- MAC commences public offering of 14.0 mln shares of common stock in connection with forward sale agreement with each of Goldman Sachs or its affiliates, and one or more other financial institutions.

- SSRM approves an additional $500 mln for share repurchases.

What Happening This Morning:

Futures S&P 500 +2.50, NASDAQ 100 +81.25 Dow Jones +32. Europe is higher while Asia is mixed. Bond yield is at 4.443% from 4.441% on the 10-Year. Crude Oil and Brent Crude are lower with Natural Gas higher. Gold and Silver are higher with Copper lower. The U.S. Dollar is lower versus the Euro, lower against the Pound and lower against the Yen. Bitcoin is at $66,391 from $66,554.

Sector Action:

- Daily Positive Sectors: Industrials, Technology, Communication Services and Materials were the leaders.

- Daily Negative Sectors: Energy, Real Estate, Consumer Defensive and Healthcare led the way lower.

- One Month Winners: Technology, Communication Services, Consumer Defensive, Healthcare and Real Estate of note.

- Three-Month Winners: Energy, Materials, Utilities, Consumer Defensive and Industrials of note.

- Six-Month Winners: Energy, Materials, Utilities, Industrials, Healthcare and Consumer Defensive of note.

- Twelve-Month Winners: Materials, Energy, Industrials, Utilities, Communication Services and Technology of note.

- Year to Date Winners: Energy, Materials, Consumer Defensive, Utilities and Industrials of note.

Bolded means the Sector is new to the period in which it falls.

Upcoming Earnings Of Note: (Erlanger Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Today After the Close: LZB of note

- Monday Before The Open: JBL KMX of note

Notable Earnings of Note This Morning:

- Beat: None of note.

- Missed: None of note.

- Flat: None of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: After The Close & This Morning – None of note.

- Mixed – None of none.

- Negative or Mixed Guidance: After The Close & This Morning – None of note.

Advance/Decline Daily Update: Market Breadth ended its move higher for now.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: HITI +15.1%, SHMD +8.3%, QCOM +4.2%, NTHI +4.2%, VMI +3.8%, VZLA +3.3%, SSRM +2.8%, CLNE +2.7%, HOOD +2.6%, PSN +2.5%, BLDP +2.4%, HSDT +2.3%, ARI +2.2%, RMIX +2% of note

- Gap Down: PLAY -14.8%, DOMO -9.5%, HUN -9.4%, ALVO -8%, ADPT -7.4%, J -3.7%, MAC -3.3% of note.

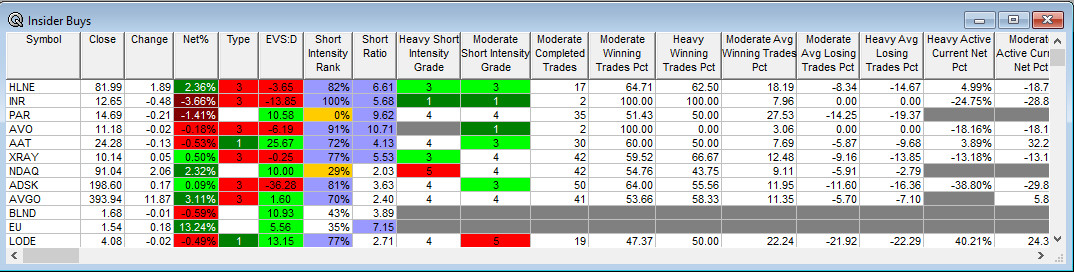

Insider Action: HLNE INR AAT XRAY ADSK AVGO LODE sees Insider Buying with dumb short selling. None see Insider Buying with smart short sellers. Above $100,000 in purchases with high shorts but no history: AVO of note.

Other Trading Action: None of note.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific. Bolded source means paywall.

- WSJ Lead Story: SpaceX to Buy Cursor for $60 Billion. (WSJ)

- NY Times Lead Story: War in Iran Has Permanently Altered the Global Economy. (NYT)

- USA Today:. How Old Maintain The Grip on Power and Politics. (USA Today)

- Bloomberg: Warsh Wants Less Fed Talk. (Bloomberg)

- Market Wrap: Stocks drift after three day rally. (Bloomberg)

Economic & Geopolitical:

- Federal Reserve Speakers of note today:

- Federal Reserve Black Out Period & FOMC starts Day 1 of its two day meeting.

- President Trump’s schedule for today:

- Executive Time at 2:00 a.m. EDT. (8:00 a.m. Local Time)

- Participates in a working session with G-7 leaders at 3:00 a.m. (9:00 a.m. Local Time)

- Participates in a Bilateral Meeting with the Emir of the State of Qatar at 4:30 a.m. (10:30 a.m. Local Time)

- Participates in a Bilateral Meeting with the President of the UAE at 5:15 a.m. (11:16 a.m. Local Time)

- Participates in a Working Lunch with the G-7 Leaders and the Middle East at 6:00 a.m. (12:00 p.m. Local Time)

- Participates in a Bilateral Meeting with the G-7 Leaders and the Development Countries at 9:00 a.m. (3:00 p.m. Local Time)

- Participates in a Cultural Performance and Concert at 1:15 p.m. (7:15 p.m. Local Time)

- Participates in a G7 Leaders’ Social Dinner 2:15 p.m. (8:15 p.m. Local Time)

- Economic Data Out –

- Weekly

- API Petroleum Institute Data out at 4:30 p.m. EDT.

- Monthly

- May Housing Starts are due out at 8:30 a.m. EDT and expected to fall to 1,440,000 from 1,465,000.

- May Import/Export Prices are due out at 8:30 a.m. EDT and came in last month at 1.90% and 3.30%.

- May ADP Employment Report at 8:15 a.m. EDT.

- Weekly

M&A Activity & Daily: None of note.

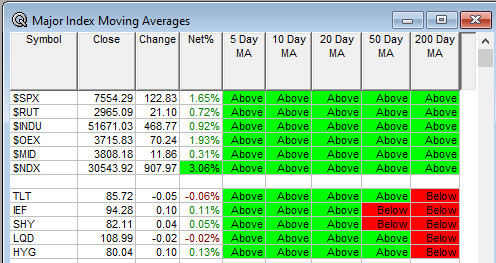

Moving Average Table: 100% from 76% of Equities are Positive, and 72% from 58% Bonds are Positive.

Meeting & Conferences of Note:

- Sellside Conferences:

- BAC Commodity Research Conference

- BAC Transforming World Conference

- Benchmark Quantum Computing Summit

- BTIG Infectious Disease Day

- H.C. Wainwright Neuro Perspectives Expert Summit

- Jefferies Consumer Conference

- Singular Research Invitational Conference

- Stifel Summer Solstice Conference

- Truist Industrials & Services Conference

- UBS Cape Cod Healthcare Summit

- Wolfe Materials of the Future Conference

- Top Analyst, Investor: HPE NEXN PETV SAIL VMI of note.

- Shareholder Meetings: COIN DLTR FIVE MA MET PENN SLM TWLO WDAY XYZ of note.

- Fireside Chat: None of note.

- FDA Presentation: None of note.

- R&D Day: None of note.

- Meetings:

- Databricks Data + AI Summit

- HP Enterprise Discover

- Planet MicroCap

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Upgrades: DT GTE KRC XOM of note.

Downgrades: HPP SKT of note.