Overnight Summary: The SP 500 closed Monday higher by 0.87% at 5010.60 from Friday lower by -0.88% at 4967.23 . The overnight high was hit at 5,059 at 4:25 a.m. while the overnight low was hit at 5037.50 at 7:15 p.m. EDT. The range overnight is 22 points as of 6:25 a.m. EDT. Currently, the S&P 500 is higher by +7.5 points at 6:25 a.m. EDT.

- Beats: MEDP +0.73, RLI +0.29, AMP +0.19, CR +0.09, RBB +0.09, CADE +0.08, BRO +0.07, HSTM +0.06, CDNS +0.04, PHG +0.04, HXL +0.03, ARE +0.02, CALX +0.01, of note.

- Flat: None of note.

- Misses: AGNC -1.69, WAFD -0.23, NUE -0.21, SAP -0.17, SSD -0.15, CLF -0.04, GL -0.01 of note.

Capital Raises:

- IPOs Priced or News:

- New SPACs launched/News:

- Secondaries Priced:

- Notes Priced of note:

- Common Stock filings/Notes:

- BHVN: Closing of Public Offering and Full Exercise of the Underwriters’ Option to Purchase Additional Shares.

- BNZI: Filed Form S-1.. Common Stock Warrants.

- DRIO: Filed Form S-3.. 15,727,223 shares of common stock.

- PXS: See Mixed Shelf.

- SERV: Closing of $40 Million Public Offering and Uplisting to the Nasdaq Capital Market Under New Ticker “SERV“.

- TTOO: Filed Form S-1 .. Common Stock and Warrants.

- Direct Offering:

- Exchangeable Subordinate Voting Shares:

- Selling Shareholders of note:

- Private Placement of Public Entity (PIPE):

- INTZ: Private Placement Subscription Agreement.

- Mixed Shelf Offerings:

- AWH: Filed Form S-3.. $100,000,000.00 Mixed Shelf.

- JAGX: Filed Form S-3.. $75,000,000 Mixed Shelf.

- PXS: Filed Form F-3.. $100 Million Mixed Shelf and 4,425,134 Shares of Common Stock.

- VANI: Filed Form S-3.. $300,000,000.00 Mixed Shelf.

- Debt/Credit Filing and Notes:

- Tender Offer:

- Convertible Offering & Notes Filed:

- VERX announces private offering of $250 million of convertible senior notes.

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close :

- After Hours Movers:

- ACET +7.6%, SAP +2.7%, CPRI +2.7%, LIND +2.5%.

- CALX -15%, SSD -8.7%, CDNS -7.4%, NUE -6.5%, PKG -5.2%, CLF -2.7%.

- News Items After the Close:

- Boeing (BA) sees slower 787 jet rate production as wrestles with supply shortage.

- Grupo Aeroportuario Del Sureste (ASR) report Q1 revenues up 15.3% year over year. Passenger traffic up 3.9%.

- FTC sues Tapestry (TPR) to prevent the acquisition of Capri (CPRI).

- Exchange/Listing/Company Reorg and Personnel News:

- ADM CFO Vikram Luthar to resign, effective September 30th.

- Buyback Announcements or News:

- Stock Splits or News:

- Dividends Announcements or News:

- ETH ups quarterly dividend by 8.33% to $0.39 from $0.36%.

- AMP ups dividend to $1.48 from $1.35 share.

What’s Happening This Morning: Futures value reflects the change with fair value.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

- Daily Positive Sectors: Financial, Technology and Utilities of note.

- Daily Negative Sectors: Materials of note.

- One Month Winners: Energy and Utilities of note.

- Three Month Winners: Energy, Basic Materials, Industrials, and Financial of note.

- Six Month Winners: Financials, Industrials, Technology and Communication Services of note.

- Twelve Month Winners: Communication Services, Technology, Industrials, and Financial of note.

- Year to Date Winners: Communication Services, Energy, Financials, Industrials, and Technology of note.

Stocks jumped on Monday, bouncing back after last week’s dismal performance. The S&P 500 gained 0.9%, ending a six-day streak of losses, with each of the benchmark index’s 11 sectors finishing the day in the green. The tech-heavy Nasdaq Composite advanced 1.1% after falling 5.5% last week. The blue-chip Dow Jones Industrial Average added 0.7%, or about 254 points. Easing tensions between Israel and Iran helped restore some market confidence. Brent crude oil slipped 0.3% to $87 a barrel, and gold futures slid 2.8% after reaching an all-time high on Friday. (WSJ – Edited by QPI)

Upcoming Earnings Of Note:

- Tuesday After the Close:

- Wednesday Before the Open:

Earnings of Note This Morning:

- Beats: PHM +0.74, LMT +0.51. GM +0.49, R +0.43, KMB +0.38, DHR +0.20, PII +0.18, DGX +0.18, GE +0.17, UPS +0.13, RTX +0.11, JBLU +0.09, PEP +0.09, PM +0.09, MSCI +0.05, FCX +0.05, PNR +0.04, HAL +0.02 of note.

- Flat: None of note.

- Misses: BPOP -0.45, XRX -0.29, LKQ -0.13, IVZ -0.07, SHW -0.05 of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: GM, NVS of note.

- Negative Guidance: PKG, CDNS, CALX, JBLU, PM, of note.

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: IBRX +28.1%, HIBB +18.6%, CANG +12.7%, ACET +10.8%, SPOT +7.6%, DHR +6.7%, LIND +6.6%, NVS +5.2%, CR +4.8%, SAP +3.8%, ARE +2.8%, UPS +2.6%, AJG +2.2%, GL +2.2%, RBB +2.1%, NGNE +2%, BGNE +2% of note.

- Gap Down: ABEO -46.6%, CALX -16.9%, SSL -8.1%, SSD -6.8%, NUE -6.6%, CDNS -5.5%, PKG -5.2%, VERX -2.5%, CLF -2.4%, PII -2.3% of note.

Insider Action: SNDA see Insider buying with dumb short selling. BRT sees Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- 5 Things To Know Before the Stock Market Opens Today. (CNBC)

- What You Need To Know To Start Your Day. (Bloomberg)

- Bloomberg Lead Story: Love That Strong Dollar But It May Not Last. (Bloomberg)

- U.S. Stocks rise with earnings center stage: Markets Wrap. (Bloomberg)

- Bloomberg: Daybreak Podcast: Apple’s China iPhone Sales drop -19%. (Podcast)

- Halliburton (HAL) sees best profits in 12 years. (Bloomberg)

- Pepsi (PEP) sees international demand boost sales. (CNBC)

- United Healthcare (UNH) paid ransom to hackers in Change Healthcare hack. (CNBC)

- JetBlue (JBLU) lowers outlook for 2024 and shares fall. (CNBC)

- Bloomberg: The Big Take: Looks at Gucci and its leader Francois-Henri Pinault. (Podcast)

- Marketplace: Humane’s new AI Pin does not live up to hype. (Podcast)

- NY Times Daily: Looks at the trial of former President Donald J. Trump. (Podcast)

- Wealthion: Auto secrets. (Podcast)

- Adam Taggart’s Thoughtful Money: Asset Price Volatility Is Suddenly Higher Than Markets Are Prepared For | Kevin Muir (Podcast)

Moving Average Update: Score gets a heartbeat improving to 31% from 23%.

Geopolitical:

- President’s Public Schedule:

- President Biden receives the Daily Briefing at 10:00 a.m. EDT.

- President Biden heads to Tampa for a campaign event at 3:00 p.m. EDT.

- President Biden returns to the White House at 7:30 p.m. EDT.

Economic:

- March New Home Sales are due out at 10:00 a.m. EDT and are expected to rise to 670,000 from 662,000.

Federal Reserve / Treasury Speakers:

- No Fed Speakers as in Blackout Period due to next week’s FOMC meeting.

M&A Activity and News:

- None of note.

Meeting & Conferences of Note:

- Sellside Conferences:

- None of note.

- Top Shareholder Meetings: AEP, BLMN, BKH, CHTR, CMA, FFIN, ITUB, WDS

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: BANL, LAZR

- Update: None of note.

- R&D Day: None of note.

- Company Event:

- Industry Meetings:

- CEM Scottsdale Capital Event

- Cholangiocarcinoma Foundation Conference

- Society for Healthcare Epidemiology of America Conference

- Society for Industrial and Organizational Psychology Conference

- Spinal Cord Injury Investor Symposium

- World Congress Experience

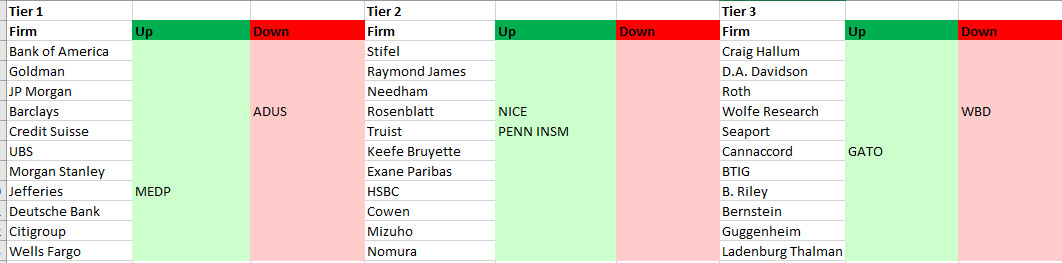

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades: