Overnight Summary & Early Morning Trading:

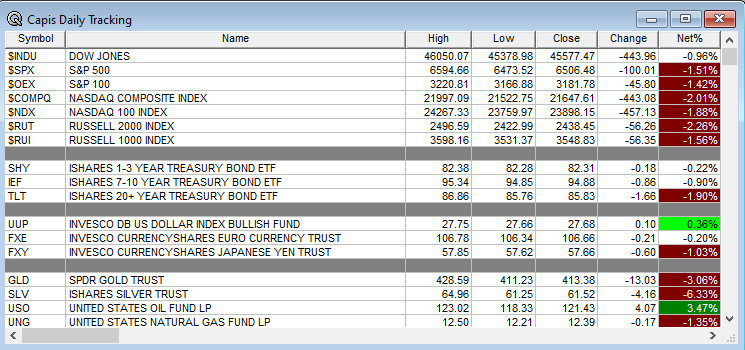

- The S&P 500 finished Friday lower by -1.51% at 6506.48 from Thursday lower by -0.27% at 6606.49.

- The S&P 500 sees support now at 6500 from 6600. Resistance is now at 6600 from 6700.

- S&P 500 hit its fourth All-Time Closing High of 2026 on 1/27/26. It has been over one month since a new all-time high.

- Year to date the S&P 500 is -4.95% from -3.49% on Friday’s close.

- Futures are higher this morning by +155 (2.47%) at 6718 on the SP 500 around 7:45 a.m. EDT.

- Bond Market is lower today on price with the 10-Year Yield at 4.435% from 4.30%.

Executive Summary:

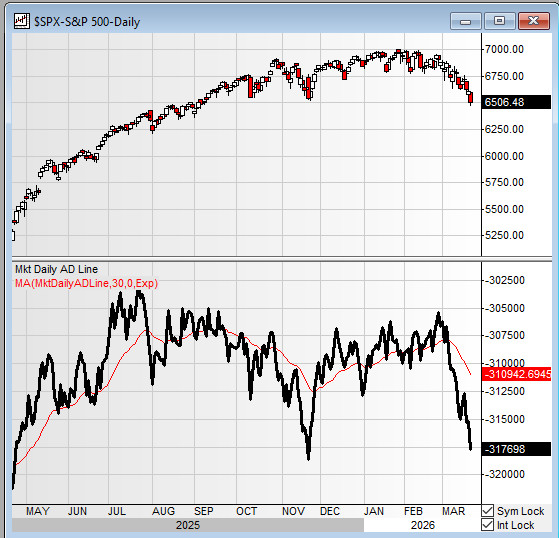

- Stocks has lost -3.12% in the last three weeks and -6.76% since the peak in January on the S&P 500. We are not out of the “Danger Zone”.

- U.S. moves into Week Four of its attack on Iran. Key to this week is the conflict not getting to “the point of no return” where chaos takes over.

- The S&P 500 is now clustering with multiple (4) drops of greater than -1%.

- Futures were ugly until President Trump said that U.S. and Iran were talking over the weekend and he was extending the deadline for Iran to open the Strait of Hormuz from tonight to Friday. Trump negotiating strategy continues to negotiate at the brink. Futures are all over the place.

Key Events of Note Today:

- Economic news of note is still delayed due to the government shutdown but we will be producing what is scheduled to be reported.

- Weekly – None of note.

- Monthly – Construction Spending out at 10:00 a.m. EDT.

- 3 & 6 Month Bill Auction at 11:30 a.m. EDT.

- Fed Speakers of Note today: Now out of the blackout period.

- President Trump’s schedule:

- Participates in Executive Time at 8:00 a.m. EDT.

- Heads to Memphis to participate in the Memphis Safe Task Force Roundtable at 1:00 p.m. EDT.

- Heads to Washington D.C. in the late afternoon.

Notable Earnings Out After The Close:

- Beats: None of note.

- Misses: None of note.

- Flat: None of note.

Capital Raises:

- IPOs For The Week: None of note.

- New IPOs/SPACs launched/News: None of note.

- IPOs Filed/Priced: None of note.

- Secondaries Filed Or Priced:

- GNLX: Form 8K – entered into a Sales Agreement

- NUCL: Form S-1.. Primary Offering of Up to 23,422,133 shares of Common Stock Upon the Exercise of Warrants Up to 5,940,000 shares of Common Stock Upon Conversion of Series A Cumulative Convertible Preferred Stock Secondary Offering of Up to 30,059,408 shares of Common Stock Up to 11,922,133 Warrants

- SABS – Closing of $85 Million Public Offering of Common Stock and Pre-Funded Warrants

- SATL: FORM S-3 – $200,000,000 Aggregate Amount of Shares of Class A Common Stock

- SLDB: Form S-3.. 1,316,899 SHARES

- SLDB: Form S-3.. 42,780,739 SHARES

- UMAC – Proposed Public Offering

- Notes Filed Or Priced: None of note.

- Convertible Offerings Filed or Priced: None of note.

- Private Placement: None of note.

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders:

- FLOC – Pricing of Public Offering by Selling Stockholders

- NVGS – Commencement of Secondary Public Offering by Selling Shareholder and Concurrent Repurchase of Shares by Navigator Gas

- Private Placements: None of note.

- Mixed Shelf Offerings:

- ALMS: Form S-3ASR Mixed Shelf

- ASMB: Form S-3.. $400,000,000 Mixed Shelf

- CODA: FORM S-3 – $100,000,000 Mixed Shelf Offering – Up to 500,000 Shares of Common Stock

- DHT: FORM F-3ASR – Mixed Shelf Offering

- DRIO: Form S-3.. $100,000,000 Mixed Shelf

- WPP: Form F-3ASR Mixed Shelf

News After The Close:

- Softbank preparing $500 bln data center in Ohio.

- Bristol Myers Squib (BMY) transforms the classical Hodgkin Lymphoma Treatment Paradigm with expanded U.S. and EMA approvals for Opdivo® (nivolumab).

- Goodyear Tire (GT) announces restructuring actions in EMEA, includes overall net reduction of 400 positions.

- Vita Coco Company (COCO) will replace TEGNA (TGNA) in the S&P SmallCap 600 effective prior to the opening of trading on Wednesday, March 25.

- President Trump said US was considering winding down Iran military campaign.

- AVAV awarded a $117.3 mln US Army contract for P550 Long Range Reconnaissance systems.

- 10K or 10Q Delays – None of note.

Buybacks:

Executive, Corporate Changes:

- NUS announces CFO James Thomas has stepped down to pursue an outside opportunity; Chelsea Lantz has been named interim CFO, effective immediately.

- FUBO discloses that its Board approved a 1-for-12 reverse stock split.

- KRG promotes Heath Fear to President and Chief Financial Officer.

- RGA CIO Mark Brooks to resign effective April 3, 2026.

- SMCI announces resignation of board member Yih-Shyan “Wally” Liaw.

- PNR David Jones, Chair of the Board, to retire; T. Michael Glenn named as next Chair.

- GBLI names Evan Kasowitz as COO.

Dividends Announcements or News:

- Top Names Ex-Dividend Today: APH ITUB POR OTF BRKR DX BBU LTC NVGS (not including SPDR ETFs)

- Top Names Ex-Dividend Tuesday:

- ELE declares first dividend of US$0.03 per share.

What’s Happening This Morning: (as of 7:30 a.m. EDT)

- Futures S&P 500 +164, NASDAQ 100 +584, Dow Jones +1169. Europe is higher while Asia is lower. Bond yield is at 4.368% from 4.297% on the 10-Year. Crude Oil and Brent Crude are lower with Natural Gas lower. Gold and Silver are lower Copper is higher. The U.S. Dollar is lower versus the Euro, lower against the Pound and lower against the Yen. Bitcoin is at $70,350 higher by +2024 higher by +2.96% from $70,777 higher by 0.62% up $436.

Sector Action:

- Daily Positive Sectors: None were higher.

- Daily Negative Sectors: All others were lower. Biggest losses include Utilities, Real Estate, Materials and Technology.

- One Month Winners: Energy and Utilities of note.

- Three-Month Winners: Energy, Materials, Utilities, Consumer Defensive and Industrials of note.

- Six-Month Winners: Materials, Healthcare, Utilities, Consumer Defensive and Industrials of note.

- Twelve-Month Winners: Materials, Energy, Industrials, Communication Services and Technology of note.

- Year to Date Winners: Energy, Materials, Consumer Defensive, Utilities and Real Estate of note.

Bolded means the Sector is new to the period in which it falls.

Upcoming Earnings Of Note: (Erlanger Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Today After the Close: None of note.

- Tuesday Before The Open:

Notable Earnings of Note This Morning:

- Beat: None of note.

- Missed: None of note.

- Flat: of note.

- Still to Report: of note.

Company Earnings Guidance:

- Positive Guidance: After The Close & This Morning – None of note.

- Mixed – None of note.

- Negative or Mixed Guidance: After The Close & This Morning – None of note.

Advance/Decline Daily Update:

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- GapUp: APGE +18.1%, PPHC +5.8%, COCO +2.1% of note.

- GapDown: FUBO -6.2%, MUX -5.5%, EVO -5.3%, UEC -4.9%, ALMU -4.7%, STM -4.6%, SMCI -4.5%, PRTA -4%, NBIS -3.9%, ELE -3.6%, PHG -3.4%, ALAB -2.7%, USGO -2.7%, GSK -2.2%, VCTR -2% of note.

Insider Action: CRM GO sees Insider Buying with dumb short selling. None sees Insider Buying with smart short sellers. Above $100,000 in purchases with high shorts but no history: AFCG of note.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- WSJ Lead Story: Trump Says Military Will Postpone Further Strikes on Iranian Energy Infrastructure. (WSJ)

- Bloomberg Lead: Trump Postpones Strikes on Iran Energy Targets. (Bloomberg)

- NY Times Business Section Lead Story: Trump Says U.S. and Iran Held “Very Good” Talks On Ending Conflict. (NYT)

- USA Today: Air Canada Pilot killed when passenger jet hit a vehicle at LaGuardia Airport. (USA Today)

- Thoughtful Money: (Podcast)

- The Big Take: The Market Just Broke a Critical Support Level. (Podcast)

Economic & Geopolitical:

- Federal Reserve Speakers of note today: None of note.

- President Trump’s schedule for today:

- Participates in Executive Time at 8:00 a.m. EDT.

- Heads to Memphis to participate in the Memphis Safe Task Force Roundtable at 1:00 p.m. EDT.

- Heads to Washington D.C. in the late afternoon.

- Economic Data Out –

- Weekly

- None of note.

- Monthly

- January Construction Spending will be released at 10:00 a.m. EDT and is expected to fall to 0.1% from 0.3%.

- Weekly

M&A Activity & Daily Changes: None of note.

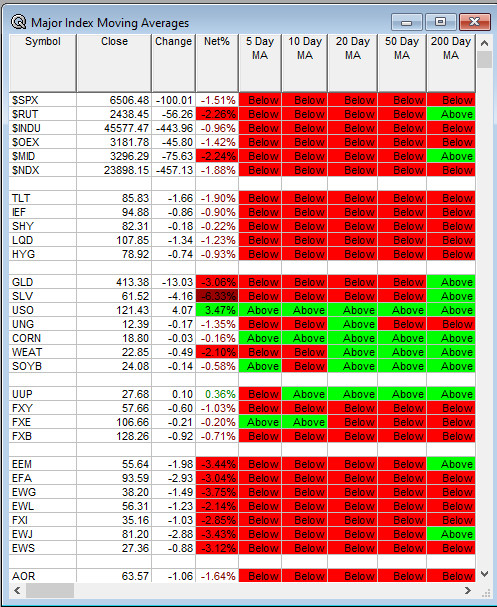

Moving Average Table: 7% from 13% of Equities are Positive, and 0% from 12% Bonds are Positive.

Meeting & Conferences of Note:

- Sellside Conferences:

- Jefferies Auto Aftermarket Conference

- Wolfe Badishkanian Small Group March Conference

- Top Analyst, Investor: GWH KZIA TAC TLPH of note.

- Shareholder Meetings: NRXP of note.

- Fireside Chat: None of note.

- FDA Presentation: None of note.

- R&D Day: None of note.

- Meetings:

- CERAWeek

- International Battery Seminar and Exhibit

- Society of Toxicology Meeting

- USCAP

- XPONENTIAL Europe

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

- Upgrades: AVAH KNOP VVV of note.

- Downgrades: SMCI of note.