Overnight Summary & Early Morning Trading:

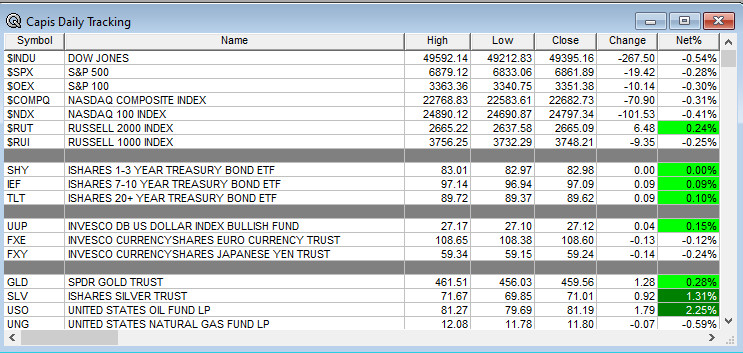

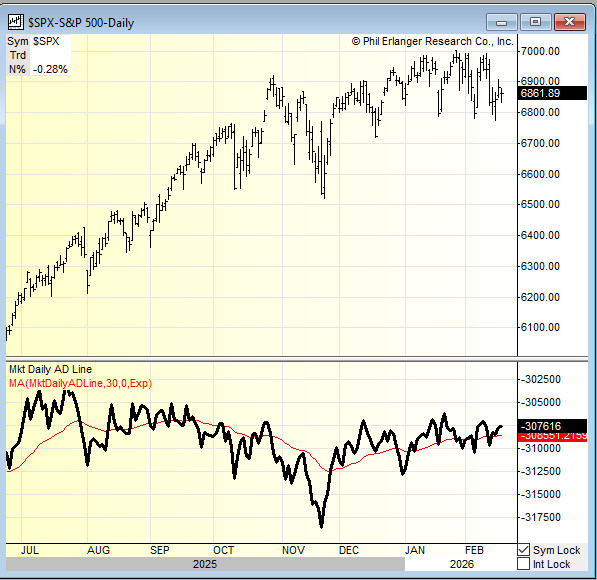

- The S&P 500 finished Thursday lower by -0.28% at 6861.89 from Wednesday higher by 0.56% at 6881.31.

- The S&P 500 sees support now at 6800 from 6900. Resistance is now at 6900 from 7000.

- S&P 500 hit its fourth All-Time Closing High of 2026 on 1/27/26.

- Year to date the S&P 500 is higher by 0.24% from 0.52% on Friday’s close.

- Futures are lower this morning by -1.25 (-0.04%) at 6875.75 on the SP 500 around 6:00 a.m. EST.

- Bond Market is higher today on price with the 10-Year Yield at 4.073% from 4.096%.

Executive Summary:

- Stocks were lower last week by -1.39% on the S&P 500. So far this week the S&P 500 is higher by 0.38%. We are not out of the “Danger Zone”.

- Bitcoin is still below $70,000 from 2/5.

- Crude moves back below $70 so that was a brief pop above $70.

- US increases Middle East Air Power to highest level since 2003 Iraq Invasion. Action coming on Iraq?

Key Events of Note Today:

- Economic news of note is still delayed due to the government shutdown but we will be producing what is scheduled to be reported.

- Weekly – Baker Hughes Rig Count

- Monthly – Personal Income, PCE Core, Q4 GDP, New Home Sales and University of Michigan Consumer Sentiment.

- Fed Speakers of Note today: Bostic at 9:45 a.m. EST, Logan at 1:15 p.m. EST, Musalem at 3:30 a.m. EST,

- President Trump’s schedule:

- Participates in a Working Breakfast with Governors at 9:30 a.m. EST.

- Participates in a Private Meeting at 10:30 a.m. EST

- 30 Year TIPS Auction at 1:00 p.m. EST.

Notable Earnings Out After The Close: (Beats > $0.05 AND <$-0.05)

- Beats: VAL+9.80, FIX +2.62, VIC +0.57, NEM +0.47, GH +0.27, ICUI +0.22, IRTC +0.16, OLED +0.11, WK +0.09, AKAM, +0.08, ALRM +0.08, TNDM +0.08 of note.

- Misses: PTCT -1.77, HHH -1.26, OPEN -1.15, TXRH -0.22, WKC -0.17, FNF -0.08, SEM -0.07, RIG -0.06 of note.

- Flat: None of note.

Capital Raises:

- IPOs For The Week: None of note.

- New IPOs/SPACs launched/News: None of note.

- IPOs Filed/Priced: None of note.

- Secondaries Filed Or Priced:

- AGIG – Pricing of $20 Million Registered Direct Offering of Common Stock

- BHAT – Pricing of US$6.4 Million Public Offering

- CADL – Proposed $100 Million Public Offering

- JFBR: Form F-3.. Up to 1,372,017 Ordinary Shares

- TLSI Proposes Public Offering

- WPC – Closing of Public Offering of Common Stock

- Notes Filed Or Priced:

- MCO: Form S-3ASR Debt Securities

- VRT: Form S-3ASR – Debt Securities

- Convertible Offerings Filed or Priced: None of note.

- Private Placement: None of note.

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- None of note.Selling Shareholders: None of note.

- Private Placements: None of note.

- Mixed Shelf Offerings:

- EBAY: FORM S-3ASR – Mixed Shelf Offering

- ENGN: Form S-3.. US$400,000,000 Mixed Shelf

- PLSE: FORM S-3 – $200,000,000 Mixed Shelf Offering

- POST: FORM S-3ASR – Mixed Shelf Offering

- SYRE: FORM S-3 – Mixed Shelf

- WTTR: FORM S-3ASR – Mixed Shelf Offering

News After The Close:

- Akamai (AKAM) beat but lowered on guidance down -9%.

- Texas Roadhouse (TXRH) sees commodity inflation continues to pressure restaurant margins.

- BA awarded a $270 mln Defense Logistics Agency contract.

Exchange/Listing/Company Reorg and Personnel News:

Buybacks:

Dividends Announcements or News:

- Stocks Ex Div Today of note: AMAT COF CNP WWD TPG VRSN LFUS BOKF MTRN DHT AEBI SBSI of note.

- Stocks Ex Div Tomorrow of note: None of note.

- OLED increases quarterly cash dividend to $0.50 per share from $0.45/share.

- QCRH increases cash dividend to $0.10/share from $0.06/share

- FIX increases quarterly dividend to $0.70/share from $0.60/share

What’s Happening This Morning: (as of 7:35 a.m. EST)

- Futures S&P 500 -13, NASDAQ 100 -52, Dow Jones -83 . Europe is higher while Asia is lower ex China. Bond yield is at 4.069% from 4.096% on the 10-Year. Crude Oil and Brent Crude are lower with Natural Gas lower. Gold, Silver and Copper higher. The U.S. Dollar is higher versus the Euro, lower against the Pound and higher against the Yen. Bitcoin is at $67,3330 higher by 0.54% up $371 from $66,593 higher by +0.41% up $272 yesterday.

Sector Action:

- Daily Positive Sectors: Energy, Utilities, Industrials and Materials were higher.

- Daily Negative Sectors: Consumer Cyclicals, Technology and Consumer Defensive were lower.

- One Month Winners: Materials, Energy, Industrials, Real Estate and Consumer Defensive of note.

- Three-Month Winners: Materials, Industrials, Energy, Healthcare and Financials of note.

- Six-Month Winners: Materials, Healthcare, Communication Services, Industrials and Energy of note.

- Twelve-Month Winners: Materials, Communication Services, Industrials, Technology and Financials of note.

- Year to Date Winners: Materials, Industrials, Energy, Consumer Defensive and Real Estate of note.

Bolded means the Sector is new to the period in which it falls.

Upcoming Earnings Of Note: (Erlanger Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Today After the Close:

- Monday Before The Open:

Notable Earnings of Note This Morning:

- Beat: LAMR +0.05, ESAB +0.01 of note.

- Missed: HBM -0.17 of note.

- Flat: None of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: After The Close & This Morning – VAL GH IRTC WK ALRM of note.

- Mixed – None of note.

- Negative or Mixed Guidance: After The Close & This Morning – LAMR of note.

Advance/Decline Daily Update:

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- GapUp: OPEN +18.6%, FET +13.5%, WK +10.9%, KOS +10.7%, RNG +9%, HG +9%, HLIT +8.1%, TNDM +8%, JAKK +7.7%, TLX +7.7%, RMNI +7.4%, ALRM +7.2%, DOMO +7%, AXTI +6.8%, PRDO +6.8%, FIX +4.9%, ASIC +4.6%, TXRH +4.1%, BCAX +3.6%, GDYN +2.7%, AU +2.4%, IRTC +2.3%, FND +2.2%, VRRM +2%, NNN +2% of note.

- GapDown: GRAL -50.6%, INSG -17.1%, VICR -13%, CADL -11.4%, CC -11.4%, AKAM -11.1%, ACH -10.9%, VAL -8%, CPRT -7.6%, WTTR -7.4%, ARDX -7.4%, ENGN -6.9%, TVTX -5.7%, ED -4.9%, TLSI -4.6%, AGIG -4.4%, DBX -4.2%, IAUX -4.1%, EGO -3.7%, MTUS -3.2%, HBM -3.2%, CXW -3.1%, PTCT -3.1%, NEM -3%, VIST -2.5%, RIG -2.4%, ST -2.4% of note.

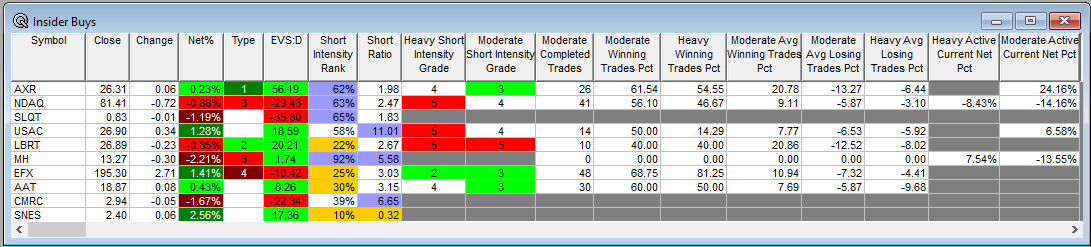

Insider Action: AXRsee Insider Buying with dumb short selling. NDAQ sees Insider Buying with smart short sellers. Above $100,000 in purchases with high shorts but no history: SLQT MH of note.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- WSJ Lead Story: Private Credit Warning Signs After Blue Owl Sells $1.4 Billion in Assets and limits withdrawals. (WSJ)

- Markets Wrap: Stocks Waver With Middle East in Focus Before Economic Data. Bloomberg

- NY Times Business Section Lead Story: China EV Sales Slow and Stocks Suffer. (NYT)

- Bloomberg Lead: Trump’s Iran Ultimatum Set Stage for Strike During IAEA Meeting. (Bloomberg)

- Thoughtful Money: Wall Street Loves National Security. (Podcast)

Economic & Geopolitical:

- Federal Reserve Speakers of note today: 3 see up top of note

- President Trump’s schedule for today:

- Participates in a Working Breakfast with Governors at 9:30 a.m. EST.

- Participates in a Private Meeting at 10:30 a.m. EST.

- Economic Data Out –

- Weekly

- Baker Hughes Rig Count is out at 1:00 p.m. EST.

- Monthly

- December Personal Income is due out at 8:30 a.m. EST and expected to come in at 0.3% from 0.3% in November.

- December PCE Core is due out at 8:30 a.m. EST and expected to rise to 0.40% from 0.20%.

- Q4 GDP is due out at 8:30 a.m. EST and is expected to fall to 3.0% from 4.3%.The Atlanta Fed is calling for growth of 5.60% so this number may be volatile.

- December New Home Sales are due out at 10:00 a.m. EST and expected to come in at 714,000 with no prior month.

- February University of Michigan Consumer Sentiment (Final) is due out at 10:00 a.m. EST and expected to stay at 57.30.

- Weekly

M&A Activity & Daily Changes: None of note.

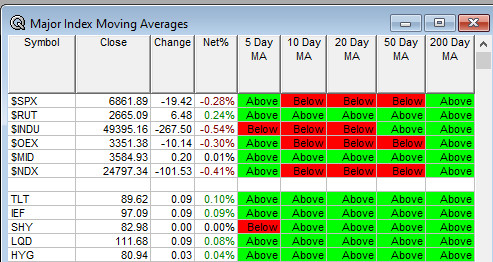

Moving Average Table: 60% from 60% of Equities are Positive, and 96% from 96% Bonds are Positive.

Meeting & Conferences of Note:

- Sellside Conferences:

- Top Analyst, Investor: MRK VNDA of note.

- Shareholder Meetings: XXII of note.

- Fireside Chat: None of note.

- FDA Presentation: None of note.

- R&D Day: None of note.

- Meetings:

- CAGNY

- ECCO

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

- Upgrades: CSGP YETI of note.

- Downgrades: BWA of note.