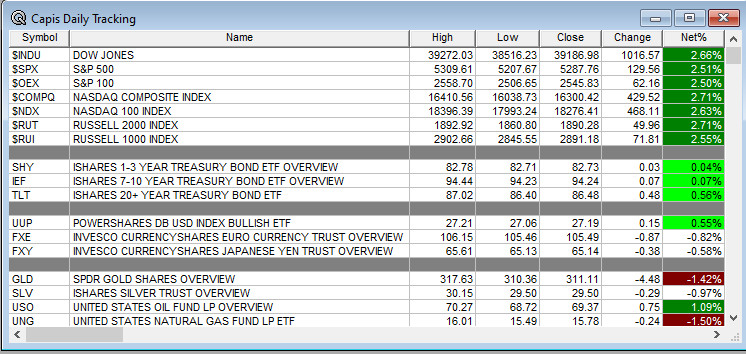

Overnight Summary & Early Morning Trading: The S&P 500 finished Tuesday higher by 2.51% at 5287.76. Monday was lower by -2.36% at 5158.20. Futures are higher this morning by +123 (+2.32%) at 5438 around 6:45 a.m. EDT. The range is now 900 points on the S&P 500 cash for the year, 5200 to 6100. Year to date the S&P 500 is down -10.10% from -12.30% Monday’s close.

Executive Summary: Stocks continue to trade in a volatile pattern of big declines and then big advances. Today, we are seeing a second big up day on news that President Trump was never going to fire Fed Chairman Powell even though he said it multiple times over the last week. Really? Oh yeah, and being tough on China? Nah, that was just an April Fool’s joke. This is how President Trump runs our country now? Many clients have said they do not know how to invest with such back and forth. Our advice, study Trump’s first term.

Breaking News: MBA Mortgage Applications fell -12.70% from -8.5% a week ago.

Article of Note: “White House is Right To Back Off The Fed”. by Bloomberg Editorial Board

Key Events of Note Today:

- Several economic releases out today, see below.

- 5-Year Month Auction at 1:00 p.m. EDT.

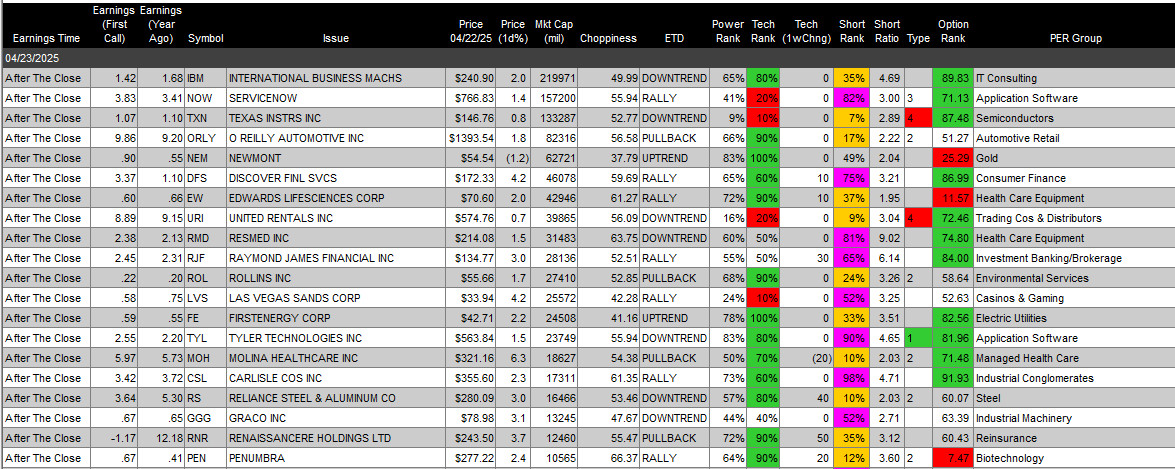

Notable Earnings Out After The Close:

- Beats: PEGA +1.05, CB +0.49, COF +0.42, CASH +0.33, WFRD +0.17, MANH +0.16, EQT+0.15, PKG +0.10, ISRG +0.07, SAP +0.07, STLD +0.06, RRC +0.05 of note.

- Misses: PFSI -1.21, TSLA -0.14, NBHC -0.12, ENPH -0.03 of note.

- Flat: None of note.

- IPOs For The Week: AIRO, CHA, HXHX, OMSE, PHOE

- New IPOs/SPACs launched/News: None of note.

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced: None of note.

- BCTX: Form S-1.. Up to 2,331,002 Common Units, Each Consisting of a Common Share and a Warrant to Purchase One Common Share

- BWAY: Form F-3.. Up to 3,603,745 American Depositary Shares representing 7,207,490 Ordinary Shares

- CDT: Form S-3.. 2,191,012 Shares of Common Stock

- FLYE: Form S-1.. Up to 36,363,636 Shares of Common Stock

- ICU: Form S-3.. Up to 3,529,412 Shares of Common Stock

- INTS: Form S-1.. Up to 4,255,319 Shares of Common Stock

- MTNB: Form S-3.. 16,894,212 Shares of Common Stock

- Notes Priced: None of note.

- Notes Files: None of note.

- Convertibles Filed: None of note.

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Private Placements: None of note.

- Selling Shareholders of note: None of note.

- SRAD – Launch of Public Offering of Class A Ordinary Shares by Selling Shareholders.

- Mixed Shelf Offerings:

- PROP: Form S-3.. $500,000,000 Mixed Shelf

- SOC: Form S-3.. $1,500,000,000 Mixed Shelf

News After The Close:

- Intel (INTC) to fire 20% of workforce.

- President Trump tells reporters that he had no intention of firing Jerome Powell. (The Street.com)

- Grail (GRAL) to present new data on Galleri and its Methylation Platform at American Association for Cancer Research Annual Meeting.

- Tesla (TSLA) misses on earnings and revenue but no worries the Cybercab is coming.

- Trump Administration might cancel COVID-19 vaccine recommendation for kids. (Politico)

- HHS, FDA confirm plan to phase out petroleum-based synthetic dyes in nation’s food supply.

- 10K or Qs Filings/Delays – (Filed), (Delayed) None of note.

Exchange/Listing/Company Reorg and Personnel News:

- Sam Altman to step down as Chairman of Oklo (OKLO).

- THRD Bio Chief Scientific Officer Christopher Dinsmore to step down effective April 21, 2025.

Buybacks:

- SRAD authorizes repurchase, no specifics.

- FSS announces additional $150 million stock repurchase authorization

Dividends Announcements or News:

- Stocks Ex Div Today: LOW LEN BSBR CLX BSAC AM QFIN DX DNUT

- Stocks Ex Div Tomorrow: FMX LEVI CCU AZZ of note.

- OTIS increases quarterly cash dividend 8% to $0.42/share from $0.39/share.

- MET increases quarterly cash dividend 4.1% to $0.5675/share from $0.545/share.

- VBTX increases quarterly cash dividend to $0.22/share from $0.20/share.

Stocks Moving Up & Down Yesterday After The Close:

- Gap Up: PEGA +23.6%, SAP +8.9%, MANH +8.2%, CASH +5.4%, TSLA +3.7%, STLD +3%, VBTX +3%, GOGL +2.6% of note.

- Gap Down: ENPH -11.4%, OKLO -10.2%, PKG -6.1%, BMY -5.6%, SRAD -4.8%, WFRD -3.5% of note.

What’s Happening This Morning: (as of 7:40 a.m. EDT)

Futures S&P 500 +124, NASDAQ +496, Dow Jones +702, Russell 2000 +. Europe is higher and Asia higher ex China. Bonds are at 4.305% from 4.395% yesterday on the 10-Year. Crude Oil and Brent Crude are higher with Natural Gas higher. Gold lower with Silver and Copper higher. The U.S. Dollar is higher versus the Euro, higher against the Pound and higher against the Yen. Bitcoin is at $93,526 from $88,521 higher by $2047 at +2.23%.

- Daily Positive Sectors: All of note led by Consumer Cyclicals, Financials and Communication Services.

- Daily Negative Sectors: None of note.

- One Month Winners: Consumer Defensive of note.

- Three Month Winners: Consumer Defensive of note.

- Six Month Winners: Consumer Defensive and Financials of note.

- Twelve Month Winners: Utilities, Financials, Consumer Defensive, Real Estate, Communication Services, Consumer Cyclical and Technology of note.

- Year to Date Winners: Consumer Defensive, Utilities and Materials of note.

Bolded means the Sector is new to the period in which it falls.

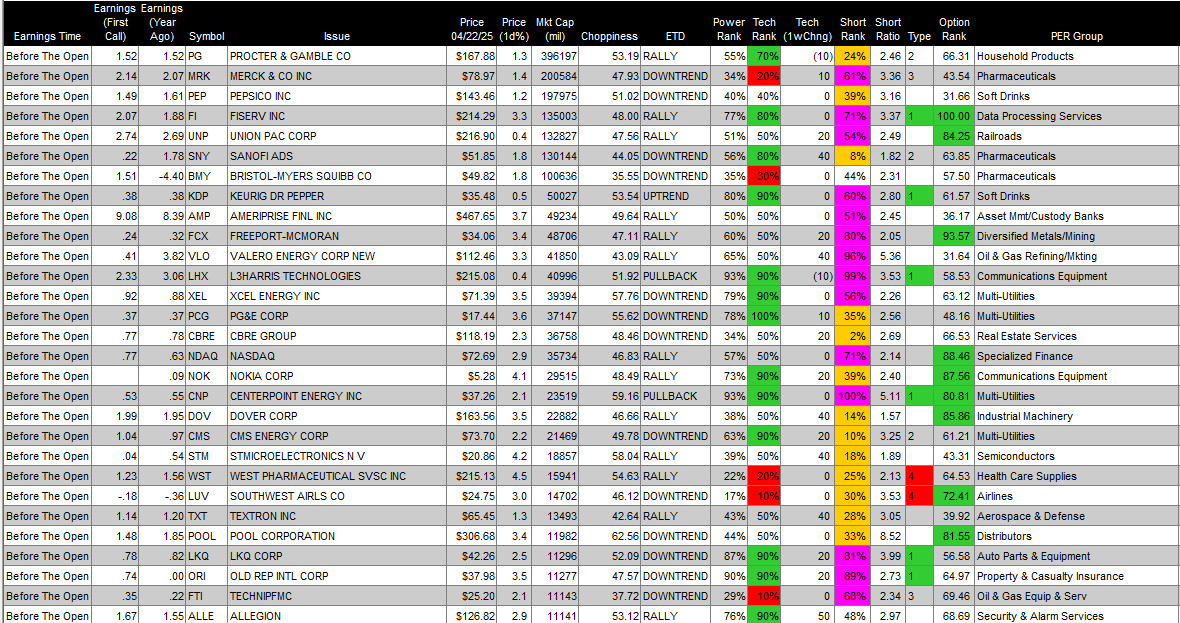

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Wednesday After the Close:

- Thursday Before The Open:

Notable Earnings of Note This Morning:

- Flat: TNL +0.00, CME +0.00 of note

- Beats: BA +0.68, GEV +0.46, BPOP +0.40, RCI +0.27, WAB +0.25, TMHC +0.19, GD +0.16, TEL +0.14, VIRT +0.10, LII +0.09, BSX +0.08, PM +0.08, PRG +0.07, TMO +0.05, ODFL +0.05, R +0.05, HCSG +0.04, TDY +0.03, VRT +0.03, OFG +0.03, OTIS +0.02, NEE +0.02, PB +0.02, CHKP +0.02 of note.

- Misses: COOP (1.55), SF (1.15), WSO (0.33), LAD (0.20), MHO (0.18), MAS (0.04), EDU (0.03), T (0.02), AVY (0.02), UMC (0.02) of note.

- Still to Report: APH, FHB, GATX, NSC of note.

Company Earnings Guidance:

- Positive Guidance: CALX of note.

- Negative or Mixed Guidance: HXL of note.

Advance/Decline Daily Update: The A/D did not make new lows with the recent volatility.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: PEGA +26.2%, VRT +18.4%, NEOG +9.7%, RRC +9.2%, SAP +8.7%, GOGL +7.8%, IPHA +7.7%, ERJ +7.4%, MANH +6.9%, TSLA +6.4%, TEL +6.4%, CASH +6.1%, UMC +5.9%, RXRX +5.7%, GRAL +4.5%, VBTX +4.2%, COF +4%, KAR +3.7%, VNO +3.3%, TOI +3%, TMO +2.9%, ASR +2.4%, CHKP +2.4%, MET +2.3% of note.

- Gap Down: ENPH -11.1%, WNC -10.6%, PKG -5.2%, BMY -3.5%, EDU -3.4%, SRAD -2.9%, ZWS -2.7%, OKLO -2.6%, PFSI -2.1% of note.

Insider Action: None of note see Insider Buying with dumb short selling. GTE sees Insider Buying for a second day in a row with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Bloomberg: Trump Floats “Substantial” China Tariff Cuts in Trade Deal. (Bloomberg)

- Market Wrap: Wall Street’s Relief Rally to power ahead. (Bloomberg)

- AAPL and META fined a combined €700M by the EU. (Bloomberg)

- Elon Musk to refocus on Tesla. (Bloomberg)

- Boeing (BA) seeks to expand 737 Max production. (Bloomberg)

- Bloomberg: The Big Take: Markets are discovering the Real Trump Trade is “Sell America”. (Podcast)

Bolded Royal Blue on story headlines means behind a Pay Wall.

Economic & Geopolitical:

- Economic Releases:

- April S&P Global US Manufacturing PMI and Global US Services PMI are due out at 9:45 a.m. EDT and last month came in at 50.20 and 54.40 respectively.

- March New Home Sales are due out at 10:00 a.m. EDT and are expected to improve to 684,000 from 676,000.

- Weekly Crude Oil Inventories will be out at 10:30 a.m. EDT.

- Federal Reserve Speakers of note today.

- Federal Reserve Chicago President Austan Goolsbee speaks at 9:00 a.m. EDT.

- Federal Reserve St. Louis President Alberto Musalem at 9:30 a.m. EDT.

- Federal Reserve Governor Christopher Waller speaks at 9:35 a.m. EDT.

- Federal Reserve Cleveland President Beth Hammack speaks at 6:30 p.m. EDT.

- At 2:00 p.m. EDT the Federal Reserve’s Latest Beige Book will be released.

- President Trump’s Daily Schedule.

- President Trump receives the Intelligence Briefing at 11:00 p.m. EDT.

- President Trump signs Executive Orders at 5:00 p.m. EDT.

M&A Activity and News:

- None of note.

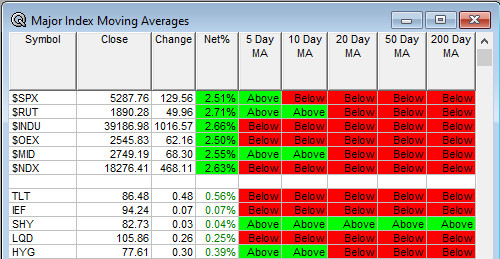

Moving Average Table: Moves from 0% to 17% from yesterday on Equity Indexes. TLT remains weak.

Meeting & Conferences of Note:

- Sellside Conferences:

- Citi Biotech Innovation Forum

- Shareholder Meetings: AN, ASML, ASR, CI, DPZ, ETN, GS, HLF, LEVI, PNC, SABR, STRA, TXT

- Top Analyst, Investor Meetings: AUTL, DFRG, LPTX, QGEN, RGLD

- Fireside Chat: None of note.

- R&D Day: None of note.

- FDA Presentation: AUTL: Data Presentation for AUTO6NG, AUTO8

- Industry Meetings or Events:

- AI Week

- ASHRAE

- NY Auto Show

- Planet MicroCap Showcase

- World Vaccine Congress

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

- Upgrades: ARI DWTX INTU LAD LOMA

- Downgrades: CVX ENPH MMFS MUR NPWR SEDG