Overnight Summary & Early Morning Trading: The S&P 500 finished Monday lower by -2.36% at 5158.20. Last Thursday the index closed higher by 0.13% at 5282.70. Futures are higher this morning by +50 (+0.96%) at 5234 around 6:30 a.m. EDT. The range is now 1000 points on the S&P 500 cash for the year, 5100 to 6100. Year to date the S&P 500 is down -12.30% from -10.18% Thursday’s close.

Executive Summary: Stocks continue to trade in a volatile pattern of big declines and then big advances.

Breaking News: None of note

Key Events of Note Today:

- API Petroleum Data out today at 4:30 p.m. EDT.

- 2 Year Month Auction at 1:00 p.m. EDT.

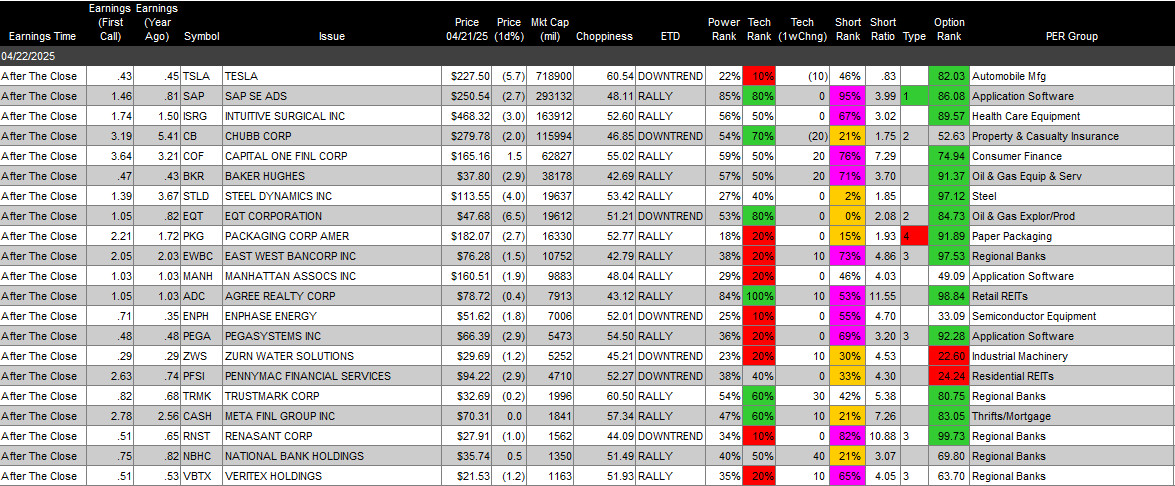

Notable Earnings Out After The Close:

- Beats: MEDP +0.61, WTFC +0.20, CADE +0.07, CALX +0.06, WRB +0.03, CATY +0.03, WAL +0.01 of note.

- Misses: BOKF -0.13, ZION +0.06, HXL -0.06 of note.

- Flat: None of note.

- IPOs For The Week: AIRO, CHA, HXHX, OMSE, PHOE

- New IPOs/SPACs launched/News: None of note.

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced: None of note.

- LGCL: Form F-1.. Up to 21,621,621 Ordinary Shares

- Notes Priced: None of note.

- Notes Files: None of note.

- Convertibles Filed: None of note.

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Private Placements: None of note.

- Selling Shareholders of note: None of note.

- Mixed Shelf Offerings:

- PFIS: FORM S-3 – $150,000,000 Mixed Shelf Offering

News After The Close:

- Macquarie Group to divest its public investments business and enter broader strategic relationship with Nomura (NMR).

- Quiet after hours as earnings begin to drive the news.

- 10K or Qs Filings/Delays – (Filed), (Delayed) None of note.

Exchange/Listing/Company Reorg and Personnel News:

- MDB interim CFO Srdjan (“Serge”) Tanjga to resign, effective May 8.

- HIMS COO Melissa Baird to transition into an advisory role in the coming months.

Buybacks:

- CALX authorizes the repurchase of up to an additional $100 mln of its common stock; brings total to $300 mln.

- MEDP authorizes up to $1 billion of repurchases.

Dividends Announcements or News:

- Stocks Ex Div Today: CVS PBR DELL CRS APA KOF AGX LTC GBX MGIC.

- Stocks Ex Div Tomorrow: LOW LEN BSBR CLX BSAC AM QFIN DX DNUT of note.

- PSX increases quarterly cash dividend to $1.20/share from $1.15/share

Stocks Moving Up & Down Yesterday:

- Gap Up: CALX +16.4%, ATKR +5.2%, WTFC +3.9% of note.

- Gap Down: MEDP -7.6% of note.

What’s Happening This Morning: (as of 7:40 a.m. EDT)

Futures S&P 500 +44, NASDAQ +155, Dow Jones +327, Russell 2000 +. Europe is lower ex the FTSE and Asia is lower ex China. Bonds are at 4.395% from 4.356% yesterday on the 10-Year. Crude Oil and Brent Crude are higher with Natural Gas higher. Gold, Silver and Copper higher. The U.S. Dollar is higher versus the Euro, higher against the Pound and lower against the Yen. Bitcoin is at $88,521 from $87,341 higher by $1225 at +1.40%.

- Daily Positive Sectors: None of note.

- Daily Negative Sectors: All led by Technology, Consumer Cyclicals and Communication Services.

- One Month Winners: Consumer Defensive of note.

- Three Month Winners: Consumer Defensive of note.

- Six Month Winners: Consumer Defensive and Financials of note.

- Twelve Month Winners: Utilities, Financials, Consumer Defensive, Real Estate, Communication Services, Consumer Cyclical and Technology of note.

- Year to Date Winners: Consumer Defensive, Utilities and Materials of note.

Bolded means the Sector is new to the period in which it falls.

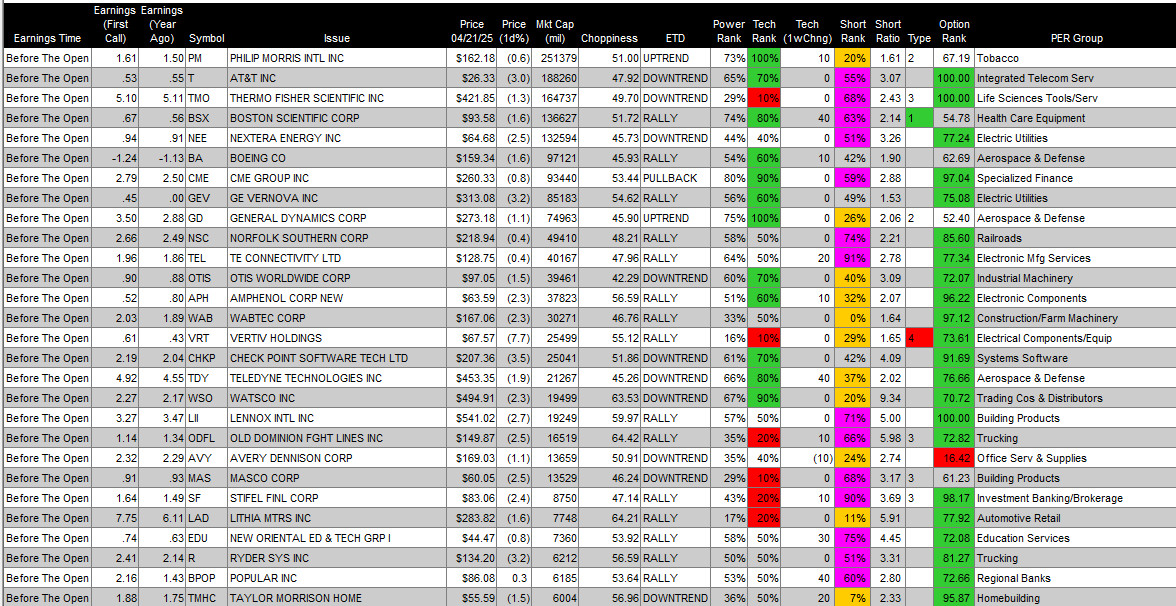

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Tuesday After the Close:

- Wednesday Before The Open:

Notable Earnings of Note This Morning:

- Flat: None of note

- Beats: LMT +0.94, ELV +0.56, MCO +0.31, DHR +0.25, GE +0.22, SYF +0.22, PHM +0.14, EFX +0.12, RTX +0.12, MMM +0.11, PNR +0.10 of note.

- Misses: HRI -0.92, DGX -0.21, NOC -0.18, VMI -0,04 of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: CALX of note.

- Negative or Mixed Guidance: HXL of note.

Advance/Decline Daily Update: The A/D was beginning to improve and then the bottom fell out.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: CALX +13.4%, HCM +8.1%, IGT +6.3%, ELS +5.5%, ATKR +4.5%, DHR +3.4%, VCYT +3.3%, CWAN +3.1%, NMR +3.1%, APPN +2.6%, CATY +2.6%, FCPT +2.2%, SPGI +2%, WFRD +2% of note.

- Gap Down: MEDP -6.7%, AZZ -5.4%, ZION -4.5%, HXL -3.7%, MYGN -3.1% of note.

Insider Action: None of note see Insider Buying with dumb short selling. GTE sees Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Bloomberg: Vance Calls For Stronger U.S. India Ties as Trade Talks Progress. (Bloomberg)

- Market Wrap: Gold Tops $3,500 as Stocks Bounce Higher. (Bloomberg)

- Japanese investors sold $20 bln of international debt following tariffs.

- Amazon (AMZN) has paused some data center leases. (CNBC)

- Five Things To Know Before The Market Opens. (CNBC)

- Bloomberg: The Big Take: Markets are discovering the Real Trump Trade is “Sell America”. (Podcast)

Bolded Royal Blue means behind a Pay Wall.

Economic & Geopolitical:

- Economic Releases:

- API Petroleum Institute Weekly Report is due out at 4:30 p.m. EDT.

- Federal Reserve Speakers of note today.

- Federal Reserve Vice Chairman Phillip Jefferson speaks at 9:00 a.m. EDT.

- Federal Reserve Philadelphia President Patrick Harker at 9:30 a.m. EDT.

- Federal Reserve Governor Adriana Kugler speaks at 6:00 p.m. EDT.

- President Trump’s Daily Schedule.

- Press Briefing at 1:00 p.m. EDT.

- President Trump participates in the swearing in of the new SEC Chairman at 4:00 p.m. EDT.

M&A Activity and News:

- None of note.

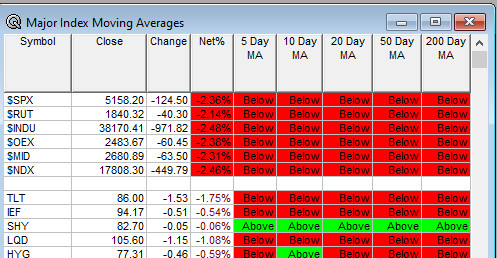

Moving Average Table: Moves from 23% to 0% from yesterday. TLT remains weak.

Meeting & Conferences of Note:

- Sellside Conferences: None of note.

- Shareholder Meetings: ADBE, BAC, BIO, CC, SHEN, WASH

- Top Analyst, Investor Meetings: IPSC, NVNO

- Fireside Chat: None of note.

- R&D Day: None of note.

- FDA Presentation: BMY: PDUFA Date for Opdivo (nivolumab) plus Yervoy.

- Industry Meetings or Events:

- AI Week

- Centri Capital Conference

- NY Auto Show

- Planet MicroCap Showcase

- World Vaccine Congress

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

- Upgrades: PAGS PSA SLGN SRAD STNE

- Downgrades: MA CURV LNT TXN YMAB

- JP Morgan Trading Desk: “.. the question is whether it can hold [this rally] or if the market reverses lower, breaking its 5,100 support. .. we feel a completed trade deal is the only catalyst that can break the market out to the upside, and this would still need resilient macro data and solid earnings.” Agree 1000%.