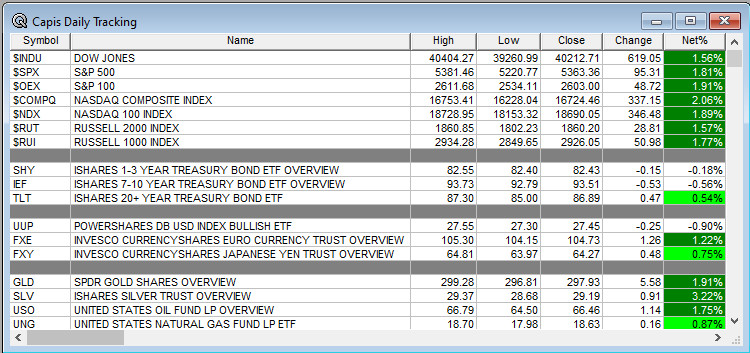

Overnight Summary & Early Morning Trading: The S&P 500 finished Friday higher by 1.81% at 5363.36. Thursday lower by -3.46% at 5268.05. Futures are higher this morning by +63.50 (+1.18%) at 5454 around 6:25 a.m. EDT. The range is now 800 points on the S&P 500 cash for the year, 5300 to 6100. Year to Date the S&P 500 is down -8.81%.

Article of Note: “Trump’s Exceptional Tariff Weekend” by Wall Street Journal Editorial Board.

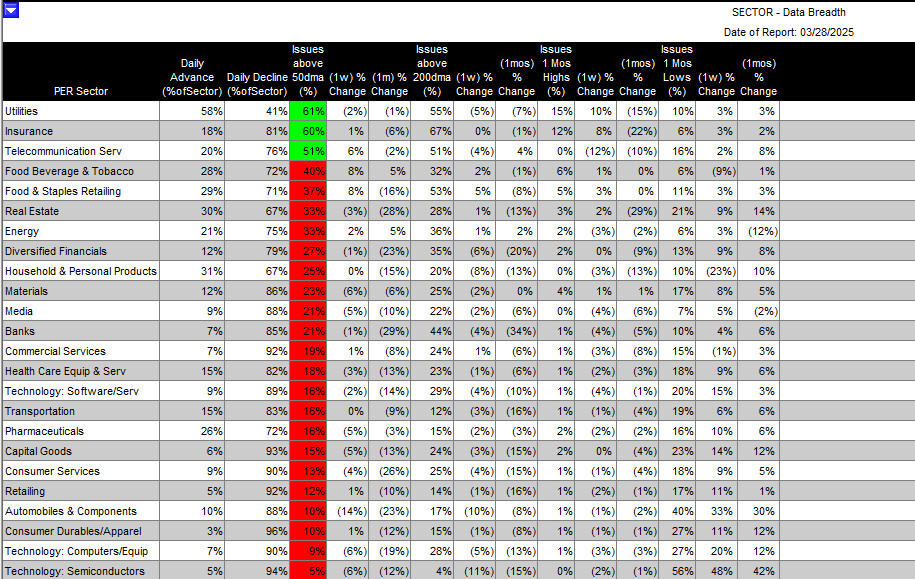

Chart of the Day: No sectors see more than half their names above their 50 day moving averages.

Quote of the Day:

Breaking News: Former Treasury Secretary Yellen was just interviewed on CNBC. Worth the listen to.

Key Events of Note Today:

- No economic releases of note.

- 3 & 6 Month Auction at 11:30 a.m. EDT.

Notable Earnings Out After The Close

- Beats: None of note.

- Misses: None of note.

- IPOs For The Week: AIRO, CHA, HXHX, OMSE, PHOE

- New IPOs/SPACs launched/News:

- IPOs Filed/Priced:

- Secondaries Filed or Priced:

- PTLE Closing of $7.14 Million Public Offering of its Ordinary Shares

- MSS: Form S-1 Filed – 62,700,000 Shares of Class A Common Stock

- LTRY: Form S-1.. Primary Offering of Shares of Common Stock to enable the Company to raise $100,000,000 under a Stock Purchase Agreement entered into on November 13, 2024.

- Notes Priced:

- XRX Closing of Senior Secured Notes Offering

- Notes Files:

- Convertibles Filed:

- Direct Offering:

- Exchangeable Subordinate Voting Shares: None of note.

- Private Placements:

- TTNP $1 Million Private Placement of Convertible Preferred Stock

- Selling Shareholders of note:

- Mixed Shelf Offerings:

- BORR files mixed securities shelf offering.

- UMBF files mixed securities shelf offering.

News After The Close:

- Egypt saw its credit rating revised to stable and Italy to raised by one the top credit agencies.

- President Trump waived reciprocal tariffs on some consumer electronic products such as the Apple iPhone produced in China but left the 20% tariff in effect. (CNBC)

- President Trump says he will announce semiconductor tariffs in the next week. (Reuters)

- On Sunday’s Meet The Press, Hedge Fund Manager Ray Dalio says tariff actions could create “something worse than a recession”. (MarketWatch)

- Barron’s is + on AMAT, AMZN, PLTR, TSLA, XOM, CVX, NEE, AEP.

- 10K or Qs Filings/Delays – (Filed), (Delayed) of note.

Exchange/Listing/Company Reorg and Personnel News:

Buybacks

- HOV authorizes a $25 mln increase to its share repurchase program.

Dividends Announcements or News:

- Stocks Ex Div Today: HRL VIV GGG LTM OZK VTMX WERN KEN UVV

- Stocks Ex Div Tomorrow: ABBV ABT FCX WSO MAA AFG PECO ACA TRN BKE CHCO ARR SBR

- AON increases quarterly cash dividend 10% to $0.745/share from $0.675/share.

Stocks Moving Up & Down Yesterday:

Gap Up: SLP (32.48 +26.48%), RYTM (59.09 +25.86%), HMY (17.25 +32.69%), IAG (7.22 +28.24%), AU (42.78 +27.5%), NEM (55.09 +24.68%), SA (12.44 +24.65%), GFI (24.57 +23.19%), HL (5.8 +22.78%), KGC (14.39 +22.01%), AVAV (146.49 +31.2%), AGX (147.55 +22.88%), CVNA (204.99 +26.09%), LOVE (18.14 +25.71%), AVGO (181.12 +23.81%), DOMO (8.15 +22.74%), BTU (12.77 +21.92%) of note.

Gap Down: NEOG (5.55 -28.91%), CRL (98.84 -27.8%), HELE (34.28 -23.41%), TAL (9.58 -22.03%), COOP (108.5 -19.16%), LX (6.65 -19%), HLF (6.76 -18.26%) of note.

What’s Happening This Morning: (as of 7:45 a.m. EDT) Futures S&P 500 +78, NASDAQ +314, Dow Jones +398, Russell 2000 +17. Europe is higher and Asia is higher. Bonds are at 4.433% from 4.435% Friday on the 10-Year. Crude Oil and Brent Crude are higher with Natural Gas lower. Gold is lower with Silver and Copper higher. The U.S. Dollar is lower versus the Euro, lower against the Pound and lower against the Yen. Bitcoin is at $84,619 from $82,037 higher by $621 at 0.75%.

- Daily Positive Sectors: All were higher for the day led by Materials, Energy and Technology.

- Daily Negative Sectors: None of note.

- One Month Winners: Consumer Defensive and Utilities of note.

- Three Month Winners: Consumer Defensive, Utilities and Materials of note.

- Six Month Winners: Consumer Defensive and Financials of note.

- Twelve Month Winners: Utilities, Financials, Consumer Defensive, Communication Services, Technology and Real Estate of note.

- Year to Date Winners: Consumer Defensive, Utilities and Materials of note.

Bolded means the Sector is new to the period in which it falls.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Monday After the Close:

- Tuesday Before The Open:

Notable Earnings of Note This Morning:

- Flat: FAST 0.00 of note

- Beats: BLK +1.16, JPM +0.44, of note.

- Misses: KMX -0.08 of note.

- Still to Report:

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative or Mixed Guidance: None of note.

Advance/Decline Daily Update: The A/D weakened with yesterday’s action.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: THTX +27.3%, TMC +20.5%, MP +12.4%, BBY +5.2%, AAPL +4.9%, INTC +4.8%, PLTR +2.1%, IDYA +2.1% of note.

- Gap Down: ORGO -7.3%, EXAS -3%, MTB -2.5% of note.

Insider Action: None see Insider Buying with dumb short selling. None see Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Bloomberg: Tump warns Sunday that tariffs coming to electronics after Friday reprieve. (Bloomberg)

- Dollar weakness causes traders to raise hedges to 5-year high. (Bloomberg)

- U.S. and Japan will hold trade talks on Thursday. (Bloomberg)

- The Trump administration is expected to begin trade negotiations with dozens of countries with goals of more energy purchases, lower export tariffs, lower trade deficits, and lower taxes on American technology companies. (The Washington Post)

- Iran and the U.S. had “constructive” meeting and plan further nuclear discussions this week. (The Washington Post)

- Pfizer(PFE) ends Obesity Pill after liver damage reported. (Bloomberg)

- Five Things To Know Before The Market Opens. (CNBC)

Bolded Royal Blue means behind a Pay Wall.

Economic & Geopolitical:

- Economic Releases:

- None of note.

- Federal Reserve Speakers of note today.

- There are 4 Fed speakers today.

- Federal Reserve Richmond President Thomas Barkin at 12:00 p.m. EDT.

- Federal Reserve Governor Christopher Waller speaks at 1:00 p.m. EDT.

- Federal Reserve Philadelphia President Patrick Harker speaks at 6:00 p.m. EDT.

- Federal Reserve Atlanta President Raphael Bostic speaks at 7:40 p.m. EDT.

- There are 4 Fed speakers today.

- President Trump’s Daily Schedule.

- President Trump heads to at 3:45 p.m. EDT.

- Press Briefing at 1:00 p.m. EDT.

- President Trump heads to at 4:00 p.m. EDT.

M&A Activity and News:

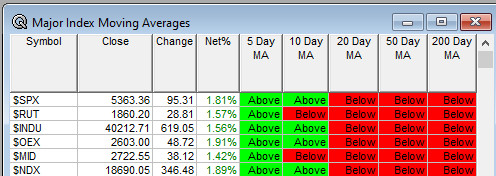

Moving Average Table: Moves from 0% to 33% week over week.

Meeting & Conferences of Note: (Not updated today, back tomorrow)

-

- Sellside Conferences:

- Sellside Conferences:

-

- Shareholder Meetings: GT, HPQ

- Top Analyst, Investor Meetings: IONA

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation:

- ASGCT Annual Meeting

- Industry Meetings or Events:

- European Conference on Interventional Oncology

- European Congress on Infectious Diseases

- Ionis Expert Panel Discussion on sHTG

- Ongoing investor education series

- Space Symposium

- TE25-2: Collaborative Autonomy Integration

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

-

- Upgrades:

- Downgrades:

-

-