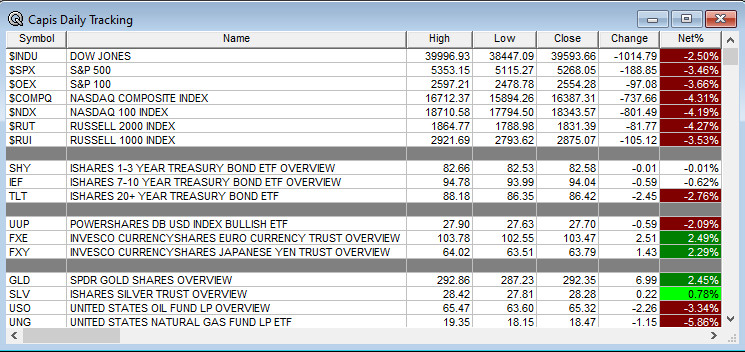

Overnight Summary & Early Morning Trading: The S&P 500 finished Thursday lower by -3.46% at 5268.05. Wednesday higher by 9.52% at 5456.90. Futures are higher this morning by +14.50(+0.27%) at 5316 around 7:40 a.m. EDT. The range is now 900 points on the S&P 500 cash for the year, 5200 to 6100.

Article of Note: “Treasuries Are Trading Like Risky Assets in Warning To Trump.” (Bloomberg)

Chart of the Day: Pricesmart (PSMT) rose on a slight earnings beat yesterday. Same-store sales rose +6.7% however.

Quote of the Day: “The economy is facing considerable turbulence,” JPMorgan Chief Executive Jamie Dimon said in a press release. “We continue to believe it is prudent to maintain excess capital and ample liquidity in this environment.”

Key Events of Note Today:

- PPI up at 8:30 a.m. EDT.

- Weekly Baker Hughes Rig Count out at 8:30 a.m. EDT.

Notable Earnings Out After The Close

- Beats: None of note.

- Misses: None of note.

- IPOs For The Week: ALEH, FATN, LAWR, MB, OMSE, PHOE, RYET

- New IPOs/SPACs launched/News:

- IPOs Filed/Priced:

- Secondaries Filed or Priced:

- REBN: Form S-1.. 6,667,949 Shares

- Notes Priced: KEYS Pricing of Public Offering of Senior Unsecured Notes

- Notes Files:

- Convertibles Filed:

- Direct Offering:

- Exchangeable Subordinate Voting Shares: None of note.

- Private Placements:

- Selling Shareholders of note:

- Mixed Shelf Offerings:

News After The Close:

- Treehouse Foods (THS) implementing operational efficiency strategies, guides Q1 revs above consensus, reaffirms FY25 revenue outlook.

- Federal Reserve Bank of Boston President Susan Collins says tariff increase could delay rate cuts. (Bloomberg)

- European Commission President says EU could tax US Big Tech if trade talks fail.

- Range Resources (RRC) expects to report a total loss on derivatives of $159 mln in Q1.

- MLM CFO James Nickolas to resign; guides Q1 revs in-line.

- Harley Davidson (HOG) trading higher on report it’s exploring $1+ bln sale of its financing arm.

- 10K or Qs Filings/Delays – (Filed), (Delayed) of note.

Exchange/Listing/Company Reorg and Personnel News:

- ALSN announces Scott Mell as New CFO, effective April 14.

- ARQT announces that CFO, David Topper, is retiring from the company and that Latha Vairavan, currently Vice President and Controller, will assume role of CFO.

Buybacks

- AGX increases share repurchase program from $125 million to $150 million

Dividends Announcements or News:

- Stocks Ex Div Today: AMT GD LYG MRVL TOL HMY SNX VIPS SAIC BKU AAP AEO GNL PMT MOMO

- Stocks Ex Div Tomorrow: HRL VIV GGG LTM OZK VTMX WERN KEN UVV

- FAST increases quarterly cash dividend to $0.44/share from $0.43/share.

- ADC announces a 1.2% increase to its monthly dividend, now at $0.256/share.

- TRGP to increase its quarterly dividend by 33% to $1.00/sh, up from $0.75/share.

Stocks Moving Up & Down Yesterday:

Gap Up: CERT +23.3%, RXRX +22.4%, ARGX +8.7%, CRL +5.4%, TARA +4%, ALSN +3.8%, HOG +2.4%, ULCC +2.2%, AGX +2.1% of note.

Gap Down: J -10.3%, CNC -5.5%, ARQT -3.3% of note.

What’s Happening This Morning: (as of 8:15 a.m. EDT) Futures S&P 500 +23, NASDAQ +98, Dow Jones +127, Russell 2000 –. Europe is lower ex the FTSE and Asia is lower ex China’s Nifty 50. Bonds are at 4.435% from 4.308% yesterday on the 10-Year. Crude Oil and Brent Crude arehigher with Natural Gas lower. Gold, Silver and Copper higher. The U.S. Dollar is lower versus the Euro, lower against the Pound and lower against the Yen. Bitcoin is at $82,037 from $81,661 higher by $2508 at 3.15%.

- Daily Positive Sectors: Consumer Services was the only one up for the day.

- Daily Negative Sectors: All others led by Energy, Technology and Consumer Cyclicals of note.

- One Month Winners: None of note.

- Three Month Winners: Consumer Defensive of note.

- Six Month Winners: None of note.

- Twelve Month Winners: Utilities, Consumer Defensive, Financials, Communication Services and Real Estate of note.

- Year to Date Winners: Consumer Defensive of note.

Bolded means the Sector is new to the period in which it falls.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Friday After the Close: None of note.

- Monday Before The Open: GS MTB

Notable Earnings of Note This Morning:

- Flat: FAST 0.00 of note

- Beats: BLK +1.16, JPM +0.44, MS +0.39, WFC +0.16, BK +0.08 of note.

- Misses: KMX -0.08 of note.

- Still to Report:

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative or Mixed Guidance: NEOG of note.

Advance/Decline Daily Update: The A/D weakened with yesterday’s action.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: CERT +20.9%, RXRX +19.5%, TARA +6.7%, ARGX +5.1%, CRL +2.2%, ULCC +2.2%, YRD +2% of note.

- Gap Down: STLA -2.4%, THS -2.4% of note.

Insider Action: None see Insider Buying with dumb short selling. None see Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Bloomberg: China Raises Tariffs on U.S. Goods to 125%. (Bloomberg)

- JP Morgan (JPM) Traders notch record revenue on market chaos. (Bloomberg)

- All bank earnings were strong this morning.

- Blackrock’s (BLK) Larry Fink likens current environment to 2008 crisis. (MarketWatch)

- Stocks making the biggest moves: JPM WFC MS NEM. (CNBC)

- Five Things To Know Before The Market Opens. (CNBC)

Bolded Royal Blue means behind a Pay Wall.

Economic & Geopolitical:

- Economic Releases:

- March PPI is due out at 8:30 a.m. EDT and is expected to fall to 0.10% from 0.20%.

- April University of Michigan Consumer Sentiment is due out at 10:00 a.m. EDT and expected to fall to 54.80% from 57%.

- Weekly Baker Hughes Rig Count at 1:00 p.m. EDT.

- Federal Reserve Speakers of note today.

- There are 5 Fed speakers today!!!

- Federal Reserve Minneapolis President Neel Kashkari at 8:00 a.m. EDT.

- Federal Reserve Boston President Susan Collins at 9:00 a.m. EDT.

- Federal Reserve St. Louis President Alberto Musalem at 10:00 a.m. EDT

- Federal Reserve New York President John Williams at 11:00 a.m. EDT.

- Federal Reserve Richmond President Thomas Barkin at 12:00 p.m. EDT.

- There are 5 Fed speakers today!!!

- President Trump’s Daily Schedule.

- President Trump heads to Walter Reed for his annual physical at 11:00 a.m. EDT and will depart at 3:45 p.m. EDT.

- Press Briefing at 1:00 p.m. EDT.

- President Trump heads to Palm Beach at 4:00 p.m. EDT.

M&A Activity and News:

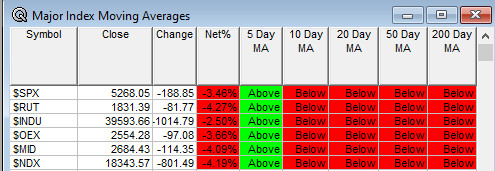

Moving Average Table: Moves from 0% to 33%. Other asset classes included for today.

Meeting & Conferences of Note: (Not updated today, back tomorrow)

-

- Sellside Conferences:

- Sellside Conferences:

-

- Shareholder Meetings: ARDX, BMO, CNTM, FMX, ICU, MBOT

- Top Analyst, Investor Meetings: YPF

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation:

- ARGX: PDUFA Decision date for VYVGART SC pre-filled syringe.

- Industry Meetings or Events:

- World Congress on Osteoporosis Osteoarthritis and Musculoskeletal Diseases

- CEM Scottsdale Capital Event

- CyberArk IMPACT

- Google Cloud Next

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

-

- Upgrades: AXP EG HII LHX NEM NKTR MTSI OBDC PGC RR SMR SRAD STKS VLN CWT

- Downgrades:

-

-