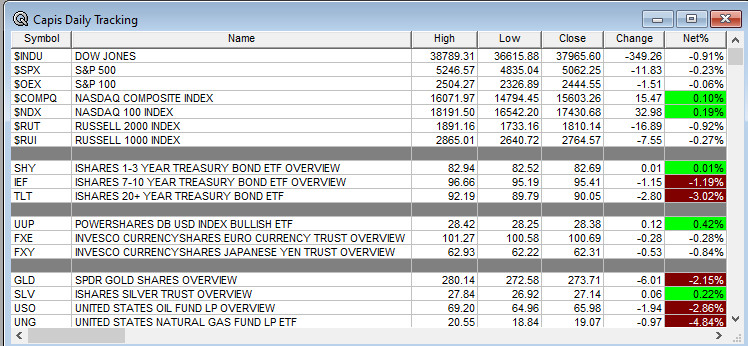

Overnight Summary & Early Morning Trading: The S&P 500 finished Monday lower by -0.23% at 5062.25. Friday was lower by -5.97% at 5074.08. Futures are higher this morning by +74 (1.46%) at 5171 around 7:10 a.m. EDT. The range is 1000 points on the S&P 500 for the year, 5100 to 6100, a drop of 200 points since Friday. Thought for the upcoming week: Monday was an extremely volatile day as the high was 5246.57 with the low at 4835.04 a daily range of 8.11% which is rather crazy.

Article of Note: “How The Tariff Damage Spreads, Auto Edition” by WSJ Editorial Board.

Chart of the Day: Erlanger Option Ranks on the Sectors climbs to a new high with yesterday’s range of 8.11%. Extreme levels usually marks a low.

Breaking News: Great interview with Treasury Secretary Scott Bessent and Hedge Fund Icon Ray Dalio on CNBC this morning.

Key Events of Note Today:

- NFIB Data came in light and weekly API due out after the close.

- 3 year Treasury Auction at 1:00 p.m. EDT.

- Only one thing matters: Tariff negotiations and the tone of the negotiations.

Notable Earnings Out After The Close

- Beats: LEVI +0.10, DAVE +0.02 of note.

- Misses: GBX -0.22 of note.

- IPOs For The Week: ALEH, FATN, LAWR, MB, OMSE, PHOE, RYET

- New IPOs/SPACs launched/News:

- IPOs Filed/Priced:

- Secondaries Filed or Priced:

- EFSH: Form S-1.. 778,524,571 Common Shares.

- MULN: FORM S-1 – 200,000,000 Shares of Common Stock

- Notes Priced: VICI Closing of $1.3 Billion Senior Unsecured Notes Offering

- Notes Files:

- Convertibles Filed:

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Private Placements:

- Selling Shareholders of note:

- FANG files for 6,842,625 share common stock offering by selling shareholder.

- DLR files for 6.7 mln share common stock offering by selling shareholders

- BOXL: files 1,323,000 Shares of Class A Common Stock offered by the selling

shareholders.

- Mixed Shelf Offerings:

News After The Close:

- Private Medicare Plans to get large rate boost from Trump administration next year. (WSJ)

- China vows to fight to the end over 34% and 54% tariff increases.

- CACI awarded a five-year task order valued at up to $66 mlnto provide expertise to U.S. Navy’s Naval Surface Warfare Center

- NASDAQ (NDAQ) reports March trading volumes. (Release)

- Core Scientific (CRZ) releases unaudited production and operations updates for March 2025; mines 247 Bitcoin.

- Pacira Biosciences (PCRX) announces settlement of U.S. Patent Litigation for EXPAREL.

- Marvell (MRVL) to sell automotive ethernet business to Infineon (IFNNY) for $2.5 billion in cash.

- Apple (AAPL) ticking higher after hours on report that consumers are rushing to buy iPhones before tariffs. (Bloomberg)

- 10K or Qs Filings/Delays – (Filed), (Delayed) of note.

Exchange/Listing/Company Reorg and Personnel News:

- PRAA appoints President of PRA Group Europe Martin Sjolund to serve as President and CEO, effective June 17

- PNC names former BlackRock exec Mark Wiedman as president of the corporation and its wholly owned banking subsidiary, PNC Bank, effective immediately.

Buybacks

- AVGO announces $10 billion share repurchase authorization.

Dividends Announcements or News:

- Stocks Ex Div Today: JD DG MNSO TIGO MAIN GBCI THO SLVM WLY OPFI

- Stocks Ex Div Tomorrow: MA BBVA BEKE HTHT GAP GNTX IDCC KRG MSM KAI BRC WB

Stocks Moving Up & Down Yesterday:

Gap Up: PCRX +15%, HUM +11.8%, CVS +6.6%, UNH +5.4%, AVGO +3.1%, LEVI +2.6%, PLAY +2.5% of note.

Gap Down: CVRX -18.2%, ASR -5%, GBX -4.1% of note.

What’s Happening This Morning: (as of 8:15 a.m. EDT) Futures S&P 500 +137, NASDAQ +456, Dow Jones +1141, Russell 2000 +56. Europe and Asia are high er. Bonds are at 4.22% from 3.975% yesterday on the 10-Year. Crude Oil and Brent Crude are higher with Natural Gas higher. Gold, Silver and Copper higher. The U.S. Dollar is lower versus the Euro, lower against the Pound and lower against the Yen. Bitcoin is at $79,875 from $76,591 higher by $1605 at +2.07%.

- Daily Positive Sectors: Communication Services and Technology of note.

- Daily Negative Sectors: Real Estate, Energy, Utilities, Consumer Defensive and Consumer Cyclical of note.

- One Month Winners: None of note.

- Three Month Winners: Consumer Defensive of note.

- Six Month Winners: None of note.

- Twelve Month Winners: Utilities, Consumer Defensive, Financials, Communication Services and Real Estate of note.

- Year to Date Winners: Consumer Defensive of note.

Bolded means the Sector is new to the period in which it falls.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Tuesday After the Close: CALM of note

- Wednesday Before The Open: NEOG DAL of note

Notable Earnings of Note This Morning:

- Flat: None of note

- Beats: WBA +0.10, WDFC +0.05 of note.

- Misses: RPM -0.15 of note.

- Still to Report:

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative or Mixed Guidance: GBX of note.

Advance/Decline Daily Update: The A/D made a new low. Awful.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: NYXH +37.5%, PCRX +24.2%, LEVI +13.3%, HUM +11.1%, BORR +9.3%, CVS +7.7%, UNH +5.8%, CVI +5%, KALV +5%, VLRS +4.9%, AGX +4.6%, PNC +4.4%, ARCO +3.9%, AIR +3.7%, AVGO +3.6%, MRVL +3.5%, NKE +3.3%, VEON +2.9%, UMC +2.8%, ARGX +2.7%, JNJ +2.7%, ASR +2.6%, CORZ +2.4%, RTX +2.3%, X +2.1% of note.

- Gap Down: CVRX -30.8%, PRAA -2.4%, GBX -2.2% of note.

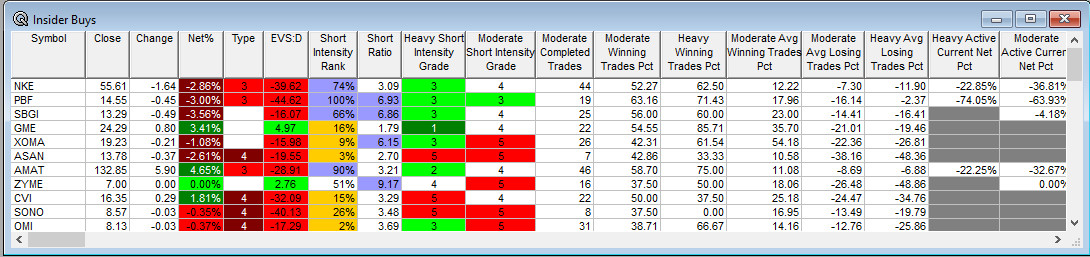

Insider Action: NKE PBF SBGI AMAT see Insider Buying with dumb short selling. None see Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Bloomberg: Stock Futures Soar as Dip Byers Emerge. (Bloomberg)

- Market Wrap: Stocks rebound as Japan sets tone for trade deals. (Bloomberg)

- Five Things To Know Before The Market Opens. (CNBC)

- Bloomberg Big Take: Trump’s Tariff Has Wall Street Facing Harsh Reality. (Bloomberg)

Bolded Royal Blue means behind a Pay Wall.

Economic & Geopolitical:

- Economic Releases:

- March NFIB Small Business Optimism Index was out at 6:00 a.m. EDT and came in at 97.4 from 100.70.

- Weekly API Petroleum Institute Data is due out at 4:30 p.m. EDT.

- Federal Reserve Speakers of note today.

- Federal Reserve San Francisco President Mary Daly speaks at 2:00 p.m. EDT.

- President Trump’s Daily Schedule.

- President Trump participates in a tree planting at 10:30 a.m. EDT.

- Press Briefing at 1:00 p.m. EDT by Karoline Leavitt.

- President Trump participates in an Unleashing American Energy Executive Order Signing Event.

- President Trump delivers remarks at the NRCC Dinner at 6:45 p.m. EDT.

M&A Activity and News:

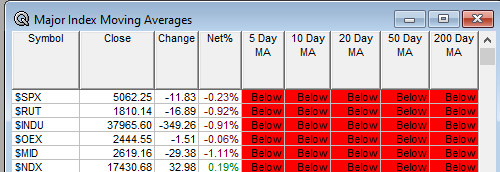

Moving Average Table: Remains at 0%.

Meeting & Conferences of Note: (Not updated today, back tomorrow)

-

- Sellside Conferences:

- BMO CAPP Energy Symposium

- Bradesco Brazil Investment Forum

- Deutsche Bank’s Private FinTech Conference

- Jefferies LatAm Summit

- Jones Healthcare and Technology Innovation Conference

- Needham Healthcare Conference

- Stifel Targeted Oncology Forum

- Sellside Conferences:

-

- Shareholder Meetings: AMGN, AOS, PMN, RAPP

- Top Analyst, Investor Meetings: CGNT

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation:

- Industry Meetings or Events:

- American Academy of Neurology Meeting

- CNBC Changemakers Forum

- NAB Show

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

-

- Upgrades: GPOR ADYYF

- Downgrades:

-

-