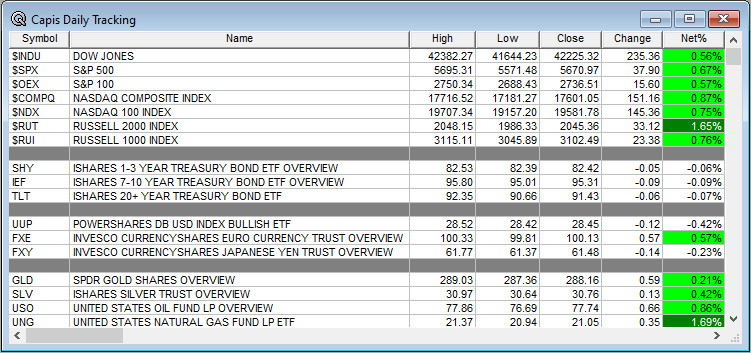

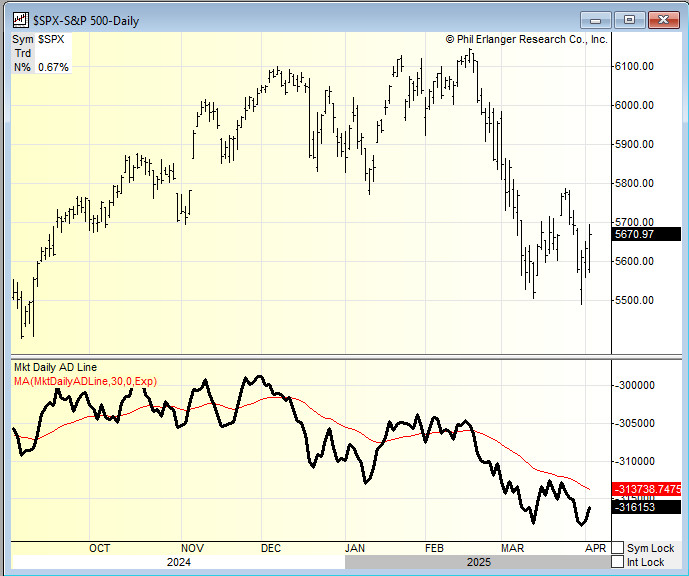

Overnight Summary & Early Morning Trading: The S&P 500 finished Wednesday higher by 0.67% at 5670.97 fromTuesday higher by 0.38% at 5633.07. Futures are lower this morning by -186 (-3.26%) at 5525.50 around 7:20 a.m. EDT. The range is 600 points on the S&P 500 for the year, 5500 to 6100 a drop of 100 points. Thought for the upcoming week: Today is just fugly. Let’s see how the day goes before we overanalyze.

Most Laughable Story From After The Close: Treasury Secretary Bessent says stock selloff about Tech woes. Really????? Not Tariffs???? (CNBC)

Key Events of Note Today:

- Several monthly and weekly economic data points due out see Economic section.

Notable Earnings Out After The Close

- Beats: PENG +0.14 of note.

- Misses: RH -0.34 of note.

- IPOs For The Week: BGIN, ENGS, OMSE, SMA, UYSC, WXM

- New IPOs/SPACs launched/News:

- IPOs Filed/Priced:

- Secondaries Filed or Priced:

- CELZ: FORM S-3 – 1,799,774 Shares of Common Stock

- Notes Priced:

- OMI – Upsize and Pricing of Senior Secured Notes Offering

- Notes Files:

- Convertibles Filed:

- LCID Proposed Convertible Senior Notes Offering

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Private Placements:

- Selling Shareholders of note:

- Mixed Shelf Offerings:

- SER: Form S-3.. $100,000,000 Mixed Shelf

- NAT files for $60 mln common stock offering

News After The Close:

- Trump Tariffs announced after the close sending futures lower. (CNBC)

- Trump Tariffs confirms 25% tariffs on auto imports starting at midnight tonight. (CNBC)

- Trump Tariffs during live press conference shows reciprocal rates: China reciprocal rate at 34%, 20% on EU; 24% on Japan; 32% on Taiwan; 26% on India.

- Trump Tariffs notes baseline tariff of 10% during live press conference.

- Fluor (FLR) receives a letter of intent from one of the world’s leading pharmaceutical makers to provide engineering, procurement and construction management services for its Lebanon, Indiana, mega-project.

- FormFactor (FORM) doubles capacity at Taiwan service center to meet growing demand.

- 10K or Qs Filings/Delays – (Filed), BZAI (Delayed) of note.

Exchange/Listing/Company Reorg and Personnel News:

- HRB names Richard Johnson as Board Chairman, effective April 1.

- PCAR CFO Harrie Schippers to retire, effective June 2; Brice J. Poplawski, VP and Controller, named successor.

Buybacks

- GCT increases share repurchase program by $16 million bringing the total authorization to $62 million

Dividends Announcements or News:

- Stocks Ex Div Today: CSCO PGR MMC PWR TME EC PPC CPB GL MTCH SSD CUZ ABM BDN

- Stocks Ex Div Tomorrow: JPM AXP BMY ROP SYY NTAP IHG MORN RTO RGKD TIMB CHX HASI TWO IGIC HLIO

Stocks Moving After The Close:

Gap Up: SLND +6.2%, NGNE +5.2%, PENG +5.2% of note.

Gap Down: RH -23.7%, FC -18.5%, W -14.3%, WSM -8.8%. LSTR -6.2%, PCAR -5.8%, AAPL -5.8%, AMZN -5.1% of note.

What’s Happening This Morning: (as of 8:25 a.m. EDT) Futures S&P 500 -, NASDAQ -, Dow Jones -, Russell 2000 –. Europe and Asia are lower. Bonds are at 4.07% from 4.146% yesterday on the 10-Year. Crude Oil and Brent Crude are lower with Natural Gas higher. Gold, Silver and Copper lower. The U.S. Dollar is lower versus the Euro, lower against the Pound and lower against the Yen. Bitcoin is at $83,105 from $84,965 lower by $3,364 at -3.88%.

- Daily Positive Sectors: Consumer Cyclicals, Industrials, Financials, Healthcare and Technology.

- Daily Negative Sectors: Communication Services led the way lower.

- One Month Winners: Energy and Utilities of note.

- Three Month Winners: Energy, Materials, Healthcare, Utilities and Financials of note.

- Six Month Winners: Financials, Energy, Consumer Defensive, Communication Services and Utilities of note.

- Twelve Month Winners: Utilities, Financials, Communication Services, Consumer Defensive, Real Estate and Technology of note.

- Year to Date Winners: Energy, Materials, Healthcare, Utilities, Financials, Consumer Defensive and Real Estate of note.

Bolded means the Sector is new to the period in which it falls.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Thursday After the Close:

- Friday Before The Open: GBX

Notable Earnings of Note This Morning:

- Flat: None of note

- Beats: ANGO +0.05, BB +0.03 of note.

- Misses: None of note.

- Still to Report:

Company Earnings Guidance:

- Positive Guidance: LNN +0.55, AYI +0.04, MSM +0.04 of note.

- Negative or Mixed Guidance: Noneof note.

Advance/Decline Daily Update: The A/D continues to struggle.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: PENG +4.5%, SSTK +3.6%, SNY +3.3%, HVT +2.1%, SLND +2%, NVS +2% of note.

- Gap Down: RH -27.3%, RXST -23.4%, UMH -20.3%, W -15.3%, FC -12.2%, RLI -10.8%, WSM -9.1%, LZB -8.3%, AAPL -7.5%, LNW -7.5%, AMZN -5.9%, LCID -5.8%, NVDA -5%, TSLA -4.9%, IWM -4.5%, FLR -4.3%, META -4.2%, QQQ -3.7%, GCT -3.6%, SPY -3.3%, DIA -2.7%, LSTR -2.7%, GOOG -2.6%, NAT -2.5%, MSFT -2.3%, UNIT -2.3%, FORM -2.3%, PCAR -2.1% of note.

Insider Action: FLWS and ADVM see Insider Buying with dumb short selling. BNTC sees Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Bloomberg: Trump Tariff Threat To Global Economy Send Oil, Dollar Lower. (Bloomberg)

- Stocks Making The Biggest Moves: Not out yet. (CNBC)

- Layoff announcements the highest since the pandemic. (CNBC)

- Microsoft pulls back on data center production. (Bloomberg)

- Five Things To Know Before The Market Opens. (CNBC)

Bolded Royal Blue means behind a Pay Wall.

Economic & Geopolitical:

- Economic Releases:

- Weekly Jobless Claims are due out at 8:30 a.m. EDT.

- February Trade Balance is due out at 8:30 a.m. EDT and is expected to fall to $121 billion from $-131.4 billion.

- March ISM Services are out at 10:00 a.m. EDT and are expected to fall to 52.80% to 53.20%.

- Weekly Natural Gas Inventories are out with its update at 10:30 a.m. EDT.

- Federal Reserve Speakers of note today.

- Federal Reserve Vice Chairman Phillip Jefferson speaks at 12:30 p.m. EDT.

- Federal Reserve Governor Lisa Cook speaks at 2:30 p.m. EDT.

- President Trump’s Daily Schedule.

- President Trump receives intelligence briefing at 1:00 p.m. EDT.

- President Trump heads to Florida for LIV Gold Dinner at 7:30 p.m. EDT and then head to Mar-a-Lago.

M&A Activity and News:

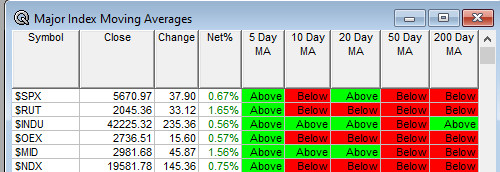

Moving Average Table: Moves from 0% to 40%.

Meeting & Conferences of Note: (Not updated today, back tomorrow)

-

- Sellside Conferences:

- Gabelli Waste & Sustainability Symposium

- H.C. Wainwright AI Based Drug Discovery & Development Conf

- Jefferies Power x Data Virtual Conference

- JP Morgan Napa Valley Biotech Forum

- JP Morgan Retail Round Up

- Morgan Stanley Latin America Executive Conference

- RBC Capital Ophthalmology Conference

- Wolfe/Nomura Clean Energy Infrastructure Conference

- Sellside Conferences:

-

- Shareholder Meetings: FCEL, RIO, SUNE

- Top Analyst, Investor Meetings: BUR, RNXT

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation:

- ALDX: PDUFA Decision for Reproxalap

- EWTX: Data Presentation for EDG-7500

- Industry Meetings or Events:

- AD/PD 2025 Alzheimer’s & Parkinson’s Diseases Conference

- A.G.P.’s Energy Conference

- AI-Powered E-Commerce Seller Summit

- Inaugural Case-to-Closure User Summit

- ISC West

- Optical Fiber Communications Conference and Exhibition

- OpenText Summit Munich

- Van Lanschot Kempen European Real Estate Seminar

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

-

- Upgrades: TJX ROST JHG BJ

- Downgrades: RXST GWW USB LYFT

-

-