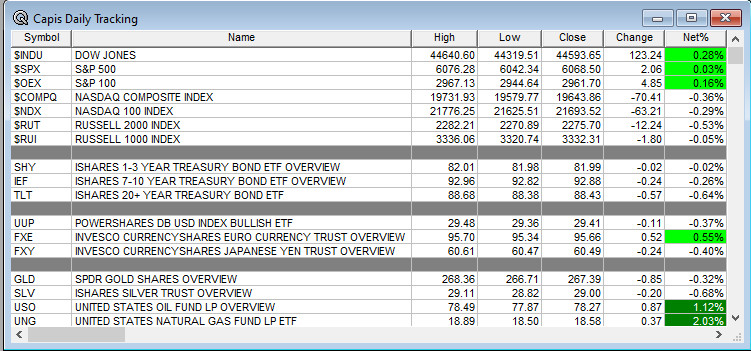

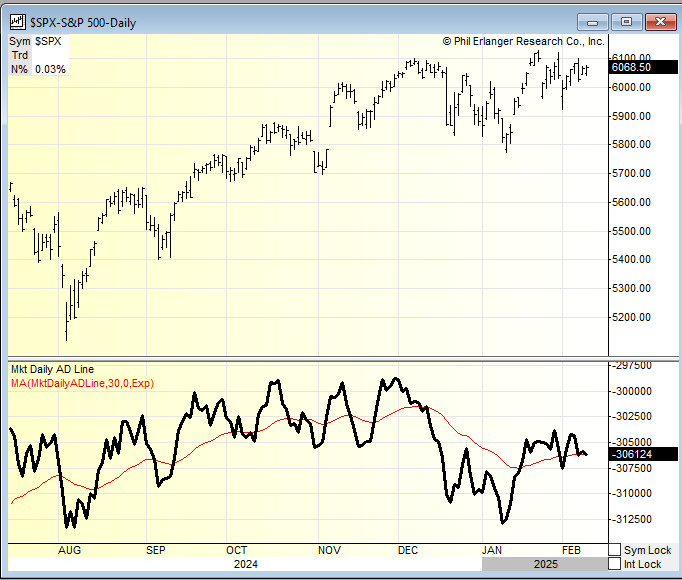

Overnight Summary & Early Morning Trading: The S&P 500 finished Tuesday higher by +0.03% at 6068.50. Monday higher by +0.67% at 6066.44. The overnight high was hit at 6096.50 at 7:45 p.m. EDT and the low was hit at 6075.25 at 4:20 a.m. EDT. The overnight range is 21 points. The current price is lower at 7:10 a.m by -0.11% at 6085.75 down -6.50 points.

Executive Summary: Stocks bounced off Friday’s weakness on Monday which is 2025 pattern. Can the S&P 500 clear 6100 this week?

Articles of Note:

*Note that certain articles highlighted may require a subscription. We highlight noted sources like the WSJ or Bloomberg that have wide audiences.

Key Events of Note Today:

-

- CPI is due out at 8:30 a.m. EDT and the latest Treasury update is due at 3:00 p.m. EDT.

- Weekly Crude Oil Inventories are due out at 10:30 a.m. EDT.

- 10- Year Note Auction at 1:00 p.m. EDT.

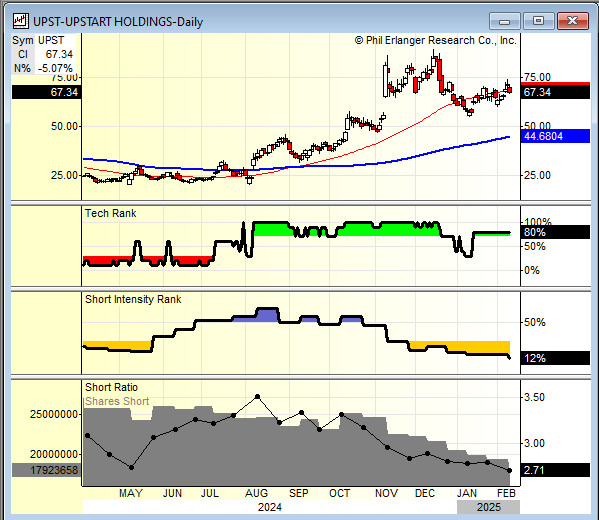

Upstart (UPST) beat estimates by $0.30, earning $0.26. The stock is higher by 27% this morning. This names is not going up on a short squeeze as Short Intensity is low.

Notable Earnings Out After The Close

- Beats: AIZ+1.41, CRSP +0.75, UPST +0.30, PBI +0.18, GILD +0.16, EXEL +0.12, TDC +0.10, ALSN +0.10, LYFT +0.07, AIG +0.06, PRI +0.05, OS +0.05, of note. (>+0.05)

- Flat: None of note.

- Misses: CAR -54.56, IAC -2.63, STAA -0.37, DIOD -0.09, SAGE -0.08, ET -0.08, BL -0.03, ECG -0.02, DASH -0.01 of note.

- IPOs For The Week: BTAI, GSAT, KORU, NEXN, NIVF, RIME, SCCO,

TCBP - New IPOs/SPACs launched/News:

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced:

- DEC files ordinary share offering.

- Notes Priced:

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders of note:

- DAL files for 9,216,343 shares of common stock offering by selling shareholder.

- Mixed Shelf Offerings:

- NLSP: Form F-3.. $75,000,000 Mixed Shelf

- ZWS files mixed shelf securities offering.

- RNST files mixed shelf securities offering.

- PIPE:

- Convertible Offerings & Notes Filed:

- SMCI announces private placement of $700.0 million of new 2.25% convertible senior notes due 2028 and amendments to existing 0.00% convertible senior notes due 2029

Biggest Movers Up & Down Yesterday:

- Movers Up: UPST +23.5%, CFLT +13.4%, FRSH +10.2%, DASH +5.9% of note.

- Movers Down: SPIR -47.1%, BL -14.8%, TDC -14.5%, LYFT -10.2%, ALSN -9%, ZG -6.4% of note.

News After The Close:

- IVZ reports preliminary month-end assets under management (AUM) of $1,902.8 billion, an increase of 3.1% versus previous month-end.

- Intercontinental Exchange (ICE) and Reddit (RDDT) announce an agreement for Intercontinental Exchange to leverage Reddit’s Data API to research, create and distribute new data and analytics products for the financial industry.

- Granite Construction (GVA) has been awarded a $78 mln infrastructure project by the California Department of Transportation in Orange County, California.

- Spire Global (SPIR) in 8-K filing: there is substantial doubt about the company’s ability to continue as a going concern.

- Super Micro Computer (SMCI) delays 10-Q filing; in late 2024, received subpoenas from DOJ and SEC requesting documents following short seller report; SMCI is cooperating with these document requests.

- Ford Motor (F) earlier today will warn Congress of devastating tariff impact. (Bloomberg) ]

- Fox Corporation (FOXA): Super Bowl LIX had the largest audience for a single-network telecast in TV history. (Nielsen)

- 10K or Qs Delays – SMCI of note.

Exchange/Listing/Company Reorg and Personnel News:

- PBI appoints Bob Gold as CFO, effective March 10.

Buybacks:

Dividends Announcements or News:

- Stocks Ex Div Today: XOM TGT PCAR URI KVUE TTEK LEVI BOKF OMF HOMB AROC NXST ST SASR WT WINA WLFC.

- Stocks Ex Div Tomorrow:

- GILD increases quarterly cash dividend 2.6% to $0.79/share from $0.77/share.

- KNSL increases quarterly cash dividend to $0.17/share from $0.15/share.

- WAFD increases quarterly cash dividend to $0.27/share from $0.26/share.

What’s Happening This Morning: (as of 8:15 a.m. EDT) Futures S&P 500 -2, NASDAQ+30.75, Dow Jones -51 and Russell 2000 +9.20. Europe is mixed with Asia mixed as well. Bonds are at 4.541% from 4.535% yesterday on the 10-Year. Crude Oil and Brent Crude are lower with Natural Gas lower as well. Gold and Silver lower and Copper higher. The U.S. Dollar is lower versus the Euro, lower against the Pound and higher against the Yen. Bitcoin is at $96,141 from $97,826 higher by $1009 up by +1.05%. Additional Comments:

- Daily Positive Sectors: Consumer Defensive, Energy, Real Estate, Financials and Utilities were higher.

- Daily Negative Sectors: Consumer Cyclicals, Healthcare, Materials and Communication Services of note.

- One Month Winners: All except for Technology of note.

- Three Month Winners: Communication Services, Consumer Cyclical, Financials and Technology of note.

- Six Month Winners: Consumer Cyclical, Financials, Communication Services, Technology, Utilities and Industrials of note.

- Twelve Month Winners: Technology, Communication Services, Financials, Consumer Cyclical and Utilities note.

- Year to Date Winners: Communication Services, Materials, Financials, Healthcare and Utiltities of note.

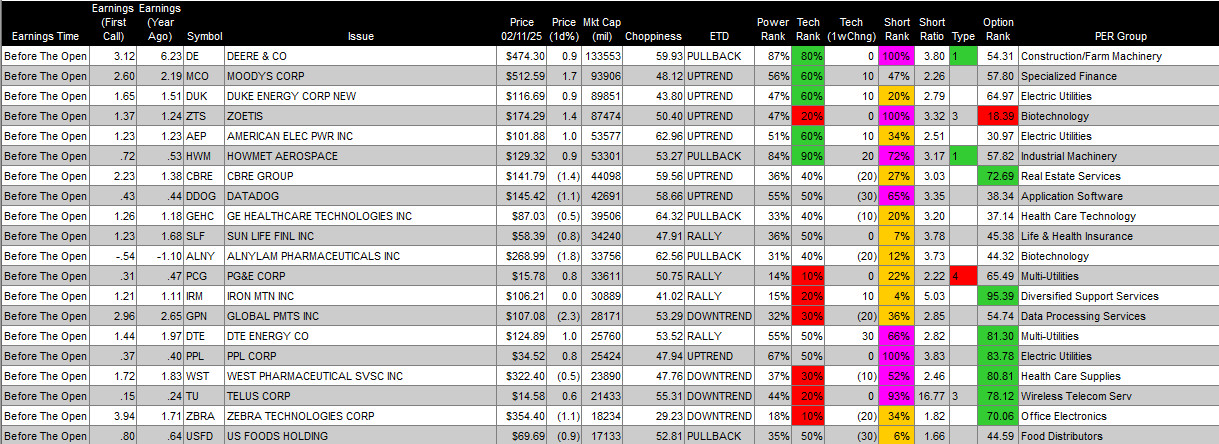

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Wednesday After the Close:

- Thursday Before The Open:

Notable Earnings of Note This Morning:

- Beats: LAD+0.62, THC +0.50, ALKS +0.29, CVS +0.28, GNRC +0.28, MLM +0.23, SPTN +0.10, BIIB +0.09, CME +0.07 , R +0.07, KHC +0.06, EXC +0.05 of note.

- Flat: None of note.

- Misses: SW-0.37, SITE -0.20, IPG -0.06, WAB -0.05, DENN -0.01 of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: of note.

- Negative or Mixed Guidance: of note.

Advance/Decline Daily Update: The A/D fell to major support making new lows and now is off those lows.

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up: UPST +27.5%, ANAB +23.8%, MCY +20.7%, CFLT +14.6%, FRSH +8.9%, HIW +8.7%, PBI +8.6%, ELMD +8.4%, ANGI +8.1%, BHF +8.1%, LAD +6.9%, DASH +6.8%, SMCI +6.6%, GNRC +5.8%, UFCS +5.7%, GILD +5%, EW +4.7%, AKR +3.5%, RDWR +3.5%, IAC +3.3%, VLN +2.9%, HIVE +2.9%, CPA +2.8%, HP +2.8%, ULCC +2.8%, MXCT +2.7%, SWTX +2.7%, BVN +2.7%, CRSP +2.3%, RDDT +2.2%, RRR +2.1%, MIR +2% Of note.

- Gap Down: SPIR -51.2%, STAA -36.7%, SMWB -26.2%, OS -19%, TDC -13.3%, BL -12.9%, LYFT -12.4%, ZG -8.9%, ALSN -8%, VRT -4.9%, BCAX -3.6%, CAR -3.6%, ZWS -3.4%, DIOD -2.9%, SAGE -2.5%, KRG -2.1% of note.

Insider Action: None see Insider Buying with dumb short selling. None see Insider Buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Lead Story on Bloomberg: A Hot Inflation Report Is Set To Derail The S&P 500 Run. (Bloomberg)

- Market Wrap: US Stock futures muted before inflation data. (Bloomberg)

- Stocks Making The Biggest Moves: Check back later not out yet. (CNBC)

- President Trump says interest rates should be lowered to go “hand in hand” with tariffs. (CNBC)

- Five Things To Know Before The Market Opens. (CNBC)

- Zelle passes Paypal (PYPL) in payments. (CNBC)

- Bloomberg: The Big Take: China’s Property Crisis Enters A Dangerous new Phase. (Podcast)

Economic:

- January CPI is expected to fall to 0.30% from 0.40% when released at 8:30 a.m. EDT.

- The latest Treasury Budget update is due out at 2:00 p.m. EDT and came in last month at $-87 billion.

- Weekly MBA Mortgage Applications rose +2.3% for the week.

- Weekly Crude Oil Inventories are due out at 10:30 a.m. EDT.

Geopolitical: (Watch our Twitter feed, Bullet86, for any impromptu appearances)

- President Trump’s Daily Schedule.

- Press Briefing at 1:00 p.m. EDT.

- President Trump signs Executive Orders at 2:30 p.m. EDT.

- Federal Reserve Chairman Powell begins day two of testimony on the Hill at 10:00 a.m. EDT.

- Federal Reserve Atlanta President Raphael Bostic speaks at 12:00 p.m. EDT.

- Federal Reserve Governor Christopher Waller speaks at 5:05 p.m. EDT.

M&A Activity and News:

- .

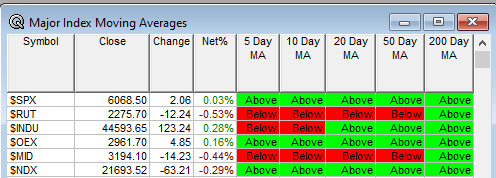

Moving Average Table: Drops to 67% from 70%.

Meeting & Conferences of Note:

-

- Sellside Conferences:

- Baird Private Company Technology & Services Conference

- Bank of America US Financial Services Conference

- BTIG MedTech Digital Health Life Sience & Diagnostic Tools Conference

- Cantor Healthcare Ski Summit

- Citi India Investor Conference

- Oppenheimer Healthcare Life Sciences Conf

- Stifel Transportation & Logistics Conference

- UBS Financial Services Conference

- Wolfe Research Auto, Auto Tech and Semiconductor Conference

- Sellside Conferences:

-

- Shareholder Meetings: CENT, PTC

- Top Analyst, Investor Meetings: FBLG, IPXX, MAMA, WDC, WAT

- Update: None of note.

- Fireside Chat

- R&D Day: None of note.

- FDA Presentation: BEAM: Data Presentgation on BEAM-101

- Industry Meetings or Events:

- AHR Expo

- BIO CEO & Investor Conference

- C2C User Summit

- Cisco Live

- Connected Health & Fitness Summit

- Descartes Innovation Forum

- Nuclear Financing Summit

- SEALSQ Quantum Day

- Western Society of Allergy Asthma & Immunology Annual Scientific Session

Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

-

- Upgrades: GFS ERO UPST MCY

- Downgrades: EDR BBD

-