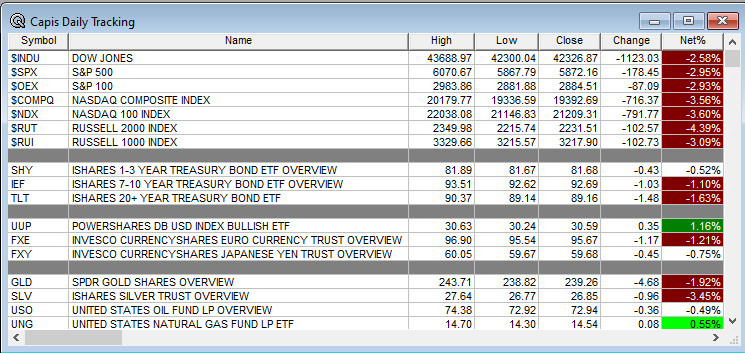

Overnight Summary & Early Morning Trading: The S&P 500 closed Wednesday lower by -2.95% at 5872.16. Tuesday lower by -0.39% at 6050.61. The overnight high was hit at 5972 at 5:25 a.m. EDT and the low was hit at 5906.50 at 4:05 p.m. EDT. The overnight range is 66 points. The current price is higher at 6:55 a.m by 0.44% up +26.00.

Articles That Matter: “Market rout shows stocks are finally catching up to what bonds have been saying. ” by Bob Pisani. (CNBC)

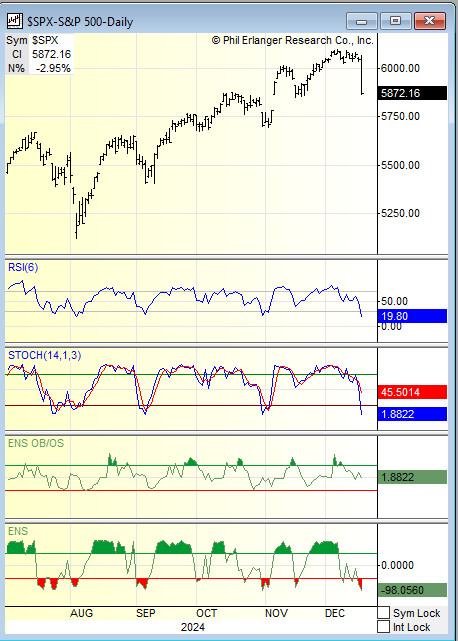

Executive Summary: Yesterday was ugly as you will see below. The S&P 500 fell -2.98% while the NASDAQ 100 lost -3.60% and the Russell 2000 -4.39%. With that said, we are now oversold. Watch for a video on markets later today, maybe after the close. RSI under 30 is oversold as are Stochastics under 20 and ENS under -50.

Key Events of Note Today:

-

- There are five economic releases out from 8:30 a.m. through 10:30 a.m. EDT.

- 5-Year TIPS Auction at 1:00 p.m. EDT.

Daily Chart Request: Want to see an Erlanger Chart in The Morning Note? Simply send an email to us at [email protected] and we will more than likely show it.

Darden Restaurants (DRI) beat estimates by $0.01 and raised guidance for FY 25. Olive Garden and Longhorn are doing great. How does it rank in the work? Note that short sellers have caught this drop. Historically, Shorts get squeezed 73% of the time, and this looks like one more time. Now the Short Intensity is at 94%. The technical rank is weak at 30% today but will improve with the bounce today as the stock is trading at $174 higher by $14.13 which is 8.84%. We have this ranked as a Type 3 Shorts Correct.

Notable Earnings Out After The Close

- Beats: GIS +0.18, JBL +0.12, SCS +0.08, BIRK +0.03 of note.

- Flat: TTC of note.

- Misses: None of note.

- IPOs For The Week: ALEH, FTRK, HIT, MIMI, MTRS, NTCL, PHH, YSXT

- New IPOs/SPACs launched/News: None of note.

- IPOs Filed/Priced: None of note.

- Secondaries Filed or Priced:

- ZCMD: Form F-3.. 19,600,000 Class A Ordinary Shares

- COSM: Form S-1 Common Stock and Warrants

- INSG: Form S-1.. UP TO 5,956,241 shares of common stock.

- Notes Priced:

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders of note:

- Mixed Shelf Offerings:

- FCCO files $75 mln mixed shelf securities offering.

- MVBF files $75 mln mixed shelf securities offering.

- AAOI files mixed shelf securities offering.

- QNCX files a $200 mln mixed shelf offering.

- MGLD files a $100 million mixed shelf offering.

- JFBR files a $50 million mixed shelf offering.

- PIPE:.

- Convertible Offerings & Notes Filed:

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down Yesterday:

- Movers Up: MESO +45.7%, BILL +5.1%, LII +3% of note.

- Movers Down: WS -14.6%, MU -13.2%, MLKN -9.6%, LEN -6.8%, EPAC -4.3%, TPVG -4.1%, WDC -4% of note.

News After The Close:

-

- 10-K Delays – PPIH of note.

- Palantir Technologies (PLTR) expands army vantage partnership with $618.9 mln contract.

- Micron (MU) missed on earnings and revenues.

- Lennar (LEN) missed on earnings and revenues.

- Trane (TT) signs definitive agreement to acquire BrainBox AI, a developer of autonomous HVAC controls and generative Artificial Intelligence building technology.

- National Bank (NBHC) announces balance sheet repositioning; co sold ~ $130 million of available-for-sale investment securities on the open market.

- EQTY Lab, in collaboration with Intel (INTC) and NVIDIA (NVDA), announced today the release of the Verifiable Compute AI framework, the first hardware-based solution to govern and audit AI workflows.

- Raymond James (RJF) client assets under administration grew 21% yr/yr and 4% over the preceding month.

- Sonoco Products (SON) to sell its Thermoformed and Flexibles Packaging business to TOPPAN Holdings for $1.8 bln.

- NOC awarded $3.46 bln U.S. Navy contract.

- Index Changes:

- S&P MidCap 400 constituent Lennox International (LII) will replace Catalent (CTLT) in the S&P 500.

- BILL Holdings (BILL) will replace Lennox International in the S&P MidCap 400 effective prior to the opening of trading on Monday, December 23.

Buybacks

- EQT approves a two-year extension to its existing share repurchase program originally announced on December 13, 2021.

- TPH announces $250 mln stock repurchase program.

- SSNC approves renewal of repurchase program; may purchase up to ~ 2.1% of its outstanding common shares beginning January 21, 2025 until January 21, 2026.

Exchange/Listing/Company Reorg and Personnel News:

- EVH appoints Dr. Von Nguyen as Chief Medical Officer, effective January 1; will succeed Dr. Andrew Hertler.

- TPVG appoints Mike Wilhelms as CFO, effective Jan 6.

- FE appoints Brian Tierney as Chair of the Board, effective Jan 1.

- GO appoints Christopher Miller as CFO, effective January 6; succeeds Lindsay Gray, who has been serving as Interim CFO.

- AMWL announces that CFO Mark Hirschhorn will take on an expanded role as COO, effective Jan. 1, 2025.

Dividends Announcements or News:

- Stocks Ex Div Today: CINF UWMC SNV VAC KLIC ELME SWBI NRIM OFLX

- Stocks Ex Div Tomorrow: GEV BTI CARR PCAR VST FERG HPE IFF PKG OMC MAIN KFY PLTK ROIC CNMB ALEX TPB GDEN HCKT GSM GOOD GLAD GMRE.

- NWFL increases quarterly cash dividend to $0.31/share from $0.30/share.

What’s Happening This Morning: (as of 8:00 a.m. EDT) Futures S&P 500 +40, NASDAQ +133, Dow Jones +253 and Russell 2000 + . Europe is lower with Asia lower as well. Bonds are at 4.53% from 4.41% on the 10-Year. Crude Oil and Brent are lower with Natural Gas higher. Gold, Silver and Copper lower. The U.S. Dollar is lower versus the Euro, lower against the Pound and higher against the Yen. Bitcoin is at $102,299 from $104,966 higher by $1135 +1.10%.

- Daily Positive Sectors: No sectors were higher yesterday.

- Daily Negative Sectors: All sectors were lower with no discrimination.

- One Month Winners: Consumer Cyclicals, Financials, Industrials, Energy and Utilities of note.

- Three Month Winners: Consumer Cyclicals, Financials, Communication Services, Industrials, Utilities, Consumer Defensive and Technology of note.

- Six Month Winners: Financials, Real Estate, Utilities, Consumer Cyclical and Technology of note.

- Twelve Month Winners: Financials, Technology, Industrials, Utilities and Communication Services note.

- Year to Date Winners: Technology, Financials, Utilities, Communication Services and Industrials of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Thursday After the Close:

- Friday Before The Open:

Notable Earnings of Note This Morning:

- Beats: ACN +0.17, KMX +0.19, FDS +0.09, CAG +0.03, DRI +0.01 of note.

- Flat: None of note.

- Misses: LW -0.35 of note.

- Still to Report: CTAS PAYX of note.

Company Earnings Guidance:

- Positive Guidance: SCS of note.

- Negative or Mixed Guidance: CAG MU of note.

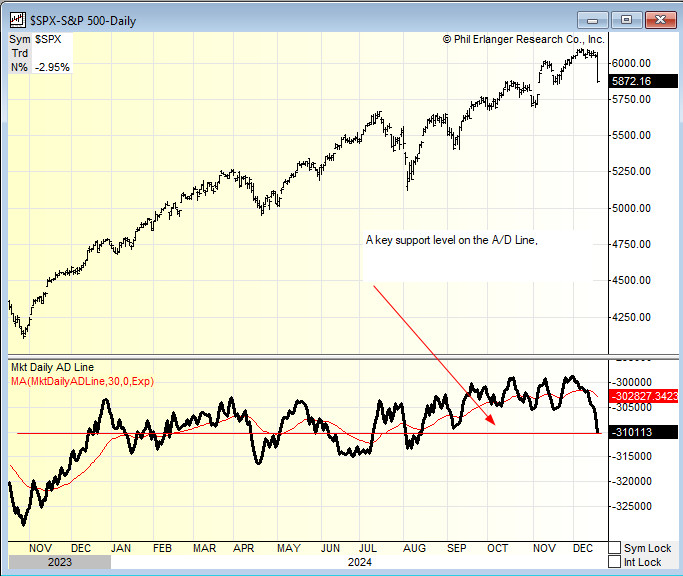

Advance/Decline Daily Update: SPX A/D is has fallen to major support. A bounce or a puke ahead?

Gap Ups & Down In Early Pre-Market: (+2% or down more than -2%):

- Gap Up:

- Gap Down:

Insider Action: No stocks see Insider buying with dumb short selling. No stocks see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Lead Story on Bloomberg: Trump and Musk Threaten US Shutdown and Shake Up Republican Party. (Bloomberg)

- Market Wrap: US Stocks poised to bounce back after Fed Jolt. (Bloomberg)

- 5 Things To Know Before The Market Opens. (CNBC)

- Stocks Making The Biggest Moves Pre-Market: . (CNBC)

- Bank of England holds rates steady. (CNBC)

- Darden (DRI) up 10% on strong sales at Olive Garden and Longhorn Steaks. (CNBC)

Economic:

- Third Quarter GDP (final estimate) is due out at 8:30 a.m. EDT and is expected to stay at 2.80%.

- November Existing Home Sales are due out at 10:00 a.m. EDT and expected to rise to 4.10 million from 3.96 million.

- November Leading Indictors are expected to improve but not turn positive moving to -0.10% from -0.40%.

- Weekly Jobless Claims are due out at 8:30 a.m. EDT.

- Weekly Crude Oil Inventories out at 10:30 a.m. EDT.

Geopolitical: (Watch our Twitter feed, Bullet86, for any impromptu appearances)

- President Biden will receive the Daily Briefing at 10:00 a.m. EDT.

- Fed Blackout Period has ended.

M&A Activity and News: None of note.

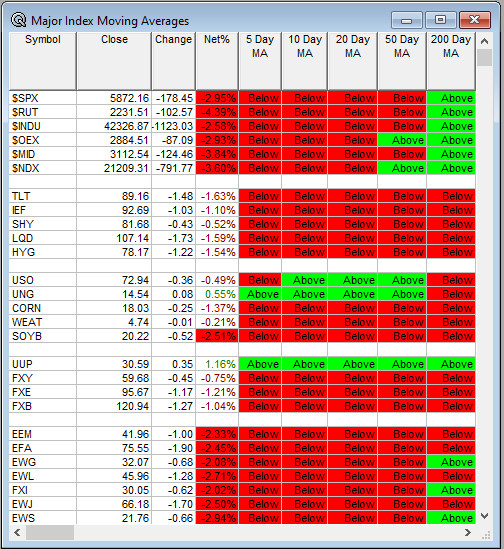

Moving Averages On Major Equity Indexes: Moves to 33% from 60%. Last time I checked the color of money is green, not red. Pretty ugly.

Meeting & Conferences of Note:

-

- Sellside Conferences:

- Goldman Sachs Energy Clean Tech & Utilities Conference

- Goldman Sachs Catalyst Clinic

- Needham Growth Conference

- Sellside Conferences:

-

- Fireside Chat: None of note.

- Top Analyst, Investor Meetings: AGCO, PECO, PROP

- Shareholder Meetings: BTM, CELU, DRIO, FDS, GLSI, NYXH, ONMD, TPCS, XYF

- Update: None of note.

- R&D Day: None of note.

- FDA Presentation:

- Company Event: None of note.

- Industry Meetings or Events:

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

-

- Upgrades: LPLA KULR HPE DTM CGTX AFRM

- Downgrades: IMO AI