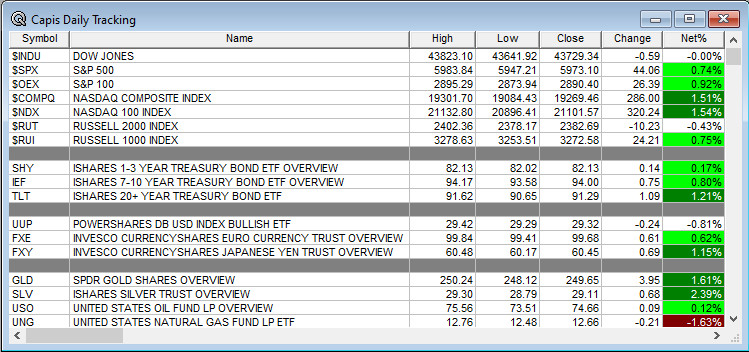

Overnight Summary: The S&P 500 closed Thursday higher by 0.74% at 5973.10 from Wednesday higher by 2.53% at 5929.04. The overnight high was hit at 6009.75 at 12:50 a.m. EDT and the low was hit at 5990.25 at 6:05 a.m. EDT. The overnight range is 20 points. The current price is 5996.50 at 6:55 a.m. EDT lower by -7.25 points lower by -0.12%.

Executive Summary: Well, the Federal Open Market Committee (FOMC) concluded its two-day meeting and Chairman Powell hosted a Press Conference at 2:30 p.m. EDT. What did we learn?

The consensus was that they would cut by 25 basis points and that is exactly what they did. Watch TLT to see if yields continue to climb.

Key Events of Note Today:

- Economic releases of note today include the University of Michigan Consumer Sentiment and weekly Baker Hughes Rig Count.

Notable Earnings Out After The Close

- Beats: INVX +1.66, CICVI +1.02, OVV +0.75, QDEL +0.58, MSI +0.36, ANET +0.32, PODD +0.30, INGN +0.25, SOLV +0.25, DXC +0.21, MTD +0.20,YELP +0.14, ZD +0.13, BILL +0.12, RRR +0.12, EOG +0.11, FTNT +0.11, FNKO +0.10 of note. (greater than +0.10)

- Flat: None of note.

- Misses: ETNB -0.77, BLNK -0.70, EVH -0,55, BHF -0.50, U -0.45, TDW -0.20, DKNG -0.19, AMRC -0.19, RIVN -0.12, BE -0.09. (lower than -0.09)

- IPOs For The Week: ADUR, ALEH, CASK, CGTL, HIT, JUNS, LEC, MSW, PHH, WYHG

- New IPOs/SPACs launched/News:

- IPOs Filed/Priced:

- Secondaries Filed or Priced:

- TVTX announces proposed public offering

- CUZ has commenced an underwritten public offering of 6,000,000 shares of its common stock

- GEHC announces the launch of a secondary underwritten public offering of 13,281,302 shares of its common stock

- HL files common stock offering; resale 1,000,000 shares of common stock contributed to the Hecla Mining Company Retirement Plan Trust and the Lucky Friday Pension Plan Trust

- ESTA announces $50 million registered direct offering

- VLY announces a proposed public offering of shares of its common stock, no par value

- Notes Priced:

- Direct Offering:

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders of note:

- INFA announces the commencement of a proposed underwritten registered secondary offering of 16,000,000 shares of its Class A common stock by certain funds associated with Permira and Canada Pension Plan Investment Board

- ACHV files for 3,488,727 shares of common stock offering by selling shareholders

- VTYX files for 7,060,100 shares of common stock offering by selling shareholder

- Mixed Shelf Offerings:

- AVIR files $500 mln mixed shelf securities offering

- INFA files mixed shelf securities offering

- RDFN files mixed shelf securities offering

- TRML files $350 mln mixed shelf securities offering

- PIPE:

- PACB announces a private convertible exchange transaction of $459 mln principal amount of 1.50% convertible senior notes due 2028

- Convertible Offerings & Notes Filed:

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down After The Close:

- Movers Up: DOCS +38%, LITE +24%, FIVN +22.1%, UPST +19%, TOST +17.1%, ALRM +11.7%, CARG +11.5%, SYNA +6.8% of note.

- Movers Down: EVH -35%, RDFN -13.9%, PINS -12.2%, TTD -10.3% of note.

News After The Close:

- Bloom Energy (BE) announces a landmark project to deliver fuel cells to the largest single-site installation to date in history

- YELP to acquire RepairPal for $80 mln in cash, close by year end.

- BlackRock (BLK) in early-stage discussions with Millennium about a strategic partnership, may take equity stake

- AMC announces AMC’s Go Plan; to invest up to $1.5 bln over 4-7 years

- 10-K Delays – TRMB

- Barron’s: China unveils $1.4 trillion stimulus package for local goivernments. (Barron’s)

- NVDA and SHW to start trading on the Dow Jones Industrials Averae. Bye Bye INTC DOW.

Buybacks or Repurchases:

- DVAX announces $200 million share repurchase program

- EG announces that its Board of Directors approved an increase of 10 mln shares in its share repurchase authorization

- UVV announces $100 mln share repurchase program

- CPAY announcing today an increase in the share repurchase authorization by $1 billion, as authorized on November 5, 2024

- TRIN announces $30 mln stock repurchase program

- EOG approves $5.0 bln increase to its authorization for opportunistic share repurchases

Exchange/Listing/Company Reorg and Personnel News:

- COLL announces that Vikram Karnani has been appointed as President and Chief Executive Officer of Collegium and will join its Board of Directors effective November 12, 2024

- BL announces planned retirement of CFO Mark Partin and appointment of Chief Accounting Officer, Patrick Vollanova as successor; effective March 1, 2025

- REZI announces that Jay Geldmacher, President and CEO, informed the Board of his intention to retire from his executive and Board roles in 2025, current Vice-Chair, Andrew Teich, to become Chairman

- EFX announces that Mark Begor will continue to serve as CEO beyond the current expiration of his employment agreement in 2025

- NWSA announces that Susan Panuccio will step down from her role as CFO on January 1, 2025, and will be succeeded by Lavanya Chandrashekar

- NGS appoints Ian Eckert as its new CFO, effective no later than January 6, 2025

Dividends Announcements or News:

- Stocks Ex Div Today: AAPL WFC HSBC PFE UL SCHW COP BH BP ET TFC GWW AEP AMX MPLX LNG HWM EXC OWL JBHT MAS TECH LAD X SUN SSB JHG MGY SON LAZ MAIN MWA TEX.

- Stocks Ex Div Tomorrow:

- RLI declares a special cash dividend of $4.00/share

- EOG increases quarterly cash dividend 7% to $0.975/share from $0.91/share

- ACGL declares a special cash dividend of $5.00/share

What’s Happening This Morning: Futures S&P 500 -2.60 NASDAQ -46 Dow Jones +32 Russell 2000 +3.41 (at 8:25 a.m. EDT). Asia is higher ex China and Europe is lower. VIX Futures are at 16.01 from 16.05 yesterday while Bonds are at 4.312% from 4.428% on the 10-Year. Crude Oil and Brent are lower with Natural Gas higher. Gold, Silver and Copper lower. The U.S. Dollar is higher versus the Euro,higher versus the Pound and lower against the Yen. Bitcoin is at $76,077 from $74,800 lower by -563 down -0.74% this morning.

- Daily Positive Sectors: Technology, Communication Services, Consumer Cyclicals and Materials of note.

- Daily Negative Sectors: Financials and Industrials of note.

- One Month Winners: Financials, Communication Services, Technology and Consumer Cyclicals of note.

- Three Month Winners: Consumer Cyclicals, Technology, Financials, Communication Services of note.

- Six Month Winners: Technology, Utilities, Real Estate, Financials and Communication Services of note.

- Twelve Month Winners: Technology, Financials, Utilities, Communication Services and Industrials note.

- Year to Date Winners: Technology, Utilities, Financials, Industrials and Communication Services of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Friday After the Close:

- Monday Before The Open:

Notable Earnings of Note This Morning:

- Beats: SONY +15.90, FLGT +0.46, MSGE +0.39, AXL +0.25, PARA +0.25, TU +0.11, PAA +0.06 of note. (greater than +0.05)

- Flat: None of note.

- Misses: FLR -0.25, WMS -0.19, NRG -0.10, GTN -0.09 of note.

- Still to Report:

Company Earnings Guidance:

- Positive Guidance: SONY FLGT ANIP of note.

- Negative or Mixed Guidance: AXL LAMR BAX BLMN HLLY GTN WMS of note.

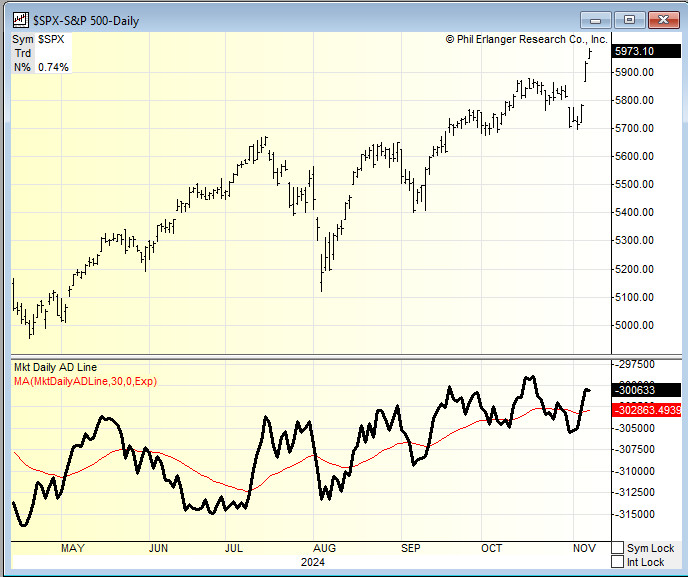

Advance/Decline Daily Update: The A/D Line continues its rebound.

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: DOCS +44.5%, LITE +24%, UPST +23.3%, FIVN +22.6%, SEZL +21.3%, TOST +16%, WBTN +15.9%, AXON +15.2%, BILL +13.5%, ALRM +12.9%, GHM +11.7%, INGN +11%, FTRE +10.8%, ADMA +10.7%, GCT +10.1%, CARG +9.4%, INDI +8.5%, QDEL +8.4%, AAOI +8.4%, FLYW +8.2%, G +7.5%, ADPT +6.6%, GRND +6.3%, SONY +5.9%, VCTR +5.5%, VEEV +5.3%, PBI +5%, DH +4.9%, ASAI +4.9%, PRA +4.8%, DXC +4.6%, INVX +4.4%, NRG +4.3%, AAON +4.2%, LCID +4.1%, EXPE +4%, DIOD +3.9%, ACVA +3.8%, COLL +3.7%, VTYX +3.6%, DVAX +3.4%, MSI +3.2%, OPEN +3.2%, KURA +3%, ETNB +2.8%, AMPL +2.5%, PTCT +2.4%,

- GapDown: EVH -35%, AGL -30.8%, MRVI -26.7%, SG -16.7%, RDFN -14.1%, RVNC -13.8%, ESTA -13.3%, SEMR -13.2%, PACB -12.7%, FLR -12.6%, PINS -12%, CNH -12%, TDW -11.7%, FIGS -11.4%, ARLO -11.1%, BLNK -10.4%, WMS -9.2%, GETY -8.5%, TTD -8.4%, LTRX -7.9%, IOVA -7.7%, NET -7.7%, DKNG -7.6%, AMN -7.6%, CPRI -7.2%, AKAM -7.1%, U -7%, SERV -6.7%, PDFS -6.6%, ECO -6.3%, TVTX -6%, GDOT -6%, RXST -5.6%, MNST -5.6%, ABNB -5.6%, ANET -5.4%, CABO -5.4%, AFRM -5.4%, VLY -5.3%, NVEE -5.1%, SPT -4.9%, FTNT -4.9%, RRR -4.8%, BE -4.7%, IONQ -4.5%, FORM -4.2%, WEST -4.2%, SQ -4.2%, INFA -4.1%, STEP -3.5%, LGF.A -3.5%, ARRY -3.2%, JAMF -3%, ADEA -2.8%, YELP -2.8%, MGNI -2.6%, FROG -2.6%, PLUG -2.5%, SVV -2.5%, KTOS -2.4%, OS -2.3%, HRB -2.3%, CLFD -2.2%, RNG -2.1%, CRBG -2%, STN -2%, LASR -2%, ZD -2%

Insider Action: No names see Insider buying with dumb short selling. TTSH sees Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Pre-Market Movers: DJT PINS MSNT ABNB DKNG SG BBWI. (CNBC)

- 5 Things To Know Before The Market Opens. (CNBC)

- Bloomberg Lead Story: Trump To Move Court Further Right. (Bloomberg)

- Markets Wrap: Stocks slip as rally takes a breather. (Bloomberg)

- Boeing (BA) to proceed with job cuts. (Reuters)

- Steve Madden (SHOO) to move shoe production out of China due to tariff threats. (NYT)

Economic:

- November University of Michigan Consumer Sentiment is due out at 10:00 a.m. EDT and expected to rise to 70.6 from 70.5.

- Weekly Baker Hughes Rig Count is due out at 1:00 p.m. EDT.

Geopolitical:

- Federal Reserve Speakers are now out of the blackout period. Expect to hear from Federales.

- Federal Reserve Governor Michelle Bowman speaks at 11:00 a.m. EDT.

- President Biden receives the Daily Briefing at 11:45 a.m. EDT

- Watch our Twitter feed, Bullet86, for any impromptu appearances.

M&A Activity and News:

- YELP to acquire RepairPal for $80 mln in cash, close by year-end.

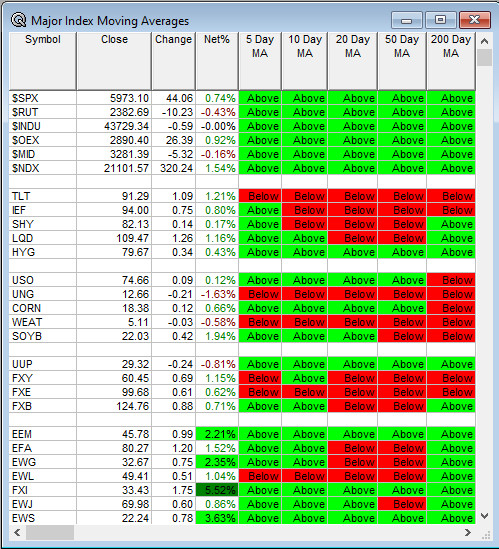

Moving Averages On Major Equity Indexes: Remains at 100%. Other asset classes continue to struggle.

Meeting & Conferences of Note:

-

- Sellside Conferences:

- Goldman Sachs APAC Healthcare Corporate Day

- Hovde Group Financial Services Conference

- Sellside Conferences:

-

- Fireside Chat: None of note.

- Top Shareholder Meetings: ABCL, ANIX, APVO, BCTX, CADL, CGEN, CLDI, CUE, CVAC, GNPX, HOWL, IMTX,

INKT, KA, LYEL, NXTC, TCRX, XAIR, XBIO, XLO - Top Analyst, Investor Meetings: CACI, MOH

- Update: None of note.

- R&D Day: None of note.

- FDA Presentation:

- Company Event: None of note.

- Industry Meetings or Events:

- BancAnalysts Association of Boston Conference

- Inaugural Sport United Conference

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Upgrades: OFIX IIPR IFF HAE DPZ CHWY BNTX BAC ADTN

Downgrades: NOVA LZ IBP CE