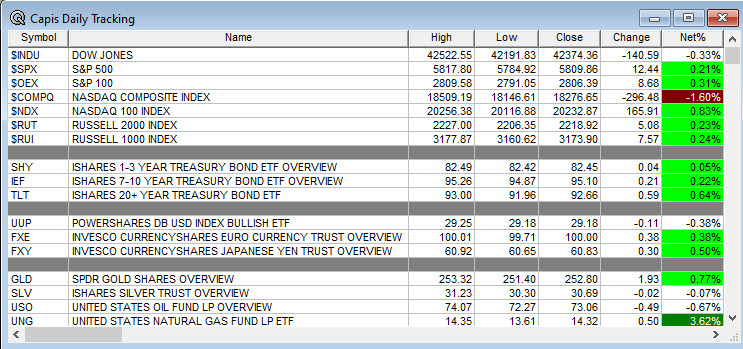

Overnight Summary: The S&P 500 closed Thursday higher by 0.21% at 5809.86 from Wednesday lower by -0.92% at 5787.42. The overnight high was hit at 5865 at 6:35 a.m. EDT and the low was hit at 5844.25 at 1:10 a.m. EDT. The overnight range is 21 points. The current price is 5864.25 at 6:35 a.m. EDT higher by +15 points higher by +0.26%.

Executive Summary: After three days of selling and a break of 5800 on the S&P 500, stocks are bouncing this morning for a second day and back above 5800. There was overnight weakness and then strength as the S&P 500 hit its low early in the morning.

Article of Note:“Prediction Markets Reflect That the Clock Favors Trump”. by John Authers (Bloomberg)

Key Events of Note Today:

- Durable Orders and the University of Michigan Consumer Sentiment are due out this morning.

- Weekly Baker Hughes Rig Count is due out at 1:00 p.m. EDT

Earnings Out After The Close

- Beats: COF +0.74, SAM +0.35, DECK +0.35, RMD +0.15, BYD +0.12, SKX +0.10, LHX +0.09, WDC +0.07, VRSN +0.06, WY +0.05, PFG +0.03, DXCM +0.02, EW+0.01, MHK +0.01, ZYXI +0.01 of note.

- Flat: None of note.

- Misses: TROX -0.30, OLN -0.25, TXRH -0.06, CINF -0.04, CSL -0.04, UHS -0.01, NOV -0.01, HIG -0.01 of note.

- IPOs For The Week: ADUR, ALEH, CUPR, FBGL, GELS, HUHU, INGM, LBGJ, NTCL, PRB, ROLR, SAG, SNYR

- New IPOs/SPACs launched/News:

- IPOs Filed/Priced:

- Secondaries Filed or Priced:

- ADC Common Stock Offering 4,000,000 shares

- JOBY Public Offering of Common Stock – up to $200.0 million of its shares

- LODE: FORM S-3 – 6,864,696 Shares of Common Stock

- QLGN: Form S-1.. Up to 14,000,000 Shares of Common Stock

- Notes Priced:

- Direct Offering:

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders of note:

- Debt/Credit Filing and Notes:

- Mixed Shelf Offerings:

- HON filed a mixed-shelf offering

- JOBY filed a mixed-shelf offering

- VERO filed a $30 million mixed-shelf offering

- VLTO filed a mixed-shelf offering

- PIPE:

- Convertible Offerings & Notes Filed:

- PATK Closing of $500 Million Senior Notes Offering and New Credit Facility

- WCN filed debt securities

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down After The Close:

- Movers Up: MGRC +13.1%, WDC +9.3%, DECK +8.8%, RMD +7.5%, DLR +6.2%, SKX +5%, APPF +4.6%, LHX +4.4%, COF +4%, FHI +3.7%, VTMX +2.9%, BYD +2.6%, of note.

- Movers Down: CPRI -46%, COUR -16.1%, TBBK -10%, MHK -9.1%, OLN -7.7%, FIX -6.7%, DXCM –4.7%, CUZ -6%, UHS -5.6%, PFG -5%, DXCM -4.7%, ROG -3.5%, ATR -3.4%, HIG -2.9% of note.

News After The Close:

- Restaurant Brands Int’l (QSR) Burger King unit removed onions from menu at CO store due to risk of illness. (Guardian)

- Barrick (GOLD) responds to Mali Government’s claims of breaching its commitments; denies the allegations made by the Malian Ministry of Mines and the Finance Ministry

- Judge has blocked Tapestry (TPR) acquisition of Capri Holdings (CPRI). (CNBC)

- Taiwan Semiconductor Manufacturing’s (TSM) Arizona plant production yields 4 percentage points higher than its Taiwan factories. (Bloomberg)

- Barron’s: Don’t Rule Out a Post Elections Market Panic. (Barron’s)

Buybacks or Repurchases:

Exchange/Listing/Company Reorg and Personnel News:

- Morgan Stanley (MS) announces that Chief Executive Officer Edward Pick was elected by the Board of Directors to the additional position of Chairman, effective January 1, 2025

- NFE appointed Andrew Dete as the Company’s President, effective immediately

- APPF CFO Fay Sien Goon steps down; also co acquires LiveEasy, a concierge platform

Dividends Announcements or News:

- Stocks Ex Div Today: CARR FAST J UNM COKE CWSI SM SIG CNXC LKFN KALU

- Stocks Ex Div Monday: BX ACI KNTK TXNM EVTC DMLP RMR SPFI VALU

- FIX increases quarterly dividend to $0.35/share from $0.30/share

- MSEX increases quarterly cash dividend 4.62% to $0.34/share from $0.325/share

- AUB increases quarterly dividend 6% to $0.34/share from $0.32/share

- MUSA increases quarterly cash dividend 6.7% to $0.48/share from $0.45/share

- AROC increases quarterly dividend to $0.175/share from $0.165/share

What’s Happening This Morning: Futures S&P 500 + NASDAQ + Dow Jones + Russell 2000 + (at 8:15 a.m. EDT). Asia is lower ex Australia while Europe is lower. VIX Futures are at 18.37 from 18.27 while Bonds are at 4.198% from 4.192% on the 10-Year. Crude Oil and Brent are higher with Natural Gas lower. Gold, Silver and Copper are lower. The U.S. Dollar is higher versus the Euro, lower versus the Pound and higher against the Yen. Bitcoin is at $67.925 from $67,225 lower by -166 at -0.24% this morning.

- Daily Positive Sectors: Consumer Cyclical, Communication Services, Financials and Real Estate of note.

- Daily Negative Sectors: Healthcare, Materials, Industrials and Utilities of note.

- One Month Winners: Utilities, Technology, Materials, Financials and Industrials of note.

- Three Month Winners: Utilities, Real Estate, Financials, Materials, Industrials and Consumer Defensive of note.

- Six Month Winners: Technology, Utilities, Real Estate, Financials and Consumer Cyclical of note.

- Twelve Month Winners: Technology, Financials, Utilities, Communication Services and Industrials note.

- Year to Date Winners: Technology, Utilities, Financials, Industrials and Communication Services of note.

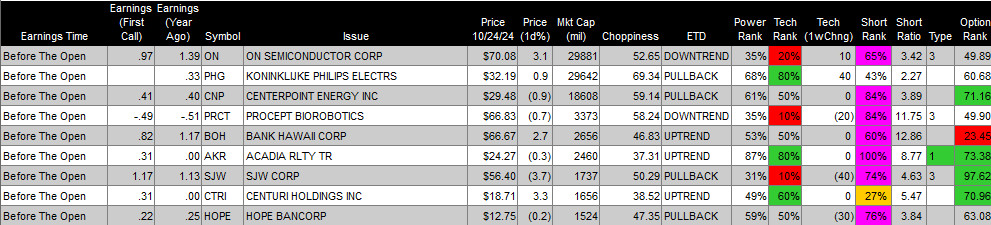

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Friday After the Close: None of note.

- Monday Before The Open:

Earnings of Note This Morning:

- Beats: SNY +2.03, BAH +0.34, CNC +0.26, AON +0.24, CRI +0.24, CL+0.02, WT +0.01 of note.

- Flat: None of note.

- Misses: NYCB -0.38, AN -0.34, B -0.30, SAIA -0.07, HCA-0.06 of note.

- Still to Report:

Company Earnings Guidance:

- Positive Guidance: APPF MGRC CNC of note.

- Negative or Mixed Guidance: ATR CSL DECK MHK of note.

Advance/Decline Daily Update: The A/D Line traded sideways much like the S&P 500.

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: LYEL +17.9%, TPR +14.6%, DECK +14.1%, MGRC +14%, WDC +11.8%, SAVE +11.2%, CNC +10.4%, DLR +9.6%, SKX +7.1%, APPF +6.7%, RMD +5.7%, MTX +5%, TYRA +4.9%, LHX +4.9%, COF +4.5%, BYD +4%, ZYXI +3.6%, SNY +3%, IDYA +2.9%, DFS +2.8%, VTMX +2.8%, NWG +2.8%, EPSN +2.7%, SEDG +2%

- Gap Down: CPRI -46.8%, COUR -18.2%, COUR -18.2%, TBBK -15.3%, MHK -9.6%, OLN -9.5%, JOBY -8.3%, DXCM -7.1%, CUZ -6%, TROX -5.8%, UHS -5.6%, WY -4.7%, SAM -4%, FIX -3.7%, SPSC -3.4%, HTH -3%, HIG -2.7%, WKC -2.7%, XRAY -2.1%, MSEX -2.1%,

Insider Action: None of note that see Insider buying with dumb short selling. None of note that see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- Pre-Market Movers: Check back as not out yet. (CNBC)

- Latest CNN Headlines. (CNN)

- Bloomberg Lead Story: Trump 2.0 Haunts World Economy Chiefs at IMF Annual Meeting. (Bloomberg)

- Markets Wrap: US Futures trim weekly drop, Treasuries gain. (Bloomberg)

- North Korea send more troops to Russia says South Korea. (Bloomberg)

- Elon Musk has had secret conversations with Russian President Putin. (WSJ)

- Boeing (BA) workers rejected new contract over retirement benefits. (NYT)

- Bloomberg: Big Take – Wall Street Takes Tax Loss Harvesting To Next Level (Podcast)

- Bloomberg: Odd Lots – Lots more on the ongoing mess at Boeing (BA). (Podcast)

- NYT Daily: United States of Pennsylvania. (Podcast)

- Marketplace: Hurricanes to test catastrophe bond market. (Podcast)

- Wealthion: Market Euphoria to end. (Podcast)

Economic:

- September Durable Orders are due out at 8:30 a.m. EDT and is expected to fall to -0.90% from 0.0%.

- University of Michigan Consumer Sentiment (final) is due out at 10:00 a.m. EDT and expected to stay at 68.90. Remember Michigan Inflation Expectations are built into this report.

- Weekly Baker Hughes Rig Count is due out at 1:00 p.m. EDT.

Geopolitical:

- No speakers of note today.

- President Biden travels back from Phoenix, Arizona and arrives in Philadelphia at 7:10 p.m. EDT.

- President Biden receives the Daily Briefing at 11:00 a.m. EDT.

- President Biden delivers remarks to the Gila River Indian Community at 2:30 p.m. EDT.

- Watch our Twitter feed, Bullet86, for any impromptu appearances.

M&A Activity and News:

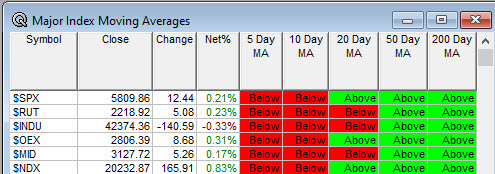

Moving Averages On Major Equity Indexes: Moves from 46% positive to 50%.

Meeting & Conferences of Note:

-

- Sellside Conferences:

- Goldman Sachs Emerging Market Conference

- Sellside Conferences:

-

- Fireside Chat: None of note.

- Top Shareholder Meetings: BCRX, JAGX, KALV, PALI, PHVS, SEEL

- Top Analyst, Investor Meetings: APLS, GVP, ITRM, SENS, SGRP

- Update: None of note.

- R&D Day: None of note.

- FDA Presentation:

- IRON: Data Presentation on DISC-0974

- ITRM: PDUFA Decision on Sulopenem

- RVMD: Data Presentation on TYRA-300: Data Presentation on RMC9805

- TYRA: Data Presentation on TYRA-300

- Company Event: None of note.

- Industry Meetings or Events:

- AACR-NCI-EORTC Symposium on Molecular Targets and Cancer Therapeutics

- Game Industry Conference

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Upgrades: BKR ANVS DENN

Downgrades: WES BYON AAPL