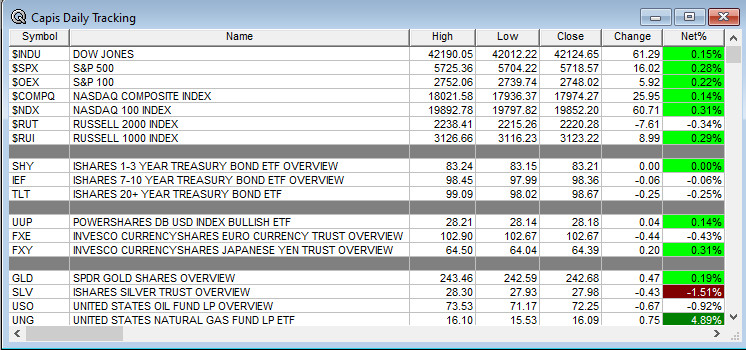

Overnight Summary: The S&P 500 closed Monday higher by 0.28% at 5718.57 from Friday lower by -0.19% at 5702.55. The overnight high was hit at 5793.50 at 4:30 a.m. EDT and the low was hit at 5763.75 at 10:25 a.m. EDT. The overnight range is 30 points. The current price is 5772 at 7:15 a.m. EDT lower by -4.75 points.

Most Important Article Of the Morning:

Executive Summary: President Biden speaks to the U.N. General Assembly this morning and then delivers a couple of speeches in NYC after that. Consumer Confidence is out at 10:00 a.m. EDT. Overnight China unleashed a stimulus package to ignite their rather tepid economy.

- 2-Year Note Auction at 1:00 p.m. EDT.

Earnings Out After The Close:

- Beats: AIR +0.03 of note.

- Flat:

- Misses: None of note.

- IPOs For The Week: BIOA, BKV, FBGL, GRDN, LGCY, NAMI, SAG, SUNH,

WCT, ZENA, ZJK - New IPOs/SPACs launched/News:

- IPOs Filed/Priced:

- Secondaries Filed or Priced:

- IVT announces proposed public offering of 6.5 mln shares of common stock

- APLD files for up to 2,500,000 shares of its Series E-1 Redeemable Preferred Stock at a price per share of $25.00

- HE to make an offering of $500 mln of shares of its common stock

- Notes Priced:

- Direct Offering:

- Exchangeable Subordinate Voting Shares:

- Selling Shareholders of note:

- Debt/Credit Filing and Notes:

- Mixed Shelf Offerings:

- HIG files mixed shelf securities offering

- HBNC files $250 mln mixed shelf securities offering

- PIPE:

- Convertible Offering & Notes Filed:

- SNOW announces proposed private placement of $2 billion of convertible senior notes

- Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

Biggest Movers Up & Down Last Week:

- Movers Up: LBRDA +21.9%, LWAY +15.6%

- Movers Down: HE -9.5%, SNOW -3.3%, IVT -2.7%, PANL -2%.

News After The Close :

-

- LBDRA issues a counterproposal to Charter Communications (CHTR) in response to an initial merger proposal

- FOR files $750 mln mixed shelf securities offering; also files for 15,000,000 shares of common stock offering by D.R. Horton (DHI)

- DE heads -1% lower after Trump threatens 200% tariff if jobs move to Mexico

- Danone (DANOY) proposes to acquire all shares of LWAY common stock not currently held for $25.00 a share

- Boeing (BA) awarded $319 mln U.S. Navy contract

- META to announce celebrity voices as options on its AI chatbot. (Reuters)

- FTC expected to greenlight Chevron’s (CVX) previously announced $53 bln merger proposal of Hess (HES). (Reuters)

- 10-Q or 10-K Delays – None of note.

- NASDAQ Delisting Notice – None of note.

Buybacks or Repurchases: Buybacks should be slow as most companies are in a blackout period as earnings season kicks into gear.

- ITRI authorizes new share repurchase program of up to $100 mln over an 18-month period.

Exchange/Listing/Company Reorg and Personnel News:

-

- JAMF appoints David Rudow to CFO, he will begin on October 28, and will succeed Jamf’s current CFO Ian Goodkind, who is departing to pursue other opportunities, effective November 28.

- SIGI announces appointment of Patrick Brennan as CFO, effective October 1, 2024

- ACAD announces that Catherine Owen has succeeded Steve Davis as CEO.

- RILY Kenny Young resigned from positions as President of the Company, CEO of B. Riley Principal Investments, LLC, and other officer roles at other subsidiaries on September 20

Dividends Announcements or News:

- Stocks Ex Div Today: TTE E EQR STM POR ARCO

- Stocks Ex Div Tomorrow: JCI AHH BFC MERC

What’s Happening This Morning: Futures S&P 500 +2 NASDAQ 100 +22 Dow Jones +37 Russell 2000 +18. Asia is higher ex Australia with Europe is higher this morning. VIX Futures are at 17.52 from 17.67 yesterday while Bonds are at 3.798% from 3.76% on the 10-Year. Crude Oil and Brent are higher with Natural Gas higher as well. Gold, Silver and Copper higher. The U.S. Dollar is lower versus the Euro, lower versus the Pound and higher against the Yen. Bitcoin is at $63,587 from $63,449 higher by +0.33% this morning.

- Daily Positive Sectors: Consumer Cyclical, Energy, Real Estate and Utilities of note.

- Daily Negative Sectors: Healthcare and Communication Services of note.

- One Month Winners: Utilities, Real Estate, Financials, Consumer Cyclicals and Industrials of note.

- Three Month Winners: Real Estate, Utilities, Financials, Consumer Defensive, Healthcare and Industrials of note.

- Six Month Winners: Utilities, Real Estate, Technology, Financials, Consumer Defensive and Communication Services of note.

- Twelve Month Winners: Technology, Financials, Communication Services, Industrials, Utilities and Real Estate note.

- Year to Date Winners: Technology, Utilities, Financials, Communication Services, Consumer Defensive and Healthcare of note.

Upcoming Earnings Of Note: (From Chartroom Software – sorted by market cap, highest to lowest with most visible names)

- Tuesday After the Close:

- Wednesday Before The Open:

Earnings of Note This Morning:

- Beats: THO +0.40 of note.

- Flat:

- Misses: AZO -5.57 of note.

- Still to Report:

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative or Mixed Guidance: None of note.

Advance/Decline Weekly Update With Both Daily and Weekly Stats: Markets have improved nicely in the last week. The Daily A/D Line has made a new high while the S&P 500 just made a new high Thursday and is now coming off that high.

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: LBRDA +18.6%, LWAY +16%, LVO +5%, NTRA +3.6%, AIR +3.6%, ACAD +3%, ESEA +3%, HES +2.7%, APLD +2.2%, BIIB +2.1%, RUN +2.1%

- Gap Down: LNW -15.5%, HE -12.1%, THO -6.4%, FOR -6%, SNOW -3%, IVT -3%, JAMF -2%

Insider Action: CODI sees Insider buying with dumb short selling. No names see Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- 5 Things To Know Before The Market Opens Today. (CNBC)

- What You Need To Know To Start Your Day. (Bloomberg)

- Pre-Market Movers: V SBUX CRM LOW (CNBC)

- Bloomberg Lead Story: China Unleashes Stimulus Package to Revive Economy and Markets. (Bloomberg)

- Markets Wrap: US Futures steady as Chinese stocks soar on stimulus. (Bloomberg)

- Novo Nordisk (NVO) CEO to testify before the Senate on high weight drug prices. (CNBC)

- JP Morgan (JPM) CEO Dimon warns geopolitical is getting worse. (CNBC)

- Bloomberg: The Big Take – Supply Chain threats are rampant. (Podcast)

- Bloomberg: Odd Lots: John Rogers of Ariel on winning with value investing. (Podcast)

Economic:

- September Consumer Confidence is due out at 10:00 a.m. EDT and expected to rise to 103.80 from 103.50.

- Weekly API Crude Oil Data is due out at 4:30 p.m. EDT.

Geopolitical:

- President Biden receives the Daily Briefing at 9:00 a.m. EDT.

- President Biden delivers remarks to General Assembly of the United Nations at 10:00 a.m. EDT.

- President Biden meets with United Nations Secretary General Antontio Guterres at 11:00 a.m. EDT.

- Later in the day President Biden delivers remarks to the Global Coalition to Address Synthetic Drug Threats at 1:45 p.m. EDT.

- Last President Biden delivers remarks on climate at the Bloomberg Global Business Forum at 4:30 p.m. EDT.

Federal Reserve Speakers:

- Federal Reserve Governor Michelle Bowman speaks at 9:00 a.m. EDT.

M&A Activity and News:

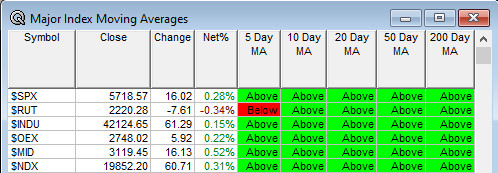

Moving Averages On Major Indexes: Move from 100% to 97% of the moving averages being positive.

Meeting & Conferences of Note:

-

- Sellside Conferences:

- Bank of America World Medical Innovation

- Deutsche Bank Leveraged Finance Conference

- Evercore ISI ADAS AV & AI Forum

- Oppenheimer Innovating Sustainability Summit

- RBC Pharmaceutical Development, Manufacturing and Bioprocessing Conf

- Scotiabank 3rd Annual Fixed Income Forum

- Fireside Chat: None of note.

- Top Shareholder Meetings: CGC, GIS, WOR

- Investor/Analyst Day/Calls: GPN, SGML, WPM

- Update: None of note.

- R&D Day: None of note.

- Sellside Conferences:

-

- FDA Presentation:

- Company Event:

- Industry Meetings or Events:

- Access Alpha Buyside Best Ideas Virtual Fall

- Atlantic Council Roundtable

- Blackbaud’s bbcon Tech Conference

- Climate Week NYC

- European Conference on Optical Comm

- International Conference on Ion Implantation Technology

- International Society for Diseases of the Esophagus World Congress

- International Ultrasonics Symposium

- NIC Fall Conference

- Verint Engage Customer Engagement Conf

- World Medical Innovation Forum

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Upgrades: MESO

Downgrades: