Overnight Summary: The SP 500 closed Monday lower by -1.20% at 5061.62 from Friday lower by -1.46% at 5123.41. The overnight high was hit at 5,120.25 at 8:00 a.m. while the overnight low was hit at 5081.25 at 10:40 p.m. EDT. The range overnight is 39 points as of 8:00 a.m. EDT. Currently, the S&P 500 is higher by +10 points at 8:10 a.m. EDT.

- Federal Reserve Chairman Powell to speak at 1:15 p.m. EDT.

- Several more economic data points this morning for Treasuries to decide if they continue to climb.

- Beats: SKIL +0.23, CFB +0.02.

- Flat: None of note.

- Misses: MITK -0.04.

Capital Raises:

- IPOs Priced or News: None of note.

- New SPACs launched/News: None of note.

- Secondaries Priced:

- MFA priced offering of Senior Notes.

- Notes Priced of note: None of note.

- Common Stock filings/Notes: None of note.

- DOOO files secondary offering of 1,500,000 shares through BMO.

- LAES files ordinary offering of 40,000,000 shares.

- STI files 41,066,656 shares of common stock.

- SYTA files $4 million of common stock.

- Direct Offering: None of note.

- Exchangeable Subordinate Voting Shares: None of note.

- Selling Shareholders of note: None of note.

- APLD files 23,585,000 shares of common stock from selling shareholder.

- Private Placement of Public Entity (PIPE): None of note.

- Mixed Shelf Offerings: None of note.

- EXR files mixed-shelf offering.

- HSDT files mixed-shelf offering.

- Debt/Credit Filing and Notes: None of note.

- Tender Offer: None of note.

- Convertible Offering & Notes Filed: None of note.

Capital Raise Summary From The TradeXchange, bringing traders and investors real time news and Squawk Box, and other sources.

News After The Close :

- After Hours Movers:

- MBPC +39%, CFB +3.5%, GILD +2.5%,

- EXR -5.2%, MITK -4%, DOOO -3.7%, NVST -3.4%

- News Items After the Close:

- TechnipFMC (FTI) awarded a large contract in Guyana’s Stabroek Block by Exxon Mobil Corporation (XOM) worth between $500 million and $1 billion.

- Canada’s Federal Budget will increase taxes on the wealthiest.

- Gildan Activewear (GIL) issues upside revenue guidance for Q1 of $695 million versus estimates of $675 million.

- First Watch (FWRG) buys completion of 21 of its franchise units in North Carolina for $75 million.

- General Dynamics (GD) wins $297 million U.S. Army contract.

- Groupon (GRPN) takes Q1 guidance to the high end of its guidance.

- Federal Reserve San Francisco President Mary Daly spoke at 8:00 p.m. EDT and said no need to urgently lower rates, significant progress on inflation but still not there and need more housing.

- Exchange/Listing/Company Reorg and Personnel News:

- Sprout Social (SPT) names President Ryan Barretto as CEO while current CEO Justyn Howard moves to Executive Chairman.

- Envista (NVST) names Paul Keel as CEO replacing Amir Aghdaei, who will remain a senior advisor.

- Buyback Announcements or News:

- Stock Splits or News:

- Dividends Announcements or News:

What’s Happening This Morning: Futures value reflects the change with fair value.

Sector Action – (1/3/6/12/YTD Updated Weekly with Monday release):

- Daily Positive Sectors: None of note.

- Daily Negative Sectors: All led by Technology, Real Estate, Communication Services and Consumer Cyclical.

- One Month Winners: Energy, Communication Services, Basic Materials and Industrials of note.

- Three Month Winners: Energy, Technology, Communication Services, Industrials and Materials of note.

- Six Month Winners: Technology, Financials, Industrials and Communication Services of note.

- Twelve Month Winners: Technology, Communication Services, Consumer Cyclical and Financial of note.

- Year to Date Winners: Communication Services, Technology, Energy, Industrials and Financials of note.

Upcoming Earnings Of Note:

- Tuesday After the Close:

- Wednesday Before the Open:

Earnings of Note This Morning:

- Beats: MS +0.32, UNH +0.30, BK +0.10, PNC +0.09, BAC +0.07, JNJ +0.07, CBSH +0.06, .

- Flat: None of note.

- Misses: NTRS -0.49, of note.

- Still to Report: None of note.

Company Earnings Guidance:

- Positive Guidance: None of note.

- Negative Guidance: None of note.

Erlanger Research Advance/Decline Chart:

Gap Ups & Down In Early Pre-Market (+2% or down more than -2%):

- Gap Up: MCBC +38.8%, ERIC +8.1%, UNH +6.9%, CBSH +3.8%, WRN +3.5%, GIL +2.5%, ZVRA +2.2%, BK +2.2%, DJT +2%of note.

- Gap Down: INO -24%, GRPN -6%, ORIC -5.7%, MITK -4.5%, NVST -3.3%, DOOO -2.7%, WTFC -2.3%, SPT -2%, VALE -2%, ARGX -2%, TSLA -1.9%, of note.

Insider Action: CRMT see Insider buying with dumb short selling. BRT sees Insider buying with smart short sellers.

Rags & Mags: Repeated stories from prior days never listed, i.e. “rehashed news”. Sorted by Global, U.S. and stock specific.

- 5 Things To Know Before the Stock Market Opens Today. (CNBC)

- What You Need To Know To Start Your Day. (Bloomberg)

- Bloomberg Lead Story: Israel Vows Response to Iran As U.S. and Allies Urge Restraint. (Bloomberg)

- Markets Wrap. S&P 500 steady after selloff rattles globe. (Bloomberg)

- China’s Q1 GDP growth surpassed expectations. (Fox Business)

- However, China’s factories drive uneven economic recovery. (WSJ)

- Dollar heads for best run in a year as Fed Seen Delaying Cuts. (Bloomberg)

- What you need to know about the Bitcoin halving. (MarketWatch)

- House Speaker Johnson to advance separate bills on Israel, Ukraine, and Taiwan after attack in Iran. (CNBC)

- United Healthcare (UNH) beats estimates despite impact from attack on Change Healthcare. (CNBC)

- Bloomberg: Daybreak Podcast: (Podcast)

- Marketplace: How Arizona is preparing for AI powered election misinformation. (Podcast)

- NY Times Daily: How AI’s insatiable appetite for data became a problem. (Podcast)

- Wealthion: Oil soars, Bitcoin teeters:Inflation grip tightens. (Podcast)

Moving Average Update: Score drops to 20% from 34%.

Geopolitical:

- President’s Public Schedule:

- The President and The Vice President receive the President’s Daily Brief, 10:30 a.m. EDT

- The President departs the White House en route to Joint Base Andrews, 11:55 a.m. EDT

- The President departs Joint Base Andrews en route to Scranton, Pennsylvania, 12:15 p.m. EDT

- Press Secretary Karine Jean-Pierre will speak aboard Air Force One en route to Scranton, Pennsylvania, 12:30 p.m. EDT

- The President arrives in Scranton, Pennsylvania, 1:00 p.m. EDT

- The President participates in a campaign event, 2:00 p.m. EDT

- The President participates in a campaign event, 5:40 p.m. EDT

Economic:

- March Housing Starts are due out at 8:30 a.m. EDT and are expected to fall to 1,485,000 from 1,521,000.

- March Industrial Production is due out at 9:15 a.m. EDT and is expected to rise to 0.4% from 0.1%.

Federal Reserve / Treasury Speakers:

- Federal Reserve Phillip Jefferson to speak at 9:00 a.m. EDT

- Federal Reserve New York President John Williams to speak at 12:30 p.m. EDT.

- Federal Reserve Richmond President Thomas Barkin to speak at 1:00 p.m. EDT.

- Federal Reserve Chairman Jerome Powell to speak at 1:15 p.m. EDT.

M&A Activity and News:

- Macatawa Bank Corporation (MBC) and Wintrust Financial (WTFC) enter into a merger where Wintrust acquires MBC for $14.85 a share.

Meeting & Conferences of Note:

- Sellside Conferences:

- Bloom Burton Healthcare Conference

- Canaccord Horizons in Oncology Virtual Conference

- Kemper Life Sciences Conference

- Morgan Stanley Brazil Education Corporate Access Day.

- Piper Sandler Spring Biopharma Symposium

- Stifel Target Oncology Forum

- Top Shareholder Meetings: None of note.

- Fireside Chat: None of note.

- Investor/Analyst Day/Calls: APPN, NVX

- Update: None of note.

- R&D Day: None of note.

- Company Event:

- SS&C Deliver Europe Conference

- Industry Meetings:

- American Academy of Neurology Meeting

- Battery Supply Chain Finance Summit

- Benzinga Cannabis Capital Conference

- HEART Conference

- Quantum Computing Symposium

- ISN World Congress of Nephrology

- Spinal Cord Injury Investor Symposium

- World Orphan Drug Congress USA

- S&P Global Power Markets Conference

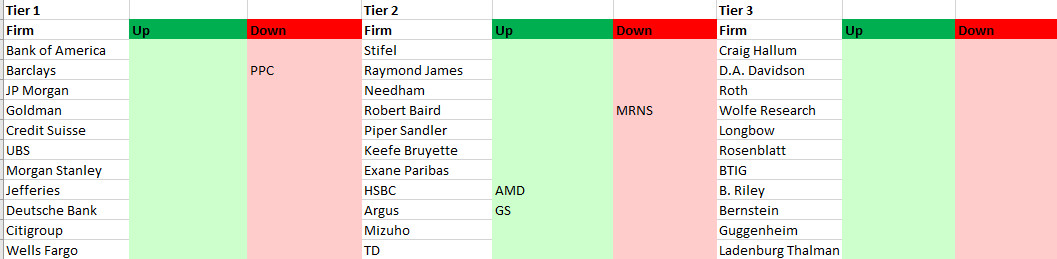

Top Tier Sell-side Upgrades & Downgrades:

The recommendations listed below in this “Upgrade/Downgrade” section are compiled from what we believe are Tier I, II and III firms. Recommendations posted are taken from a variety of sources each day and we only post upgrades or significant initiations as well as downgrades to underweight or sell. The purpose of this posting is to make the reader aware of market-moving recommendations. None of these recommendations should be interpreted as actual recommendations from CAPIS or its employees.

Today’s Upgrades and Downgrades: